Every S&P 500 Stock Is Losing to 30-Year Treasuries

(Bloomberg Opinion) -- After spending almost a decade writing exclusively about bonds, it’s sometimes easy to forget just how counterintuitive they can seem to many casual market observers. One survey last year showed just 8% of Americans could accurately define fixed-income investments, while about half of them answered “I do not understand it at all” with regards to U.S. Treasuries, municipal debt and high-yield corporate securities.

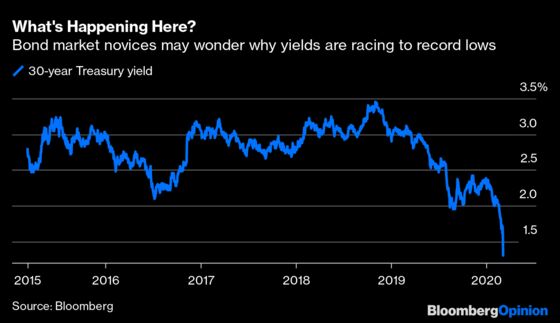

Understandably, those same people might now be confused about what to make of the historic levels reached in the $16.7 trillion Treasuries market over the past two weeks as the coronavirus outbreak intensified. The benchmark 10-year yield dropped below 1% for the first time in 150 years. The Federal Reserve shocked and awed by reducing its key short-term lending rate by 50 basis points in its first emergency interest-rate cut since 2008. Now 30-year Treasuries yield a paltry 1.3%, which is less than the S&P 500’s dividend yield. That had previously never happened since the U.S. government began selling long bonds in the 1970s.

The easiest way to think about these moves is twofold, both from what I’d consider a Main Street perspective. First, it’s cheaper than ever to borrow or refinance if you have strong credit. Rates for 30-year U.S. mortgages have tumbled to 3.29%, down from 3.45% last week and the lowest ever in almost five centuries of data, according to Freddie Mac. Second, individuals should expect to earn less interest going forward from their savings accounts, even the “high-yielding” ones.

But there’s another way to look at the events of the past few weeks, as well as the previous 16 months, through more of a Wall Street lens. While fixed-income investors tend to rightly focus on interest payments, it’s worth remembering that bonds produce total returns just like stocks and other asset classes. And the results have been nothing short of remarkable.

Since early November 2018, when the 30-year Treasury yield peaked at 3.4647%, long bonds have returned 52%, according to ICE Bank of America Corp. index data through March 5. That’s better than almost 90% of the S&P 500 Index. The gain exceeds the overall equity index, which is up just 18%, as well as other safe haven assets like gold (up 32%). Unless you went all-in on Tesla Inc., which has soared more than 100%, you would have been hard-pressed to find a higher-flying investment than the longest-dated Treasuries.

Rapid price appreciation, of course, is not what Treasuries are known for. Despite the huge swings in recent days, bonds on a whole tend to be less volatile than equities.

That means on a risk-adjusted basis, 30-year Treasuries look even better. So much so, in fact, that no company in the S&P 500 Index has fared better since November 2018. That’s right, when taking both total return and volatility into account, long bonds have bested all 500 of the S&P 500 companies (and Tesla, too).

Here’s a chart of the few companies that come close to 30-year Treasuries in risk-adjusted returns:

The 3% cutoff is interesting in part because it’s right around the same yield on Treasuries that helped spark a steep equities sell-off in late 2018. While a number of investors were calling for yields to only climb further, there was ample evidence at the time of record demand for long-duration assets — precisely those that would gain the most from falling interest rates. It also served as a giveaway in retrospect that bond bears couldn’t get their stories straight.

Hindsight always delivers great returns, of course. Heading into this year, no investor was perfectly positioned for a potential pandemic that could send the global economy into a recession. But that’s what’s reflected in a 0.75% 10-year Treasury yield. And don’t let a simple comparison between bond yields and the S&P 500 dividend yield fool you — if an economic slowdown is in the cards, no matter how small, equities will fare worse than government securities.

Yes, it hurts now to think about missing out on 3% Treasury yields. Bloomberg News’s Cameron Crise asked on Twitter when the 30-year bond would next trade at that level. More than half of the 173 responses said “after 2024” or “never.” It probably stings even more to consider the prospect of sitting on a 50% gain with seemingly little on the horizon that could eat into those profits.

But at least it serves as a valuable lesson about bond markets for those who don’t understand fixed income. Structural forces like a huge buildup in government and corporate debt since the financial crisis have made higher borrowing costs untenable. Relentless demand for safe assets from retirees with longer life expectancy also helps to keep a lid on benchmark bond yields when interest rates are rising, and to send yields tumbling during episodes of fear, like markets have witnessed in the past two weeks.

Simply put, it seems abundantly clear now that yields need not revert to longer-term averages. That’s a lesson that has humbled even bond-market veterans.

This naturally depends on the time horizon. But as an example, it took about five-and-a-half years for the S&P 500 to climb back to its pre-financial crisis peak and it took a similar stretch to rebound from the bursting of the dot-com bubble. Treasuries delivered steadily positive returns.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net, Beth Williams

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.