(Bloomberg Opinion) -- Amazon.com Inc. may have cured one of its financial headaches. But now it has other problems on its hands.

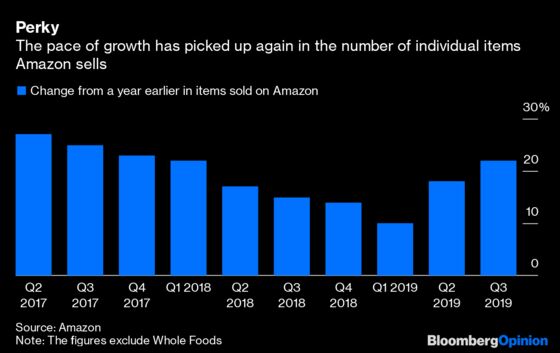

Amazon’s third-quarter financial report, released on Thursday, showed that customers are buying more stuff from its online bazaar, which is good news for a company that had a puzzling slowdown in growth. It appears to have helped that Amazon started to move from two-day standard shipping for its Prime shopping club members to one day. The number of individual items Amazon sold in the quarter increased at an accelerated rate of 22% in the third quarter, and revenue was higher than analysts had expected.

There are consequences of Amazon trying to kick-start growth with faster shipping and other methods, of course. It comes at the expense of profits.

Amazon has already warned that it’s spending more than it expected to speed up its package delivery operations. As a result of this and other increased spending, Amazon’s operating profit margin in North America shrank to 3%, the lowest in two years. The company is spending money in other areas, too, from salespeople for its cloud-computing division to programming for its streaming video service.

The company’s outlook for the fourth quarter suggests both that revenue growth will slow from the headier pace of recent quarters and that total company profit margins will continue to shrink. That wasn’t music to investors’ ears. Amazon shares fell in after-hours trading.

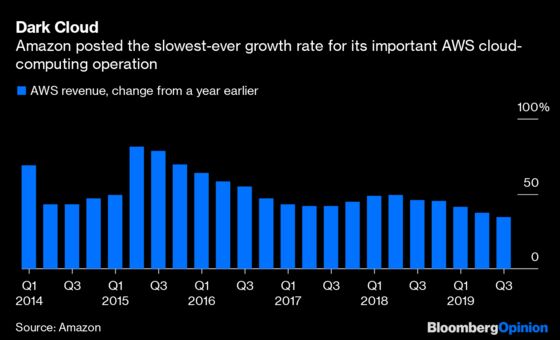

Perhaps Amazon’s best financial and strategic asset, its Amazon Web Services cloud-computing business, also showed worrying signs. The growth rate was the lowest dating back to at least 2014, when Amazon first began disclosing AWS financial results.

It’s not unusual for Amazon to slash prices on AWS to win business or take other steps that might trade off revenue for strategic reasons. But Amazon needs AWS to keep growing like a weed, in part because it delivers outsized profits for the company. AWS generates one-fifth the revenue of Amazon’s e-commerce businesses, but its operating profits are larger.

The third quarter didn’t look so hot for AWS profits, either. The second consecutive quarter of AWS operating margins at about 25% takes that figure back to 2017 levels.

Amazon investors were fine — thrilled, actually — with Amazon’s project to plow money into faster shipping and its effort to encourage people to buy more goods from Amazon instead of a conventional store. There were signs those endeavors were having the intended effect, at least before the holiday quarter forecast. Amazon tends to be fairly cautious with its outlook, and that may be what’s at play here.

But anxiety is understandable about Amazon. The company’s retail competition is savvier now and has advantages that Amazon can’t match. It isn’t an invincible beast in online shopping. And with a hiccup in growth and margins at AWS, even the one sure thing for Amazon for now doesn’t look so certain.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.