(Bloomberg Opinion) -- Two things happened around 9:30 p.m. New York time on Tuesday as U.S. election results came pouring in:

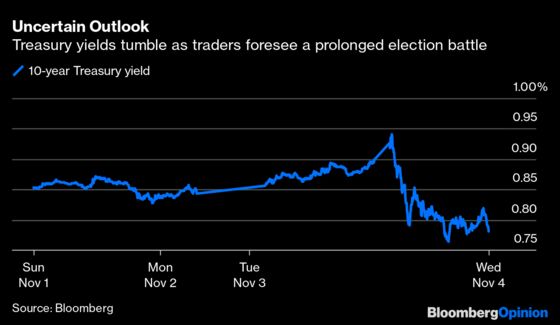

- The 10-year Treasury yield extended its decline, touching 0.79% from as high as 0.94% about two hours earlier.

- The odds of President Donald Trump winning re-election jumped to 71% from about 32% on Betfair.

Predictably, the second move received more attention, even though Betfair is a sliver of the size of the world’s biggest bond market. After all, it seemed to reflect a dramatic shift that expressly captured bettors’ views on who would come out ahead in the presidential election. U.S. equities even began rallying in tandem with Trump’s improving odds after previously soaring on the expectation that Democrat Joe Biden would emerge victorious and usher in a “blue wave.”

In hindsight, everyone would have been better off interpreting the clear signal from the huge rally in the $20.4 trillion Treasuries market: That this election has all the makings of a prolonged and contested affair. Long-term yields don’t fall 10 basis points or more simply because one party is more likely to have control of the White House. Treasuries rally like that only when there’s an unexpected rush to havens — that is to say, when there’s no clarity and investors are nervous.

So it’s little surprise that Treasury yields fell even further after Trump falsely claimed victory and said “we’ll be going to the U.S. Supreme Court. We want all voting to stop.” While this gambit was telegraphed well in advance, it’s nonetheless unnerving for investors to see the world’s oldest democracy tested in such a way. It might take days before states such as Pennsylvania report final results, and even then, there could be challenges and recounts. Don’t expect 10-year yields to test 1% under such a cloud of uncertainty.

In reality, just about every state was more or less within the margin of error of polling expectations — it was simply that markets got a bit too eager to price in a “blue wave” scenario in recent days. The crucial battleground states of Wisconsin, Michigan and Pennsylvania appeared to favor the president early, but that mainly reflected Election Day votes, which tend to skew Republican. The unusually large number of absentee ballots cast because of the coronavirus pandemic, which lean Democratic, are still being counted there. Biden has already overtaken Trump in Wisconsin and Michigan.

This trend was known in advance, though it’s fairly obvious that denizens of the election betting markets didn’t have a full understanding of this phenomenon. Jim Bianco, president and founder of Bianco Research, posted this map of PredictIt odds soon after 11 p.m. New York time, which showed Trump favored to sweep the Midwest battlegrounds:

As of this morning, Biden is not only competitive in two of those three states, but also in Georgia, where the New York Times’s “needle” now gives the former vice president a razor-thin edge. When combined with leads in Nevada and Arizona and a pickup in Nebraska’s Second District, there are any number of ways for Biden to come out ahead.

Perhaps in a reflection of this shift, the 10-year Treasury yield climbed almost 5 basis points from its low, to 0.81% at 7:30 a.m. in New York, only to dive yet again to 0.76% by 9:20 a.m. Again, the craving for certainty above everything else is readily apparent here. A Biden presidency, combined with a Republican-controlled Senate and a weakened Democratic House majority, isn’t exactly a recipe for the kind of fiscal stimulus that investors were imagining in their Democratic sweep scenarios. In fact, depending on whether you view Senate Majority Leader Mitch McConnell or House Speaker Nancy Pelosi as more obstructionist, this configuration is potentially the worst option for a fiscal jolt to the economy.

The only worse option in the eyes of bond traders, it seems, is a bitterly contested election. America might yet avoid that fate, but it certainly doesn’t seem as if there will be a concession speech soon, either. As long as the country doesn’t know its next president, expect Treasuries to be a hot commodity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.