Sports Direct Billionaire Mike Ashley Spins Out of Control

(Bloomberg Opinion) -- A year ago, Mike Ashley was being hailed as a possible savior of Britain’s rapidly depopulating shopping districts. Now, after the comically delayed announcement of his company’s annual results last month, the colorful sportswear billionaire looks like just any other struggling retailer.

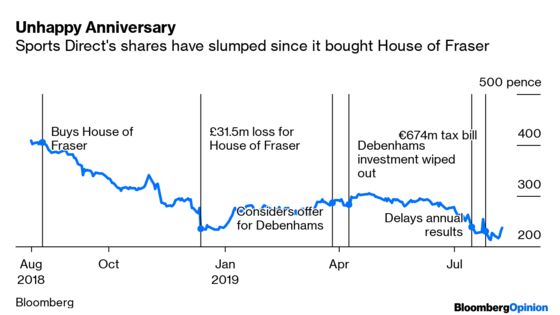

It’s 12 months since his Sports Direct International Plc struck a deal to acquire the ailing department store chain House of Fraser. Ashley, who had long stalked the business, now regrets the move. The acquired business has had an instantly negative effect on the wider group, which showed up starkly in its results statement.

House of Fraser’s poor trading shouldn’t really have surprised anyone after years of chronic under-investment. Add in supplier problems and cautious consumers and it racked up more than 50 million pounds ($61 million) of losses from August to the end of Sports Direct’s financial year on April 28. Ashley is even losing money on House of Fraser stores where he’s paying no rent.

While this hasn’t turned out to be the “Harrods of the high street” of Ashley’s dreams, he did at least manage to limit some of his financial exposure. Sports Direct paid 90 million pounds for the assets, and invested a similar amount in working capital, but it did pick up House of Fraser’s shop stock too. That might have been worth more than the purchase price.

Ashley was never likely to keep all of House of Fraser’s stores. He’s still planning more upmarket outlets in Glasgow, Belfast, Liverpool and Newcastle. He’s keen too to sell more of the designer labels that have made his Flannels chain of smaller stores a hit, so having bigger flagship department stores will help. Many House of Frasers will probably be closed though.

Ashley, who’s been targeted by U.K. politicians before because of his employment practices, can legitimately say he’s tried to save jobs. But turning around a chain with “terminal” problems (his words) was just too difficult. While he will no doubt be criticized, stemming financial losses and making Frasers – the new name for the high-end chain – smaller and higher quality make sense.

Nevertheless, even this more limited ambition is a huge challenge, and his company has problems elsewhere. Its strategy of improving the attractiveness of its core Sports Direct stores – known for their “pile ‘em high and sell ‘em cheap” approach – hasn’t gained traction yet. Nike and Adidas are still reluctant to supply it with the latest sneaker models.

An unexpected 674 million euro ( $754 million) tax bill – which caused that embarrassing delay in the results – was another unwelcome surprise and smacks of a group that’s spinning out of control. Indeed, Sports Direct’s management has been stretched thin by a string of Ashley investments that have also included Game Digital, a video game retailer, and Jack Wills, a struggling apparel supplier to affluent teens. This has been compounded by the departure of key executives, including the head of retail Karen Byers.

In the current climate, Ashley’s strategy of having lots of high street property, in which he can drop different brands (which he usually buys on the cheap) appears sensible. In a distressed market, why not try to take advantage of the misery elsewhere? He might still take a fresh tilt at Debenhams, another British department store chain that’s now owned by a group of lenders and hedge funds.

But Sports Direct appears to be fighting fires on too many fronts. Investors, who have pushed the shares down by 42% in a year, are right to be skeptical. Ashley has to win over the big brands for his Sports Direct chain, and some luxury names at House of Fraser. Given the history of his stores, that won’t be easy.

While net debt is forecast to remain an undemanding 1.5 times in the current financial year, according to analysts, and the Sports Direct chain still generates cash, upgrading stores and making strategic investments isn’t cheap.

As I’ve argued before, Sports Direct would be better off as a private company. Ashley, who owns 62% of the shares, says he has no intention of doing this because without outside shareholders he would be “uncontrollable.” But it’s hardly as if he’s been reined in by the demands of being a listed company.

As it is, minority investors have little option than to hope he makes the right choices from here. There may yet be method in the Ashley madness, but he needs to prove that the last year wasn’t all just folly.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.