(Bloomberg Opinion) -- Economists have long hated the mortgage interest deduction, but U.S. politicians have long considered it untouchable. Then, in 2017 — after much wrangling and over the objections of several suburban members of Congress — Republicans capped the deduction as part of the Tax Cut and Jobs Act.

Now there is some new evidence on the effects of that law — and the case for entirely eliminating the mortgage interest deduction just got a little stronger. Not only would its elimination free up revenue for other priorities and simplify the tax code, it is unlikely to have a negative effect on homeowners.

After 1986, when Congress eliminated the deductibility of interest on personal loans and increased the size of the standard deduction, the mortgage interest deduction was on life support. Add in the factor of declining interest rates, and the deduction was nearly useless for the vast majority of taxpayers.

The National Association of Realtors responded with a media campaign warning Americans that any effort to cut the deduction would mean the end of the American Dream. Congress abandoned the effort. Over time, home prices have steadily risen, and the deduction has become enshrined as an untouchable middle-class benefit.

Even the 2017 effort was a compromise. House Republicans wanted to cap the benefit at the first $500,000 of a mortgage balance. The Senate raised the cap to $750,000 and grandfathered in existing homeowners.

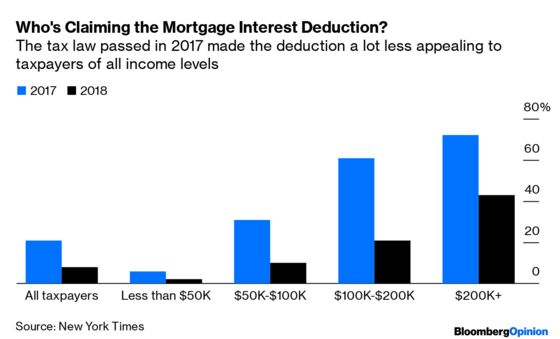

The $750,000 limit was set so that the deduction would hit primarily the jumbo mortgage market. At the time, one prominent study estimated that only 14% of taxpayers would find it worthwhile to claim the deduction.

Yet as the New York Times reports, citing IRS data, only 8% of taxpayers claimed the deduction in 2018, compared to 21% in 2017. Even more important, the percentage of taxpayers earning $100,000 to $200,000 annually who claimed the deduction declined from 61% to 21%. For upper-middle-class families, the mortgage interest deduction went from being a benefit for the majority to one for a minority.

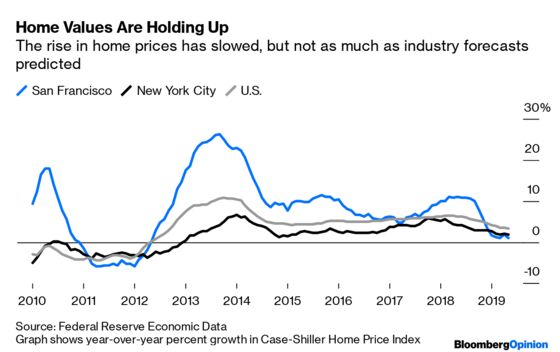

Yet away from the coasts, there has been little price paid — politically or economically. The new law seems to have had only a modest effect on home prices. In San Francisco and New York City, the rise in home prices has slowed, but prices have not fallen as far as the industry predicted.

Nonetheless, the National Association of Realtors is lobbying to weaken the effects of the 2017 tax reforms — even though the evidence shows that the cap is both more effective than proponents hoped and less damaging than opponents feared. Congress should act now to completely eliminate the mortgage interest deduction before the movement to revive it gains any steam.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a former assistant professor of economics at the University of North Carolina's school of government and founder of the blog Modeled Behavior.

©2019 Bloomberg L.P.