Alibaba's Hong Kong Share Sale Presents a $43 Billion Dilemma

(Bloomberg Opinion) -- After its $11.2 billion Hong Kong share sale, Alibaba Group Holding Ltd. will be sitting on $43 billion in cash. That sounds like a great problem to have. Only one publicly listed, non-financial company has more: Apple Inc., at $49 billion.

Then you realize that management literally has more money than it knows what to do with. Chief Executive Officer Daniel Zhang and Maggie Wu, the chief financial officer, have three choices:

- Do nothing. Just sit on that cash in a low-interest-rate world.

- Spend it. On acquisitions and marketing; historically, this has depressed margins.

- Give it back. Dividends, maybe, but more likely, buybacks.

Let’s go through them.

Sitting on that cash is really the easiest, most unimaginative thing to do. But no one says they can’t.

Spending it is definitely in the cards. Alibaba said in its prospectus that it plans to use the proceeds for “driving user growth and engagement, empowering businesses to facilitate digital transformation and improve operational efficiency, and continuing to innovate.”

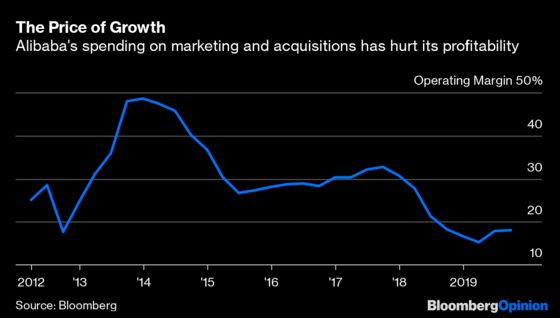

That first point, driving growth, is really just banker-babble for marketing and acquisitions. In the past few years, Alibaba has laid out money for food delivery (Ele.me), groceries (Freshippo), logistics (Cainiao) and others. It’s also spent significantly to battle new rivals like Meituan Dianping and Pinduoduo Inc. This expenditure has been a major reason why top-line growth has stayed so strong. If not for these new revenue streams, Alibaba’s 40% growth last quarter would have been closer to 30%.

That “digital transformation” it talks about includes helping grocery stores getting into delivery (Taoxianda) and building out its still-unprofitable cloud business. Meanwhile, “continuing to innovate” means whatever you want it to mean.

All these initiatives, while strategic and logical, have had the effect of cutting its operating margin in half over the past five years. It’s highly likely that if Alibaba continues spending at this pace, it would do so on less-lucrative businesses that could take even longer to prove profitable.

Which leaves the final option. Return the money.

Pause for a moment to appreciate the irony of a company selling $11 billion of shares to then turn around and buy back shares. Yet Alibaba will be listed on two major bourses — Hong Kong and New York. By using the Hong Kong money to cut the New York float, Alibaba can start to shift its investor base closer to home in China, which was a key purpose of this offering.

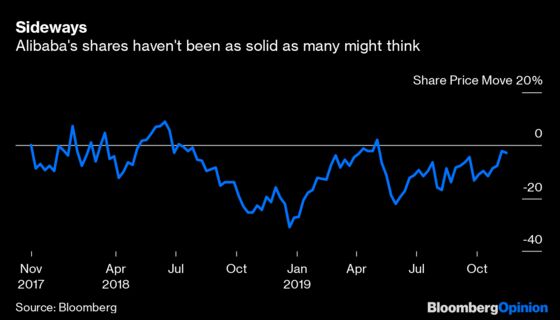

It may sound ridiculous that a company which has climbed 22% over the past year, trades at around 24 times estimated earnings, has a return on capital of 19.7%, and return on equity of 29.8% should consider spending money to prop up its stock. Yet there are two things to consider: Its shares have moved sideways over the past two years, and there’s precedent for solid companies to do this.

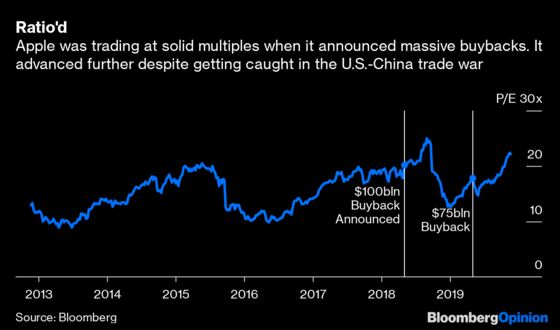

At the time that Apple announced an additional $100 billion buyback in 2018 (on top of more than $200 billion it had already bought in the prior six years), its return on capital was around 21.3% and return on equity around 36%. Its price-earnings of almost 18 times was near historic highs and shares had climbed 23% over the prior 12 months. A year later, it added another $75 billion to the buyback program, despite a further 21% advance in its shares and a widening of those return metrics. (To be sure, much of Apple’s rise has been due to buybacks).

Buybacks can sometimes be seen as a way for troubled companies to prop up their share price, like Baidu Inc., which has dropped 38% in the past 12 months amid falling revenue and profits. Yet plenty of solid companies with great financials do the same, especially when there’s a dearth of better places to put the money. This would signal to Alibaba’s new Hong Kong investors that it’s willing to back them up, and has a war chest to do so.

Sure, Alibaba doesn’t need buybacks. But it doesn’t need $43 billion in cash, either.

That's from removing the "others" category from Alibaba's China Commerce Retail business

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.