(Bloomberg Opinion) -- The newest way to own the libs is to not own the libs.

The American Conservative Values ETF (ticker: ACVF) was launched at the end of October. Its guiding principle is that, whether you like it or even know it, your portfolio is all too often funding the “liberal agenda.” So this ETF has a roster of companies — the “worst of the worst” — that it deems “politically active” in ways opposed to conservative causes and therefore boycotts. Presumably, the ACVF investor sleeps better knowing their money isn’t woke.

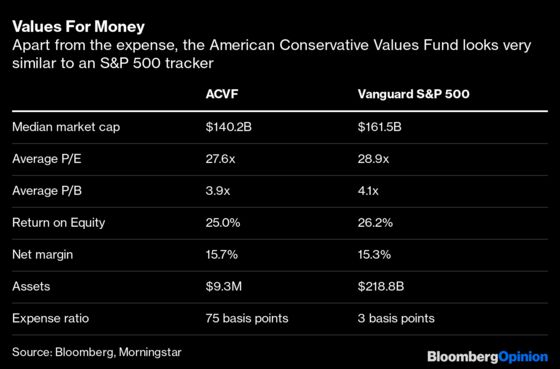

So now we know the price of being a principled financial conservative: 72 basis points. That is the spread between ACVF’s 75 point expense ratio and the few points it costs for an index tracker like the Vanguard S&P 500 ETF. Because when you look past the marketing, ACVF is essentially that most vanilla of products: a U.S. large-cap equity fund.

There is nothing inherently wrong with paying an extra 72 basis points to own something very much like the S&P 500 but with a rightward lean. If folks are willing to plow their cash into joke cryptocoins, then there’s clearly room for folks to chase an S&P 500-less-75-basis-points return. As for why one might sign up for that haircut, the answer partly has its roots in so-called social investing. Some investors have long sought to align their portfolios with their values by excluding companies that run afoul of religious, moral or ethical beliefs, most commonly businesses related to guns, tobacco and alcohol . But this was mostly a fringe movement.

That began to change roughly two decades ago with the arrival of ESG investing (even if the moniker “ESG” was not necessarily in wide usage back then). This often misunderstood strategy seeks to identify companies with environmental, social and governance attributes that reduce financial risk or enhance financial performance. Unlike values-based investing, ESG is supposed to apply objective criteria rather than subjective belief, meaning it can be packaged and mass-marketed like any other investing strategy. And that marketing has started to pay off.

ESG’s surging popularity has opened the door to values-based funds, too. Some of them, like ESG, can credibly claim to be objective and add value; and if they conform to your ethics, all the better. The fossil-fuel divestment campaign is a notable example, where you can actually make an argument that incorporates a defensible model of future cash flows. It’s harder to say that about a fund that, say, excludes an airline because it objects to changes in voting laws.

It’s just not that easy to draw political lines around that notoriously agnostic beast called the market. ACVF’s boycott list includes such left-wing stalwarts as, er, Walmart Inc. and Goldman Sachs Group Inc. Its top holding, on the other hand, is Microsoft Corp., which has skirted the deplatforming row over hard-right sites such as Parler to some degree but, on the other hand, supports LGBTQ rights and criticizes Georgia’s new voting restrictions.

“We have a lot of questions from conservative investors about Microsoft,” admits Tom Carter, president of Ridgeline Research LLC, which created the fund. He adds: “If you got rid of every tech company that leaned left, you’re not going to have much of a sector.” Quite.

It’s notable that ACVF launched less than a week before November's bitterly contested election. Around the same time, a left-leaning fund that similarly traffics in U.S. large-caps, albeit with a blue tinge, also launched. The Democratic Large Cap Core ETF is more quantitative, using political contributions to select companies. It’s also more concentrated, holding only around 40 stocks, and charges only 45 basis points. But that’s still a hefty chunk of your index returns taken in return for dubious benefit.

Both are well-timed to cash in on political tribalism. But investors are likely to discover that companies and markets, like politics, are complex and tend to resist conforming to a set of personal beliefs. No one can guarantee your portfolio will align neatly with your values, which themselves aren’t necessarily set in stone. The only sure thing is that attempting to do so will cost you. Values ain’t value.

And in that wonderful way of all things financial, a fund launched in 2002 that sought to monetize the opposite way of thinking, prioritizing investments in defense, tobacco, alcohol and gambling-related stocks. Its name: The Vice Fund.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2021 Bloomberg L.P.