Amazon Is Slowing. Should Investors Worry?

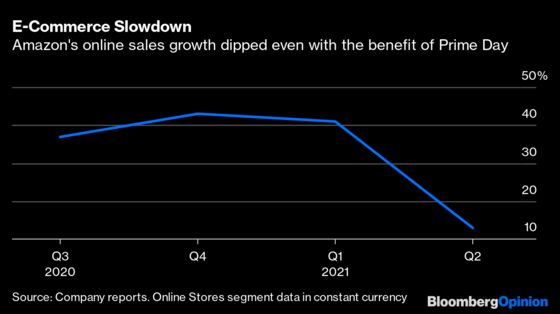

On one hand, e-commerce sales are clearly slowing, foreshadowing more lackluster revenue results the rest of the year.

(Bloomberg Opinion) -- Jeff Bezos stepped down as chief executive officer of Amazon.com Inc. earlier this month after one of the most legendary runs in the history of business. The big question now is whether his successor, Andy Jassy, can keep the momentum going. Judging from the company’s latest earnings results, he has his work cut out for him.

Amazon late Thursday reported second-quarter earnings per share of $15.12, above the $12.28 Bloomberg consensus. The company’s $113.1 billion of revenue in the period was 27% higher than a year earlier, although slightly below expectations of $115.1 billion. But there are signs of bigger weakness ahead. For the current quarter ending in September, Amazon projects revenue growth of 10% to 16%, significantly lower than the 23% average analyst estimate. This subdued forecast sent Amazon’s stock price sliding more than 7% in after-hours trading.

The most recent e-commerce numbers don’t look good. Bank of America credit-card data shows online sales growth so far in July declined from a year earlier after rising 7% in the second quarter and jumping 62% in the first quarter. With Amazon representing about 40% of U.S. online sales, according to eMarketer, there is no way for the company to avoid the overall category drop.

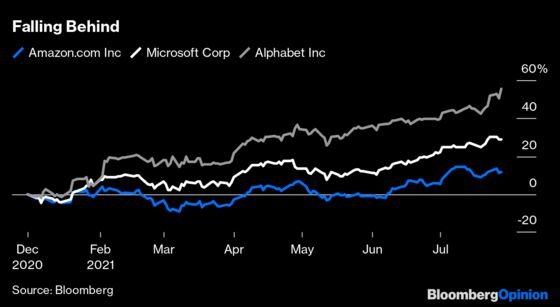

What about Amazon Web Services, the company’s cash cow? The cloud-computing unit that rents computing power to corporations is widely regarded as the technology giant’s most valuable business. But here again, its momentum is slowing relative to the competition. It’s been happening for a while: Amazon’s cloud services grew slower than the overall market and its peers last year, according to Gartner. It happened again in the June quarter, with AWS revenue rising by 37% on a constant currency basis, compared with growth of roughly 50% for Microsoft Corp.’s Azure and Alphabet Inc.’s Google Cloud during the same period. Clearly, AWS’s two main competitors are gaining ground and establishing themselves as credible alternatives. It’s a trend that is not likely to reverse anytime soon.

There are other areas of uncertainty for the coming year. With 1.3 million employees, Amazon faces profit margin pressures if labor pressures force wages higher. Amazon is also likely to face more scrutiny for its anti-competitive business practices from regulators appointed by the Biden administration.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tae Kim is a Bloomberg Opinion columnist covering technology. He previously covered technology for Barron's, following an earlier career as an equity analyst.

©2021 Bloomberg L.P.