(Bloomberg Opinion) -- H2O Asset Management just filed the semi-annual report for one of its funds. It makes for fascinating reading, particularly if you happen to be a regulator concerned about investment products that offer clients daily redemption while at the same time as dabbling in hard-to-trade debt. If you’re a customer, however, you might want to question again what H2O has been doing with your money.

A quick recap. In June, the Financial Times reported that H2O, one of Natixis SA’s asset managers, had stuffed its portfolios with bonds sold by companies related to German entrepreneur Lars Windhorst. The hard-to-trade nature of those securities prompted Morningstar to suspend its rating of one of H2O’s funds; by the end of the month, investors had pulled almost 8 billion euros ($8.8 billion) from them.

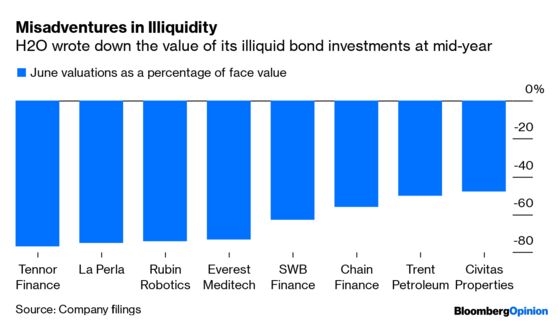

On June 24, Natixis said the fund had switched to “record these securities at their transactional value in case of an immediate total sale, rather than recording them at their standard market value.” It turns out that those transactional values are way, way below their face values.

Those figures are for the bonds in H2O’s Multibonds fund, and are for valuations assigned on June 28 – just over a week after the FT first detailed the asset manager’s excursion into illiquid debt. The Windhorst-related companies that sold the bonds include Italian lingerie maker La Perla and German residential real estate company Civitas Properties.

The website for H20, which managed $32.5 billion at the end of 2018, doesn’t yet list the semi-annual reports for its other funds. But it’s clear that the more than 1 billion euros that the firm had lent to Windhorst by mid-year had been written down by between half and three-quarters.

One of the steepest drops is for Tennor Finance BV, Windhorst’s renamed holding company, which was previously called Sapinda. H2O says the 100 million euros its Multibond fund owns of Tennor’s 5.75% notes repayable in 2024 are worth just 23.41 million euros. Data compiled by Bloomberg show that the notes were issued at 100% of face value on June 17 – less than two weeks before H20 revalued them at a discount of almost 77%. That’s a remarkably swift deterioration by anyone’s standards.

Even the Tennor reappraisal, however, isn’t the biggest value drop H20 has suffered on its holdings. That honor is reserved for $155.5 million of bonds issued in June 2018 by ADS Securities, an Abu Dhabi brokerage firm. As of March, H20 owned $128 million of the issue, or 82% of it, after increasing its holdings twice from an initial $78 million in mid-2018, according to data compiled by Bloomberg.

The Multibonds fund owned $15.55 million of face value of the securities as of the end of June. H2O lists them as being worth $3,343,483.52 – an impressively precise figure for a bond that appears never to trade. That marks a drop of almost 80% from their face value.

ADS Securities is the only company that H2O has bought illiquid bonds from that Windhorst doesn’t own. But, as my Bloomberg News colleagues Sridhar Natarajan and Luca Casiraghi reported on June 27, ADS was entangled in a failed trade involving Windhorst, H2O and Goldman Sachs Group Inc. in 2016.

In response to questions about the ADS bond investment, an external spokesman for H20 referred to a June statement, which said that the illiquid bonds bought by the fund “have indeed been referred to us by Lars Windhorst.”

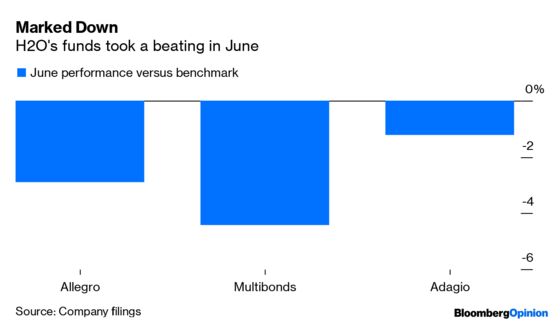

For H2O’s investors, those writedowns appear to have dented performance in June, the most recent month for which returns data is available on the company’s website. This chart shows the extent of the damage:

H20 may end up being rewarded for its bravery. The illiquid bonds it owns are all scheduled to mature in the coming five years, and carry interest rates of between 4% and 8.25% – coupons that look increasingly attractive in a world where negative rates are increasingly the norm. And the year-to-date performance of its funds looks to have improved since mid-year. Moreover, the firm plans to create a new fund specifically designed to own what it calls “deep value” securities.

But the speed and the severity of the markdowns is evidence that the greater rewards offered by hard-to-trade securities come with elevated risks – risks that the regulators may decide are higher than funds that offer daily redemption should be allowed to bear.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.