(Bloomberg Opinion) -- Chinese billionaire Li Shufu has made a habit of shuffling around the pieces of his sprawling empire to find the best value. Yet none of that grand strategizing has addressed his main problem: a growing pile of debt.

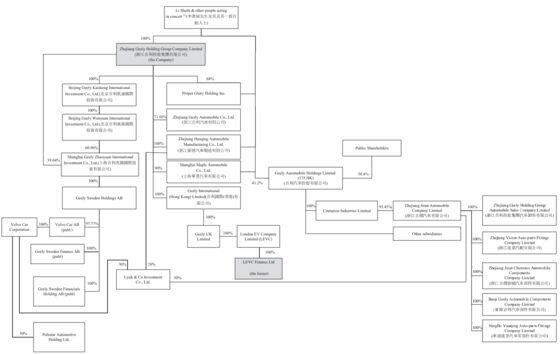

Every few months, Zhejiang Geely Holding Group Co., the parent company of Hong Kong-listed Geely Automobile Holdings Ltd. and Sweden’s Volvo Car AB, comes up with yet another plan for its various subsidiaries. Whether it’s listing them on public markets or monetizing assets, creating new brands to boost valuations or merging various parts and units, the goal, it seems, is often the same: shifting value from one corner to another, and maximizing the efficiency of all the capital that's being put to work.

At this point, most investors have gotten used to these maneuvers, and it isn’t hard to see Li’s motivation. Volvo, his crown jewel, is heading toward an initial public offering by the end of this year that could value the business at around $20 billion. That figure has been a touchy point, and plans for a listing fell through in 2018 because Li and investors couldn’t see eye-to-eye.

But shareholders would do well to look beyond those efforts, and pay attention to the constant tinkering. Those moves will weigh on prospects if Li doesn’t pay down debt at the parent-company level.

In July, Volvo agreed to take control of its part-owned research and development center and manufacturing operations in China from Zhejiang Geely. That came after the companies shelved a plan to merge Geely Automobile and Volvo, which was supposed to help streamline capital spending and production costs. They then carved out a new unit — Aurobay, jointly owned with Zhejiang Geely — to merge internal-combustion-engine operations. The company would become a global supplier of powertrains.

In the same month, Volvo said it intends to raise its stake in electric car performance brand Polestar. The investment in Polestar increased in value as a private placement triggered a valuation effect of 2.0 billion Swedish kronor ($239 million) for Volvo. Bloomberg News reported that Polestar was in talks to go public through a blank-check firm, a SPAC, that could value the combined company at $25 billion.

In January, Zhejiang Geely had divested of its holdings in Polestar and converted it into a wholly-owned subsidiary of Volvo Cars (China) Investment Co.

The common factor in all of this is a reliance on Volvo, Zhejiang Geely’s cash cow. In the years since Li bought the Swedish automaker from Ford Motor Co., he has managed to turn the struggling company around. Now it hands out dividends to its major shareholder and undertakes several related-party transactions with subsidiaries and units tied to Geely. In the first half of the year, Volvo, through its Chinese joint venture, distributed around 4.13 billion Swedish kronor to the parent and 5.97 billion Swedish kronor as part of a special dividend. Operationally, too, Volvo is now the more powerful brand compared with homegrown Geely.

Yet all that value could be at risk given Zhejiang Geely’s mounting pile of debt, at 155 billion yuan ($23.9 billion) at the end of 2020, up from 126 billion yuan a year earlier. Even if Volvo and the listed Geely unit aren’t as indebted, this amount of leverage at the parent level is hard to manage, especially when spending needs continue to increase and capital raising is difficult.

As a recent bond offering document noted, “the Group’s relatively high level of indebtedness and leverage could materially and adversely affect its liquidity,” adding that it could require putting more cash flows from operations toward repaying borrowings, and in turn, reduce what’s available to fund working capital. The elevated debt burden could also limit flexibility, according to the document.

Li can’t reduce debt without equity financing from its various subsidiaries, as S&P Global Ratings has said. Listing the Geely unit on the Shanghai Star Board could have helped with deleveraging, but that fell through. The company is now looking at external financing options for the recently created Zeekr Intelligent Technology unit, one of its electric vehicle brands.

With the Volvo IPO penciled in for the end of the year, Li may find it worthwhile to keep things simple. Paying down debt could wind up getting him closer to the lofty valuations he’s angling for. Other shareholders will be happier, too.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2021 Bloomberg L.P.