Christine Lagarde's Biggest Problem Is Germany

Lagarde has political skills to try to persuade Berlin to loosen fiscal stance. Sadly, her chances of success are still very slim.

(Bloomberg Opinion) -- Christine Lagarde is still to be confirmed as the European Central Bank’s next president, but work is already piling up on her desk. The euro zone is in danger of becoming the biggest collateral victim of the U.S.-China trade war and Lagarde will need all her political skills to plot an escape route from the threat of recession.

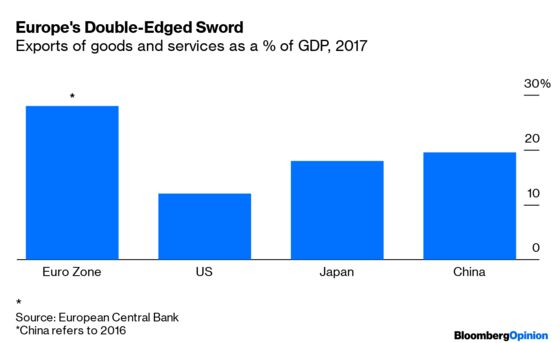

The euro zone is uniquely vulnerable to any blockages in international trade. In 2017, exports of goods and services amounted to 27.9% of its gross domestic product compared to 12.1% for the U.S., according to the ECB. The monetary union had a current account surplus of 323 billion euros ($362 billion), or 2.8% of GDP, in the year to May. While countries such as Germany and Italy might be very different in their commitment to fiscal rectitude – and in how they’re viewed by the bond market – they both share the same export-led model of economic growth.

The euro area faces two big problems in the trade war. First, it can do very little to stop it. Donald Trump and Xi Jinping, the U.S. and Chinese presidents, are calling the shots while Europe’s leaders can only run for cover. True, Jean-Claude Juncker, the departing head of the European Commission, has managed to delay a full-blown trade confrontation between the U.S. and the European Union. Nevertheless, the worsening relationship between Washington and Beijing is weighing on exports and investment decisions in the EU.

Second, the monetary union has few tools with which to combat a trade-induced slowdown. Most people expect the ECB to loosen monetary policy at its next policy meeting, cutting rates further into negative territory. It could also resume its program of net asset purchases. Still, the ECB is in a weaker position than the U.S. Federal Reserve. The American economy’s stronger recovery has allowed the Fed to raise rates in the past few years. That gives it more room to cut if the slowdown persists.

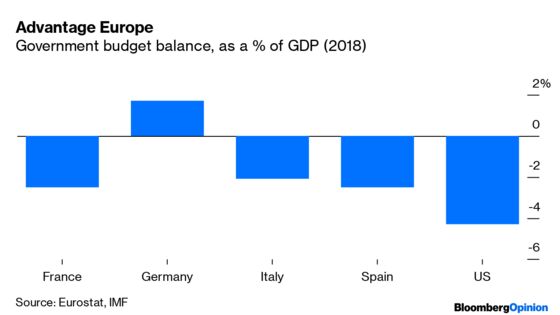

In principle, the euro zone should rely more on fiscal policy, where comparisons with the U.S. are more flattering. Aggregate debt in the bloc was 85.1% of GDP last year, compared to 105.8% in the U.S. Deficit levels are much lower too: A mere 0.5% in the monetary union, against 4.3% in the U.S. Germany enjoys a hefty fiscal surplus.

Yet the political obstacles to a well-designed fiscal stimulus are formidable. Though Berlin might be warming to the idea of borrowing to fund measures to combat climate change, according to a Reuters report, there’s no sign that it’s willing to change its so-called “debt-brake” fiscal rule (which limits its structural deficit to 0.35% of GDP). Any extra climate spending would be welcome but it’s unlikely to be meaningful. If domestic unemployment stays low, German politicians probably won’t feel the urge to open the public purse.

Even if Berlin did change the habits of a lifetime, it wouldn’t solve everything. A chunky stimulus package in Germany would boost the domestic and euro zone economies. But countries in difficulty, such as Italy, would benefit only a little from the cross-border spillover effects of any extra German spending. If the euro area had a centralized budget, it would let it allocate funds where they’re needed most. That would help enormously.

Lagarde’s political skills are sorely needed. On monetary policy the ECB will have to continue with the playbook put together by Mario Draghi, the departing president. This means keeping negative rates as low as possible and restarting quantitative easing if needed. A hawkish tilt, including raising the deposit rate, would be foolish at a time when inflation is below target, growth is stuttering, and European manufacturers need a weak euro.

The new ECB chief’s real challenge will be to convince Berlin that it’s time to take off the spending caps. That alone will require a seismic shift. She’ll also need to make the case for a centralized euro zone fiscal capacity, although that’s unlikely to get very far as long as the rest of the currency area feels countries like Italy might abuse it.

Her chances of success are, unfortunately, slim. The euro zone has a masochistic tendency to act only in a crisis. Europe is walking naked into Trump’s trade war.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.