Verizon’s Slump Raises a Tough Question About T-Mobile-Sprint

(Bloomberg Opinion) -- If regulators want proof that the merger of T-Mobile US Inc. and Sprint Corp. will ultimately be harmful to consumers, Thursday’s wireless industry sell-off may be it.

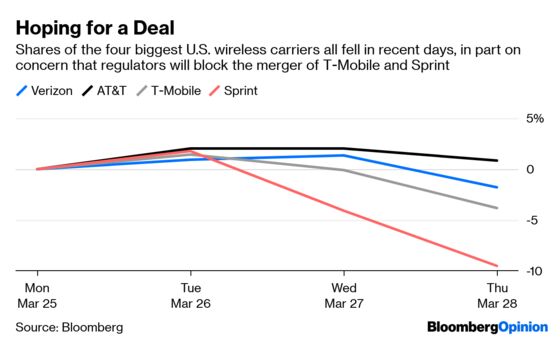

Shares of Sprint tumbled about 6 percent as of 2:45 p.m. New York time, while T-Mobile fell 3.8 percent and AT&T Inc. slid 1.5 percent. Verizon Communications Inc. dropped the most since January in what was the second-worst performance among S&P 500 members.

The sudden dimmed outlook may be tied to press reports revealing the difficulty T-Mobile and Sprint are having in getting their deal across the finish line. On Wednesday, DealReporter said that the New York attorney general’s office is working with 17 other state attorneys general in preparing to oppose the transaction, which is valued at $59 billion (including debt). Then on Thursday, Bloomberg News reported that some U.S. officials vetting the deal remain skeptical of the companies’ argument that Sprint will be too weak on its own if it’s not allowed to combine with T-Mobile.

T-Mobile and Sprint have been arguing that by joining forces they’ll have greater ability to keep prices low — and build a nationwide 5G network to aid the U.S. in its race against China. Democrats in the House and Senate have voiced concern that instead, the merger will lead to higher prices for consumers.

For years, T-Mobile and Sprint have been the low-cost carriers keeping the marketplace competitive, and they effectively pressured their larger rivals, AT&T and Verizon, into offering unlimited data plans. Critics of the deal are worried that dynamic will no longer exist if the industry is reduced to three players. The fact that Verizon and AT&T are falling alongside T-Mobile and Sprint may support that case. It’s at least evidence that investors expected consolidation to be a boon for all the companies’ bottom lines, meaning they saw renewed pricing power.

AT&T’s CEO, Randall Stephenson, tap-danced around this point when asked about his rivals’ transaction during an interview last week on stage at the Economic Club in Washington. “I have to be cautious because if I say that the deal ought to get done, that would be a death knell for it,” he said, because his remarks could be taken as proof that the merger is anti-competitive.

I still think whether it gets approved is anybody’s guess. Nevermind the fact that predicting how regulators will rule on M&A is always difficult, this particular situation has complex political undertones. But it certainly feels like sentiment has turned more negative recently, and I even wrote that Sprint shareholders need to brace for the possibility that the company ends up alone. I won’t rehash all my points as to why a stand-alone Sprint looks scary (you can read them all here), but I’ll summarize by saying this is a deeply indebted company with negative free cash flow and a bruised brand in need of serious investment.

T-Mobile made a similar “woe is me” argument for its 2011 attempted sale to AT&T, which was rejected by regulators. That, of course, proved to be incorrect given that T-Mobile then staged an incredible turnaround and became the fastest-growing carrier, its subscriber base eventually eclipsing Sprint’s. However, T-Mobile’s parent was awarded a $3 billion breakup fee and rights to airwaves that later helped the business in its transformation. Do you know what Sprint gets if the T-Mobile merger is blocked? Nothing.

Sprint’s financial challenges aren’t reason enough to approve the transaction, though. I’ve also noted that the combined company would command a significant share of the prepaid market that serves lower-income Americans. And members of Congress have questioned the effects on residents of rural areas.

John Legere, T-Mobile’s CEO, has been a cheerleader for this deal like no executive has ever stumped for their company before. His style is to be candid with critics, and that’s given him a certain air of credibility. But his somewhat flimsy commitment in February — which came seemingly out of nowhere — to not raise prices for three years following the merger left much to be desired. It’s hard not to interpret that as an admission the combined company would have the ability and incentive to flex its pricing muscle.

Here’s a simple question for Legere: If the deal won’t lead to higher prices, why then are shares of Verizon and AT&T sinking on speculation that the deal may be doomed?

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.