(Bloomberg Opinion) -- Another earnings report, another guidance cut. What else did you expect from 3M Co.?

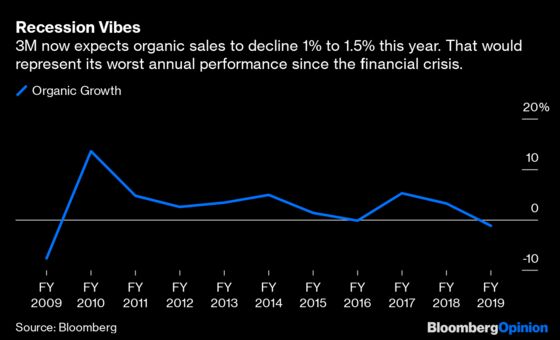

The $93 billion maker of Post-it notes and industrial adhesives lowered its earnings and revenue forecast for 2019, with Chief Executive Officer Michael Roman on Thursday citing a “challenging” macroeconomic environment. Roman has been in his role since July 2018, and he’s had to cut the company’s outlook in some way during every quarter of his tenure but one. The exception was this year’s second quarter, when 3M maintained its forecast for 2019 sales to grow as much as 2%, absent the impact of currency swings and M&A. That depended on a stabilization in China and automotive markets; unsurprisingly, that didn’t materialize, and Thursday’s deep guidance reduction shows the company would have been wise to be more cautious. 3M now expects sales to at best decline 1% for the full year. That will be its worst showing since 2009.

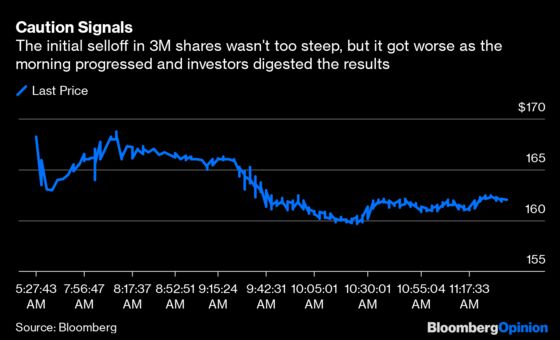

The series of guidance cuts under Roman has been sloppy and, at times, illogical. His initial 2019 forecast called for organic sales growth of as much as 4%, even as economic data pointed to a cooling in manufacturing demand. It’s telling that 3M shares initially fell only about 1% on this latest earnings miss. No one really believed Roman when he said in July that 3M’s guidance was still realistic. That lack of credibility should be troubling for the company.

But the fact is, there’s a lot to be concerned about in this latest disappointment, both for 3M and for the broader economy, and the stock slumped 5% as investors dug into the numbers more closely. The guidance cut reflects in part a 15-cent per-share negative impact from 3M’s $6.7 billion takeover of wound-care company Acelity Inc., which closed earlier this month. But even when you back that out, the magnitude of the outlook reduction is severe. 3M anticipates fourth-quarter organic sales may decline as much as 3%, a sharp shift from a 1.3% slide in the third quarter that was already worse than analysts had expected. Looking at the U.S. as a region, organic sales declined 1.1% in the three months ended in September, compared with a 0.1% gain in the second quarter. In Asia, sales slumped 4.4% on the same basis in the third quarter.

It doesn’t take long for 3M’s products to go from the factory to the end customer, so it’s on the front lines of any economic weakness. Thursday’s earnings report offers troubling fresh evidence that the current manufacturing slowdown is accelerating and deepening. This follows the first quarterly earnings decline in nearly three years at another industrial bellwether, Caterpillar Inc., on Wednesday, though its commitment to cut production and other costs to adjust to the weaker demand environment helped offset investors’ concerns about its downbeat profit and sales outlook. Also on Thursday, toolmaker Stanley Black & Decker Inc. cut its full-year earnings guidance below even the lowest analyst estimate and announced a new $200 million cost-cutting plan. That’s on top of a “margin resiliency” program focused on using digital technologies to improve profitability by $300 million to $500 million by 2022.

3M lacks the same kind of promise of margin protection. Because of the Acelity deal, 3M has reduced its planned share repurchases for 2019. Meanwhile, its acquisition of artificial-intelligence platform M*Modal for $1 billion earlier this year and other growth investments are pressuring margins in the health-care division. 3M announced a $225 million to $250 million restructuring plan in April, but it’s still grappling with inventory pullbacks in its more industrial-facing units as nervous customers worry about the sustainability of demand. Economic weakness plays a role here, but there are also signs of operational foot faults. Adding another earnings disappointment to CEO Roman’s resume won’t help 3M fix the perception that its days as a safe bet are over, and not soon to return.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.