(Bloomberg Opinion) -- Ever since the U.K. voted to leave the European Union, Brits have been reaching for the gin and tonic. Now, maybe not so much.

Fevertree Drinks Plc has ridden the wave for premium spirits, selling its classy mixers to a new generation of drinkers. But in its home market, the growth that propelled the company to a peak market capitalization of 4.6 billion pounds ($5.7 billion) last autumn is slowing.

The company reported Tuesday that U.K. sales rose just 5% in the six months to June 30, sending the shares down almost 10%.

Some of this deceleration can be explained by the very strong performance in the year earlier period. In the first half of 2018, U.K. sales rose 73% as Brits toasted a royal wedding and watched the World Cup amid soaring temperatures. This year, unseasonably cold weather in early summer had the opposite effect.

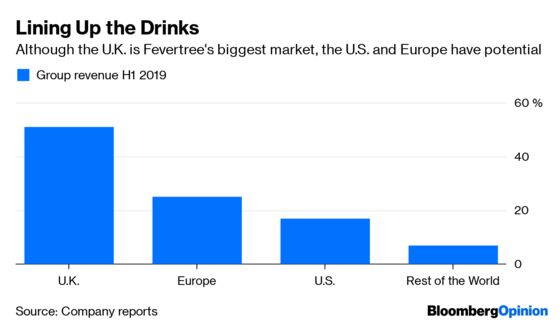

Even so, the trend in the U.K., which still accounts for half of group sales, is a worrying one.

First of all, Brits’ thirst for G&Ts may be waning. Analysts at Jefferies say we may now be close to “peak gin,” making expansion in the category more challenging. The group also now has the number one position by value in the U.K. mixers category in both pubs and retailers. It’s going to be much harder to maintain strong sales growth as an industry leader instead of as a cheeky upstart.

Given the challenging U.K. environment, developing the overseas business is more important than ever. At least Europe has significant potential, given that drinkers there are at an earlier stage in discovering the delights of gin. And the U.S. looks promising – sales rose 24% excluding currency movements in the first half, and the company already has the number one position in the country’s premium mixer market.

But there is a risk that overseas sales don’t compensate fast enough for a British slowdown.

Sales trends across the consumer industry are being disrupted by the stark differences in British weather between 2018 and 2019. It probably won’t be clear for a while yet as to whether Fevertree’s sales growth is really suffering from gin fatigue, or whether this is just a temporary aberration. The company expects the full-year outcome to be in line with its previous expectations.

That's better than it could have been, but its not what investors are used to. The company previously had a habit of upgrading its forecasts when it communicated with the market. That may explain why the shares have been hit so hard, losing close to half of their value since their all-time high last September. Given Fevertree's previous stellar growth, and a valuation to match, any stumble was always going to leave investors with a nasty hangover.

They can still console themselves that Fevertree is just the sort of business that might slot into the portfolios of one of the big beverage or consumer goods companies. They are prepared to pay up for faster growth, but the previous valuation might have made it a difficult sell to their own investors.

Though the shares still trade 45% above peers on a price to earnings basis, that is well below their past premium. Fevertree is still far from a cheap tipple, but for a thirsty buyer, it could slip down more easily.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.