Alarms Still Blare on Triple-B Bonds, But No One Cares

(Bloomberg Opinion) -- In the bond market, it can sometimes feel as if the more things change, the more they stay the same.

Consider the following two articles about the massive amount of triple-B rated corporate debt:

-

“A $1 Trillion Powder Keg Threatens the Corporate Bond Market” by Bloomberg News. The takeaway: “A lot of these companies might be rated junk already if not for leniency from credit raters. To avoid tipping over the edge now, they will have to deliver on lofty promises to cut costs and pay down borrowings quickly, before the easy money ends.”

-

“Bond Ratings Firms Go Easy on Some Heavily Indebted Companies” by the Wall Street Journal. The takeaway: “Amid an epic corporate borrowing spree, ratings firms have given leeway to other big borrowers. … The buildup has fueled one of the most divisive debates on Wall Street: Will higher debt loads cause big losses when the economy turns?”

The first one is from October 2018 and the second from a couple of weeks ago. That alone isn’t what’s most interesting — financial-market themes tend to repeat themselves, after all. Rather, it’s the fact that market appetite for those bonds on the brink of junk couldn’t be any more different between then and now, even though it’s clear that fears about ratings inflation and a huge wave of downgrades haven’t gone away.

Around this time last year, Scott Minerd, global chief investment officer at Guggenheim Partners, made headlines by tweeting that “the slide and collapse in investment grade credit has begun,” starting with General Electric Co. No one seemed to want to own bonds rated just a step or two above junk — the Bloomberg Barclays triple-B corporate-bond index trailed the broad market in 2018 for just the second time since the financial crisis. I was willing to be contrarian after his comments, writing that investors shouldn’t fear a doomsday that everyone seems to think is coming.

Still, the rapid change in sentiment through the first 10 months of 2019 has been nothing short of astounding. While there were signs of the tide starting to turn earlier this year, triple-B bonds have now returned 14.4% through Oct. 30, better than any other rating category. If the gains hold through the end of the year, it would be the triple-B market’s strongest performance since 2009, when it bounced back from its worst annual loss on record amid the financial crisis.

Investors have either made peace with the risk of mass downgrades when the credit cycle turns, or they’ve just decided to ignore it and reach for yield when the Federal Reserve is cutting interest rates. Neither seems to be sustainable.

It’s not as if the Wall Street Journal’s recent article is an outlier — CreditSights said in an Oct. 30 report that about $70 billion of triple-B corporate debt is at risk of falling to junk within the next 12 months, including household names like Kraft Heinz Co., Macy’s Inc. and Ford Motor Co. It’s not a question of whether so-called fallen angels become more prevalent, according to the analysts, it’s “when and how fast.”

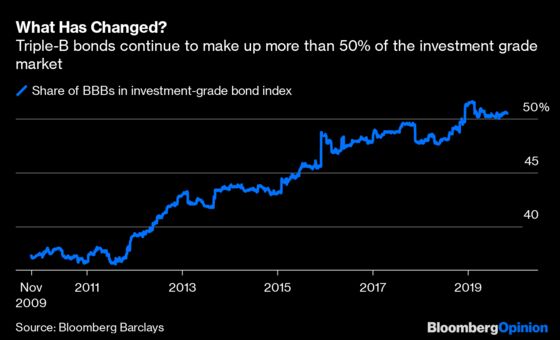

As for the “debt diet” that was supposed to happen this year, which would make triple-B companies less leveraged? In the aggregate, it’s been exactly the opposite. Fitch Ratings, in an Oct. 31 report, noted that triple-B corporate issuance is on pace to reach a record in 2019 after accounting for almost two-thirds of the $515 billion in bonds sold through the first nine months of the year. Triple-B securities make up half of the $5.8 trillion investment-grade corporate bond market, Bloomberg Barclays data show.

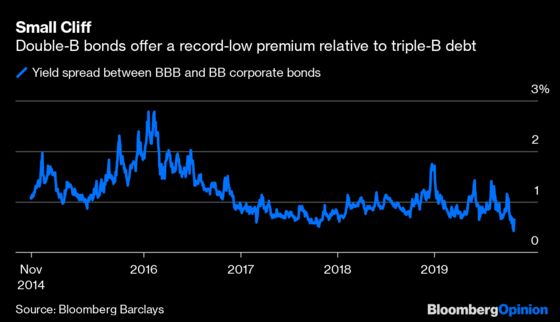

But perhaps the most telltale sign of just how little investors seem to mind the “ratings cliff” between investment- and speculative-grade is how they’re gobbling up double-B bonds just as voraciously as triple-Bs. In fact, on Oct. 28, the spread between the two dropped to 43 basis points, a new low, according to Bloomberg Barclays data. At the start of 2019, it was as high as 172 basis points. Even though triple-B corporate bonds are having their best year in a decade, double-B debt isn’t far behind.

This trend isn’t going to end overnight. Investors poured $2.3 billion into investment-grade bond funds in the week through Oct. 30, and an additional $940 million into high-yield funds, according to Lipper data. The sub-2% yield on 10-year Treasuries is probably still causing sticker shock to some investors, given that until a few months ago it hadn’t breached that level since President Donald Trump’s November 2016 election. For those in Japan and Europe, buying U.S. corporate bonds rather than Treasuries is sometimes the only way to avoid negative currency-hedged yields. Global and structural forces keep investors slamming the buy button in credit markets.

Eventually, though, something has to give, as it always does. For now, corporate-debt buyers are content to just avoid triple-C rated securities. That includes Guggenheim investors led by Minerd, who said in a note this week that “now is not the right time” to add the riskiest junk debt, given the downside potential of more than 20%.

The reasoning makes sense — triple-C rated companies are the most prone to default in an economic downturn. But in such a slump, triple-B companies would be vulnerable to downgrades. If investors were so sure last year that rating cuts would be too much for the high-yield market to bear, why wouldn’t they also stay away from triple-B bonds at this point?

There’s no obvious answer. It’s just a reminder that total returns aren’t everything. Even though triple-B securities are the belle of the ball in credit markets this year, nothing much has truly changed.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.