(Bloomberg Opinion) -- In a fractious call with analysts last month, during which Ford Motor Co.’s management were once again lambasted for their vagueness about planned restructuring measures, Chief Financial Officer Bob Shanks did make at least one revealing comment:

“We swim in the water with ankle weights, big ones … We want to get them off so that the real underlying strength of this company can come through.”

He was referring, of course, to Ford’s unprofitable international operations and a portfolio that’s still too heavily skewed towards unpopular sedan cars — factors that contributed to a shock profit warning.

But with Ford’s shares falling by one quarter so far this year, investors must be wondering whether that’s the extent of the automaker’s surplus baggage.

Two more potential problems — leadership and liquidity (namely, Ford’s capacity to pay dividends) — have also come into sharp focus recently. Neither will be addressed in a hurry, and that’s partly because of the influence of the founding family.

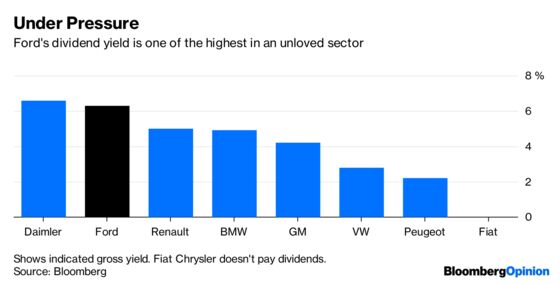

First, liquidity: Ford is committed to paying about $3 billion in dividends this year. In view of Ford’s rapidly deteriorating operating performance and the litany of longer-term challenges it faces, that’s probably too high. The 6.3 percent dividend yield — a level that often indicates a payout cut is in the offing — suggests plenty of investors think the same.

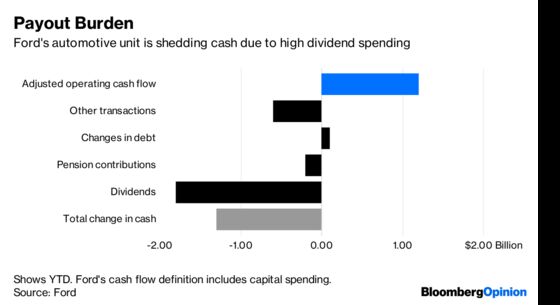

Not so long ago, some analysts were complaining Ford was too stingy with its cash. So what’s changed? Outside the U.S., Ford isn’t generating returns that exceed its cost of capital. Including dividend and pension contributions, Ford’s automotive unit consumed about $1 billion of cash last year and this year isn’t shaping up any better. Management have, somewhat belatedly, announced a mammoth restructuring that’s set to cost about $7 billion in cash terms over the next four years or so. The company’s annual capex bill is about $7.5 billion, plus it is also having to invest plenty in autonomous vehicle research. Suddenly, things look tight.

True, Ford’s balance sheet remains in decent-ish shape now — the autos unit has about $9 billion of net cash. But a more sudden sales slowdown would cause this to bleed cash due to Ford’s negative working capital position. Already, cash flow is deteriorating, and Berenberg analyst Alexander Haissl says the company will have to cut the dividend by one-third from next year.

That’s liquidity. What about leadership?

Chairman Bill Ford made a good call when he hired Alan Mulally from Boeing to run crisis-hit Ford in 2006. Mulally’s experience of cost-cutting at a hugely complex manufacturer proved invaluable at the automaker, which, unlike rival General Motors Co., didn’t require a government bailout.

Hence, Ford watchers were probably reluctant to question the chairman’s decision last year to tap another outsider to run the company — Jim Hackett, whose background is in office furniture. Ford described Hackett, who took up the helm in May 2017, as a “visionary” — in other words, the sort of person needed to help the company make the leap to the autonomous and electric vehicle era.

Hackett certainly isn’t to blame for the shortcomings in Ford’s product line-up or China business, which predate his arrival, and he’s had plenty of bad luck, too: Ford’s very profitable U.S. truck operations were hit by a fire this year, the competitiveness of U.K. business is being upturned by Brexit, plus complying with Europe’s tough new emissions rules is proving challenging.

However, Hackett’s encounters with the financial community — peppered with buzzwords but short on details — have been nothing short of disastrous. Furthermore, the speed at which Carlos Tavares has turned around Peugeot (and now Opel/Vauxhall) has made Hackett’s repeated pleas for patience feel pretty inadequate. A Wall Street Journal article this week exploring Hackett’s cerebral/baffling leadership style hasn’t helped his cause either.

Arguably, what Ford needs right now isn’t so much a visionary but someone who can also take swift, tough decisions — about half of the company’s 200,000 workforce are in Ford’s unprofitable overseas operations, which underscores the scale of the challenge.

His frustration boiling over, Morgan Stanley analyst Adam Jonas outright asked Hackett last month whether he still expected to be running the company when the company finally gets around to holding a now-delayed capital markets day. But having waxed lyrical about Hackett’s qualities so recently, Bill Ford is hardly likely to withdraw his support now.

Similarly, the chairman and his family aren’t likely supporters of a dividend cut — they control 40 percent of the voting rights thanks to a special class of stock, and depend on the lucrative payout. Shanks, the CFO, told Bloomberg on Tuesday the dividend isn’t at risk.

With Ford’s management treading water, its investors are left to hope that the company’s many ankle weights don’t cause it to drown.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.