No One Wants to Pay Budweiser’s $10 Billion Bar Tab

(Bloomberg Opinion) -- For a company that built its beer-brewing empire on the back of swashbuckling deals, the future for Anheuser-Busch InBev SA looks pretty unexciting.

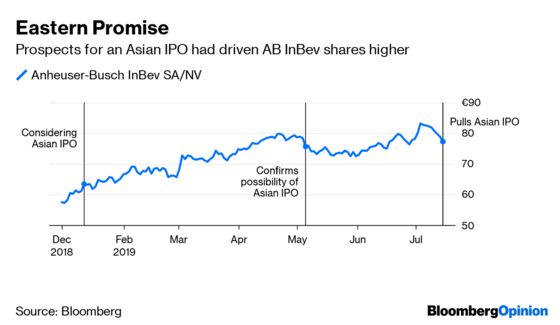

Friday’s decision by the Belgian giant to pull an initial public offering of its Asian unit, which might have raised as much as $10 billion, means it has given up the chance to pay down its $100 billion of debt faster. Perhaps more important, the brewer has lost a valuable source of funding for acquisitions in Asia.

AB InBev had set a punchy price range for the listing, as noted by my colleague Chris Hughes. Even so, the decision to pull the IPO – rather than cut the price – is curious. A survey by Bernstein analysts indicated that there was significant interest among investors at HK$38 per share, which was below the HK$40-47 range but not that much lower. This reduced offer would have generated $400 million less than an IPO at the bottom of the price range, Bernstein notes. For the world’s biggest brewer, with a market capitalization of 157 billion euros ($177 billion), that would have seemed a small concession given the IPO’s considerable benefits.

Without the prospect of the Asia listing, AB InBev has little choice but to knuckle down and gradually chip away at its mountain of borrowings. Net debt stood at $103 billion on December 31. The IPO would have cut the total by about 10%, according to Bernstein, and allowed the company to hit a key debt reduction target a year early. Now net debt will still be 4.2 times earnings at the end of this year. That’s better than the 4.6 times at the close of 2018, but it’s still too high. It underlines the slow pace of reducing the burden.

This doesn’t leave the group much flexibility to do deals. True, the company could gear up further or use AB InBev shares as currency. But neither option is attractive. Investors would be justifiably nervous about borrowings rising even more. The group’s two biggest shareholders, Altria Group Inc. and Colombia’s Santo Domingo family, may not want to be diluted through any deal that was funded by equity.

Cutting the dividend again to speed deleveraging is another option. The group should probably have gone further when it halved the payout in October. Still, such a decision wouldn’t be taken lightly.

While it’s possible the IPO might return to the agenda, it’s hard to see what might change either the company’s or investors’ contrasting views of the Asian business’s value. With the prospects of the listing gone – at least for now – the king of beers is tasting pretty flat.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.