(Bloomberg Opinion) -- When the world’s biggest health crisis in a century struck in February, central bankers and politicians rushed to protect their economies. The devastation of lockdown threatened even the soundest financial firms, whose collapse would have worsened the crisis.

But the trillions of dollars plowed into companies and households, accompanied by the easing of regulatory demands on lenders, didn’t merely ensure the financial system was cushioned from the shock. For some pockets of global finance, having oodles of fresh liquidity has been a massive boon — even as economies crumbled.

Plenty of banks have been doing rather well, and getting bigger. Bolstered by strong capital and cheap funding, 2020’s winners should ride the wave of monetary expansion in 2021, even if economic growth might take years to recover. Granted, the trajectories of the pandemic and the economy remain uncertain. Accommodative policies could be curtailed before a vaccine has properly taken effect. Nonetheless, the odds are skewed in favor of financial firms that facilitate and manage this huge gusher of liquidity.

Big trading operations have been the chief beneficiaries. Since the Lehman crisis, trading has been concentrated in fewer banks, widening the gap between the finance industry’s haves and have nots. This year’s bursts of volatility, enormous market rotations and soaring asset values have rewarded Wall Street with unprecedented revenue. In the first nine months, trading income at the top-10 firms rose by about a third, according to McKinsey & Co, with the U.S. giants taking more market share from their few remaining European rivals. JPMorgan Chase & Co., the biggest Wall Street beast, says its revenue is on course to rise by 20% in the fourth quarter.

While securities firms aren’t budgeting for a repeat of 2020’s bonanza next year, investment banking revenue should still look much better than it did in 2019, when the business appeared to be on a relentless downward trend.

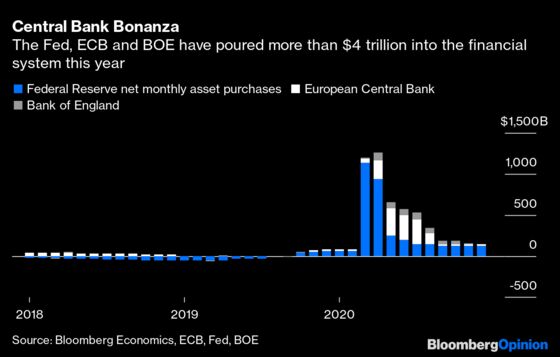

Conditions remain ideal for bankers. Record debt sales this year will lead to more refinancing. Governments continue to unleash economic support and central banks keep easing monetary policy. As the rollout of vaccines begins, economic optimism is awakening animal spirits. M&A is rebounding sharply. Financing and capital-markets activity should follow.

In one of the bolder trading forecasts for 2021, Deutsche Bank AG says its revenue should be down only “slightly” next year, when compared to 2020’s rip-roaring sales performance. Even if central banks reverse course, it’s quite possible that market swings and the readjustment of portfolios could spur more trading activity.

Should the economic recovery stay on track, it’s not just companies that will put savings to work. Investors too are whittling down the deposits they built during the pandemic, shifting from cash and cash-like instruments into riskier products. That injection of fresh money into bonds and stocks, and increasingly into higher-yielding private markets, could add to the value of fund-manager holdings. Assets at BlackRock Inc., the biggest money manager, rose to an all-time high in the third quarter.

At the richer end of the industry, millionaires and billionaires have been pumping funds into wealth managers. As asset prices rebound, many are turning to banks for ways to protect their savings with complex, bespoke products, or to borrow against their wealth. Morgan Stanley, Goldman Sachs Group Inc. and JPMorgan are all focusing on asset and wealth management. That’s a sign of where the industry’s growth will come: Global wealth is expected to keep outpacing GDP expansion.

Meanwhile, U.S. consumers are armed with $1 trillion of excess savings, according to Greenmantle, a consultancy. For finance firms, a spending splurge would translate into transaction fees and interest on credit card balances.

This isn’t to say that a banker’s life is trouble free, including the titans of finance. The decline in interest rates is damaging to lending margins, even if borrowings grow strongly. Net interest income at the four largest U.S. banks dropped to its lowest level in more than five years in the third quarter. McKinsey estimates that by 2024 banks globally might see revenue trailing 14% lower than estimated before the pandemic because of rock-bottom rates.

Another worry is that defaults and loan delinquencies are just beginning to materialize as some government support measures taper off. Unless banks have provisioned cautiously in 2020, it could take another blockbuster trading year to offset the pain of lower lending margins and higher loan charges. A permanent post-pandemic slump in commercial property — to which banks are significantly exposed — would pose a serious risk.

Plus the shift to digital banking, and the fascination with cryptocurrencies, will increase competition and require heavy investment. In asset management, the primacy of passive funds will put pressure on fees and force banks to bulk up through acquisition.

In the U.S., the Biden administration might be tougher on financial services than President Donald Trump. In Europe, Brexit threatens to fragment markets and slow the U.K.’s recovery, which would lead to bigger loan losses.

However, any pain won’t be felt equally in finance. Lenders to small and medium-sized companies, for example, could suffer more. Witness the consolidation among banks in Italy and Spain. For the dominant players, the pandemic fixes will yield more bounty.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2020 Bloomberg L.P.