(Bloomberg Opinion) -- It turns out Wall Street bond traders aren’t the only ones who can turn quick profits on falling interest rates.

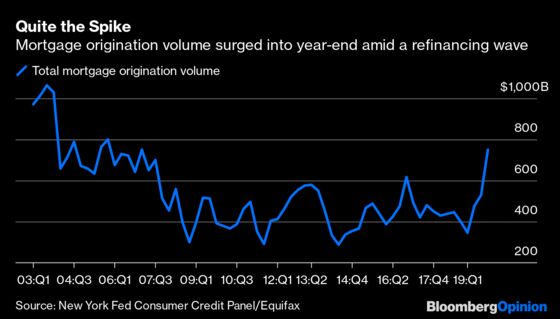

The Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit on Tuesday revealed that mortgage origination volume in the final three months of 2019 soared to $752 billion, the largest since the end of 2005 and up significantly from $528 billion in the third quarter. In a statement, the bank attributed the surge to “a large increase in refinance activities.” Data released Wednesday by the Mortgage Bankers Association showed refinancing activity continued to climb, making up almost two-thirds of applications in the week ended Feb. 7.

It’s worth delving deeper into this number because it’s not as if every drop in long-term U.S. Treasury yields has led to this kind of refinancing boom — and especially not as quickly.

The most recent lurch higher in mortgage origination volume before this was in the fourth quarter of 2016. That makes sense, given that 30-year Treasury yields fell to a record low at the time of 2.09% in early July that year, down from 3% just six months earlier. Measuring from that point would mean there was a lag of at least three months before homeowners really stepped up and took advantage of their refinancing options. By contrast, 30-year Treasury yields fell to a record low of 1.9% on Aug. 28. That means in the span of as little as five weeks, some borrowers went through the process of refinancing their mortgages.

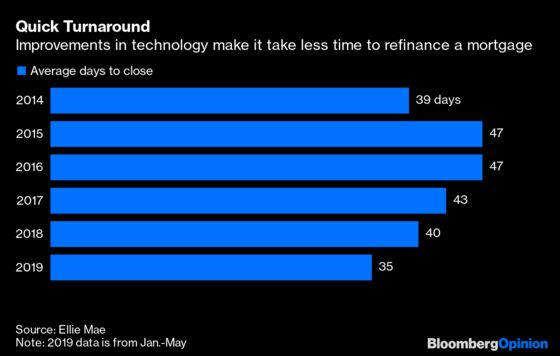

The difference between then and now is almost certainly due to technological advancements that serve to speed up the reaction time to lower interest rates in the mortgage market. Bloomberg News’s Christopher Maloney spoke last year with Jonathan Corr, president and CEO of Ellie Mae Inc., which makes software that aims to streamline the mortgage origination process. According to data from the company, it now takes about 35 days to close on a refinancing, compared with 47 days in 2016. And some lenders say they can do it in three weeks or less. That’s a boon to homeowners when the 30-year mortgage rate is just 3.45%.

Even some heavy-hitters in the mortgage market are riding the technological wave. Maloney recently interviewed Tim Mayopoulos, the former CEO of Fannie Mae. He’s now president of Blend Labs Inc., a company that provides online platforms for mortgage lenders to make loans. Here’s what Mayopoulos had to say about changes in mortgage finance in a Q&A:

“First, the entire process is much faster than it used to be. At Blend we recently announced a one tap mortgage pre-approval where a consumer can sign on to their mobile app and give their consent to start a process that checks their bank statements, income, employment and other characteristics within seconds and let the potential borrower know the mortgage amount available to them and its terms.

…

Consumers could not understand why they could order from Amazon and see delivery within a few days, yet they had to spend a time and labor intensive process chasing after pieces of paper and using fax machines to get a mortgage.

I had gotten to know Nima Ghamsari, the founder of Blend, while I was at Fannie Mae and we had similar views of what the future should look like – that a consumer would be able to apply for a mortgage on their smart phone and know whether or not they’ve been approved in a matter of seconds.”

This trend toward digital platforms and mobile applications, of course, goes well beyond Amazon.com Inc., Netflix Inc. and Uber Technologies Inc. The largest Wall Street banks are all-in on providing their customers with a comprehensive mobile-banking platform that allows them to deposit checks and move their money around without ever stepping into a brick-and-mortar branch. And there are even ways for savvy individuals to maximize interest rates down to the basis point through various online savings accounts and certificates of deposit.

That kind of quick maneuvering would seemingly depend on a customer’s comfort with new technology. Yet in the New York Fed’s data on mortgages, age actually didn’t appear to make much of a difference. In fact, the biggest percentage increase in origination volume in the fourth quarter from the previous quarter was for borrowers aged 60 to 69. On a dollar basis, those aged 40 to 49 had the largest jump.

Credit scores showed a clearer divide: People with the most pristine credit made up most of the activity. Those with scores above 760 accounted for $479 billion of origination volume, the most ever for a three-month period. Adding in those with scores from 720 to 759, the combined total of $598 billion was the highest since 2003, when origination volume across the credit spectrum peaked at more than $1 trillion. At that time, though, mortgage origination among borrowers with scores of 719 or worse totaled $389 billion. Last quarter it was less than half that, at $154 billion.

This quicker reaction to changing interest rates will undoubtedly cause headaches for mortgage-bond investors. The securities tend to thrive in times of lower volatility because they’re less vulnerable to early prepayments, which force traders to buy new debt at lower yields, or extension risk, where interest rates rise and traders are stuck holding lower-yielding debt.

Mortgage-backed securities aside, though, it’s encouraging that homeowners have new ways to quickly and easily lock in savings on their mortgages. It at least comes closer to leveling the playing field between households, which have been cautious overall and have barely taken on more debt as a percentage of gross domestic product since the financial crisis, and non-financial corporations, which have rushed to take advantage of rock-bottom interest rates by leveraging up. With interest rates seemingly lower for a lot longer, Main Street deserves a taste of on-demand cheap financing.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.