(Bloomberg Opinion) -- Investors who are optimistic about the outlook for the U.S. economy and financial markets due to reports of healthy consumer spending, retail sales and an unemployment rate that held near a 50-year low in August need a history lesson.

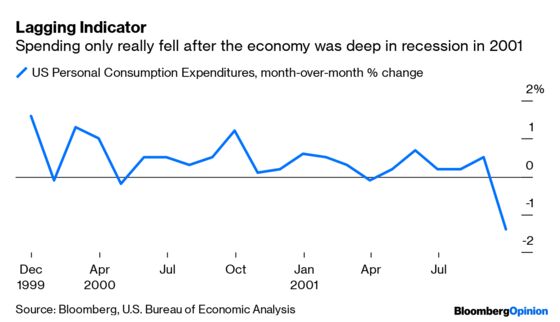

Even though consumer spending accounts for about two-thirds of the economy, it was a poor predictor of the last two recessions, which occurred from March to November 2001, and from December 2007 to June 2009. A slowdown in spending coincided with the start of the first recession and lagged behind in the second.

Although consumers should be viewed as critical to the pace of economic growth, their spending patterns should not be relied upon to provide guidance on the timing of a recession. As such, the strong 0.6% rise in consumer spending for July cannot be taken to mean the economy is on solid ground. This seemingly paradoxical conclusion has important implications for investors.

Economists divide a country’s gross domestic product into four components: expenditures by consumers, investment spending by companies, government outlays and net exports. Of these, consumer spending is by far the most important in the U.S., historically between 65% and 70% of the total. This is why U.S. growth has held up relatively well despite the adverse impact on capital spending stemming from the uncertainties of President Donald Trump’s trade policies.

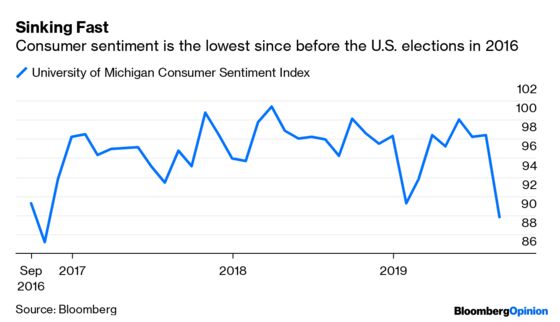

There are signs, though, the consumers are feeling fatigued. The University of Michigan’s Consumer Sentiment Index released last week fell in August by the most since 2012. The Conference Board’s Consumer Confidence Index also posted a steep decline. And this week, the Federal Reserve’s Beige Book economic report covering July and August that is based on anecdotal information collected by the 12 regional Fed banks, described consumer spending as “mixed.”

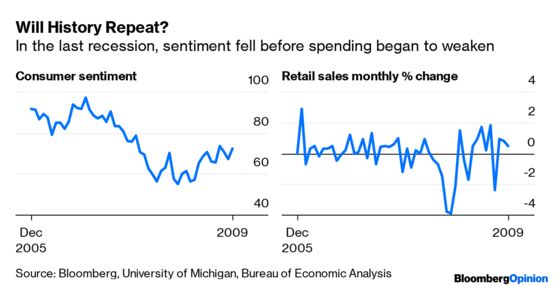

Experience from the Great Recession shows that there is a lag of a several months before adverse consumer sentiment gets translated into reduced spending. Sentiment was still rising until January 2008, but then began to decline before bottoming in November 2008.

Why have consumers largely shrugged off the pessimism toward trade shown by manufacturers? A key reason is that spending is closely tied to movements in equity prices. Equities form a bigger component of retail investors’ portfolios than bonds, and consumer optimism rises and falls with the stock market. The S&P 500 index reached a record high in March 2000, while it’s high in 2006 came in December, both occurring 12 months before the onset of recessions.

The latest escalation in the trade war, with additional tariffs imposed by both the U.S. and China as of Sept. 1, will have a large impact on consumers. Imported food, clothing, footwear and consumer electronics are among the products whose prices will rise once in the U.S. to take account of the new tariffs. Further levies on consumer products are set to become effective on Dec. 15.

Signs of weakness among consumers will become clearer by the start of the new year, meaning U.S. companies will have to decide how much of the price increases they will absorb and how much they will pass on to consumers. Neither option is likely to be positive for share prices.

By the middle of 2020, the vicious cycle of consumers on strike and reduced corporate profitability should be in full bloom. That may mark the beginning of the next recession.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.