(Bloomberg Opinion) -- Buy the rumor, sell the news – especially when the news is a lower-than-expected takeover offer.

Shares of Wabco Holdings Inc., a Michigan-based maker of brakes and truck-safety systems, fell more than 10 percent on Thursday after it agreed to sell itself to ZF Friedrichshafen AG for about $7 billion including debt. It’s rare that you see a target falling on news of an actual deal; even oft-speculated subjects of on-again, off-again takeover talks such as Wabco tend to get a day-of bump. Not in this case: ZF is offering Wabco holders $136.50 in cash for each of their shares, a premium to where the company was trading in February before reports first emerged of deal talks, but a 6.5 percent discount to where it traded as of Wednesday. The shares even fell below the purchase price as traders baked in a buffer for regulatory risk and the fact that the deal won’t close until early 2020.

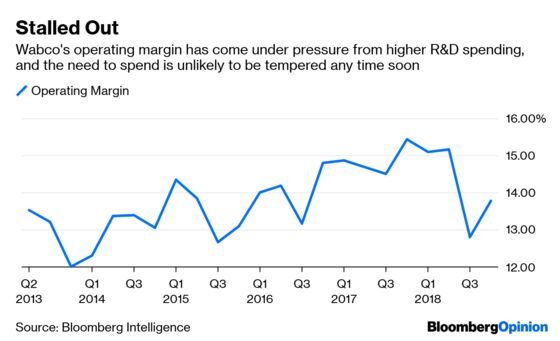

The price works out to just over 11 times Wabco’s expected Ebitda in 2019. That’s a lower valuation than analysts from Citigroup Inc., William Blair & Co. and KeyBanc Capital Markets Inc. saw as appropriate in a takeover and short of Wabco’s historical average over the past five years. But before the prospect of a deal came on the scene, analysts on average were expecting Wabco shares would climb only as high as $127.25 on their own over the next year as higher engineering spending crimped profit margins.

Wabco’s focus on safety and automation technology for self-driving vehicles insulates its revenue growth somewhat from a broader trucking market slowdown, but Piper Jaffray Cos. analyst Alexander Potter takes its execution issues of late as evidence that the company isn’t able to pursue these new opportunities as profitably as it has in the past. And in that case, as I’ve written before, Wabco is better off as part of a larger company with a bigger budget.

“This is the right combination at the right price at the right time,” Wabco CEO Jacques Esculier said in a statement that seemed carefully crafted to anticipate some frustrated shareholders. “It has become increasingly apparent that our industry will face a new level of strategic complexity and will attract new competition, including new entrants from outside the sector, able to bring unprecedented resources to the table.”

As a closely held company that’s controlled by the Zeppelin Foundation and a private German family foundation, ZF has more leeway to invest in electric and autonomous-driving technology. It knows that it needs to, lest the legacy transmissions at the heart of its product portfolio become obsolete. ZF vowed last year to spend 12 billion euros ($14 billion) over the next five years on projects including the development of a battery-powered delivery van that can drive on its own. ZF expects self-driving technology to work best in commercial vehicles operating in low-traffic areas such as factory sites and airports; Wabco’s braking systems will be essential to advancing that effort and guarding against unforeseen obstacles and accidents. Piper Jaffray’s Potter thinks it will be nearly impossible for truck makers with self-driving ambitions to avoid buying from the combined Wabco and ZF.

You could see how this might still be frustrating for Wabco shareholders, however. Because ZF has no public stock it can use as a currency, Wabco investors’ ability to participate in this glorious future is capped at their $136.50 per share payout. While you can never rule out a competing offer, the odds seem low as Wabco and ZF reportedly held advanced deal talks in 2017 before reconnecting this year, leaving ample time for someone else to make a bid. Should Wabco shareholders choose to push for a higher price from ZF, however, they would seem to have grounds to do so.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.