(Bloomberg Opinion) -- Dan Loeb wants to split up Sony Corp.

In a seven-page letter and 100-slide presentation, Third Point LLC’s founder and CEO outlined what Sony’s shares have been saying for years: The company is worth more than the sum of its parts.

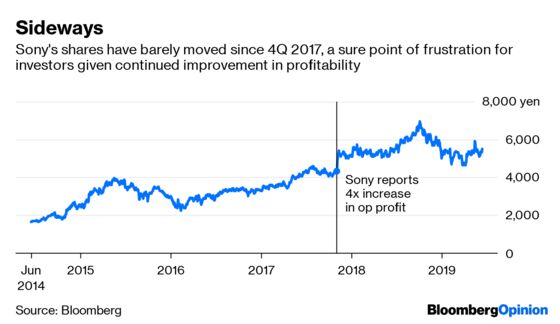

Any Sony investor ought to share the frustration of Third Point, which owns a $1.5 billion stake. After posting losses for six out of seven years, Sony just notched its fourth consecutive annual profit (up 87% in the year through March 31). While this turnaround lifted shares, they’ve remained largely stagnant since the end of October 2017, when PlayStation demand spurred a fourfold increase in quarterly operating profit.

The company’s return on common equity went from negative 5.5% in fiscal 2015 to 27.3% in the most recent year, while its return on invested capital has expanded almost fivefold in the past two years. Yet the shares are trading at a mere 12.6 times estimated forward 12-month earnings, below the 18.6 times for Nintendo Co. and 14.9 times for Canon Inc.

To that end, Loeb’s latest push for change at the Japanese electronics giant includes a request to spin off the semiconductor business and keep core Sony focused on gaming, music and pictures. The mechanics are deceptively simple, and thanks to new tax laws in Japan, potentially quite lucrative.

Sony needn’t run an IPO in the traditional sense of selling some shares in one of its divisions. Instead, it can split into two listed companies: New Sony and Sony Technologies. The latter would house the chip business, and every existing Sony shareholder would get an equivalent stake in both.

To do this, management would need to admit something that’s been clear for a decade: Sony messed up.

Twenty years ago, the company was poised to become what Apple Inc. is today. Back then, Sony owned the portable music market. It invented the Walkman, and when CDs came along it brought out the Discman. The advent of digital music, a catalog of its own, and a range of components to put it all together meant that Sony should have invented the iPod and iTunes. But it didn’t. And, as Steve Jobs proved, you don’t need to own the various parts to dominate the whole.

And yet Sony has held on to these disparate parts far longer than it should have.

In my view, Sony should keep all of its various divisions together if, and only if, there are demonstrable synergies. Samsung Electronics Co. proves that such synergies aren’t only possible but extremely valuable. The South Korean company’s ownership of displays, memory chips and semiconductor manufacturing allows it to keep churning out the best smartphones every year (that is, when they don’t explode).

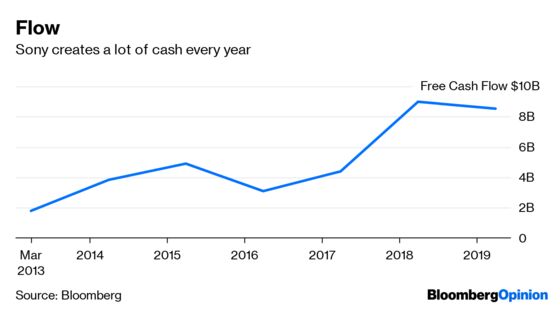

Yet Loeb’s strategy doesn’t adequately address what Sony should do after that. Third Point mentions that post split, New Sony would have room to raise debt, given its inefficient balance sheet, should it need to make acquisitions. It already has $25 billion in total cash, and net cash of $3.6 billion while free cash flow last year was $8.6 billion.

Third Point notes that Sony has the capacity for $34 billion in buybacks over the next three years while keeping net leverage under 1 times. Unfortunately the two buybacks it already announced this year, for a total of 300 billion yen ($2.7 billion), have done little to boost the stock. Perhaps share performance was muted by the tough macroeconomic environment, especially in tech. If that’s the case, then it’s worth noting that a global slowdown and continued U.S.-China tensions aren’t likely to disappear anytime soon.

The case for a reorganization is compelling and shouldn’t be ignored. But both Loeb and Sony management need to spend more time working out what to do with the New Sony.

Third Point notes that one reason for a split would be to allow the new entities to be better compared against appropriate peer groups.

Third Point defines net leverage as net debt/Ebitda.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.