A Solitary Rate Hike Can’t Save the Lira Now

The Turkish central bank has to be given independent rein to really get hold of inflation by committing to continue hiking rates.

(Bloomberg Opinion) -- If a battle can’t be won, don’t fight it.

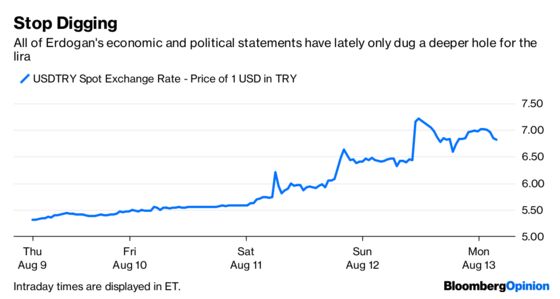

Turkish President Recep Tayyip Erdogan would be well advised to recognize that his campaign for the lira was lost before it even started. His rhetoric in recent days on “economic war” being waged against his country has only fanned the flames.

Though the central bank has at least shown it’s not asleep — its move over the weekend to loosen banks’ reserve requirements is a welcome step — the measures have not had much of an effect. Tinkering with liquidity does not address the main issue.

The central bank has to be given independent rein to really get hold of inflation by committing to continue hiking rates. This is going to require a huge swallowing of pride from Erdogan — he may have won the recent presidential election, but as my colleague Mark Gilbert pointed out, investors get to vote every day. And the president is refusing to accept reality.

Bar a Damascene conversion from this strongman, the only thing that will make a difference to the currency is an interest-rate increase. The magnitude would have to be substantial — at least 200 to 300 basis points. But that still wouldn’t be enough. For a start, it would have to happen well ahead of the next central bank meeting, which is scheduled for Sept. 13.

Equally important is the conviction with which policy makers deliver the move. Officials need to demonstrate a total change of attitude, and clearly signal that this won’t be a case of “one and done.” Investors need to see that a series of increases are on their way, and that they will continue until inflation is controlled. This is the only way the doom loop can be broken.

This will not solve all of Turkey’s problems, as they didn’t spring up overnight. Inflation has been out of control for a while, and the current account has been in deficit for years. Though investors had viewed the fragility of Turkey’s position as an acceptable risk, Erdogan’s obstinate refusal to accept basic economic fundamentals has given them every reason to turn away, as I have argued.

He can’t close down the borders and hide. He’s in charge of an open economy that is heavily reliant on dollar funding, which means that not only are the tools of economic warfare out of his hands, one potential weapon — capital controls — has the potential to seriously worsen the situation.

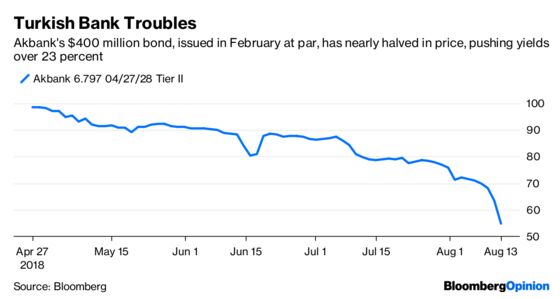

This also means that the Turkish banking system is incredibly vulnerable. The lira’s freefall has provoked a surge in nonperforming loans, according to Bloomberg Intelligence. Forty percent of the nation’s corporate lending is in foreign currencies, a proportion that only grows as the currency declines.

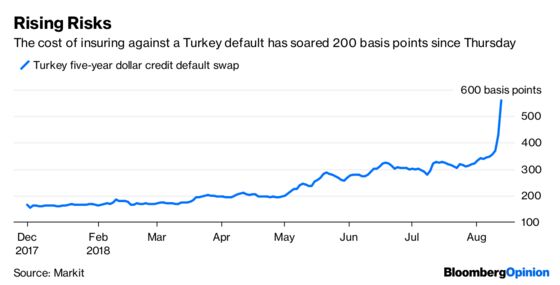

That subsidy seems like it’s weathered the recent storm up to now. The problem is that it also looks increasingly fragile, because there’s a huge risk that creditors’ sentiment turns. Turkish banks so far don’t seem to have had to pay a bigger margin to access foreign-currency loans, though that hasn’t kept their senior five-year credit default swap spreads from ballooning above 500 basis points, according to Markit data.

A really worrying sign would be if foreign banks started to pull back substantially from lending syndicates. Turkish banks have about $20 billion of dollar and euro-denominated bank debt to roll over until the end of 2019. Clear evidence of a withdrawal here would the beginning of the end for lenders and companies.

However many “new friends” Erdogan says he can drum up to replace Western financing, the fact of the matter is that they don’t seem to have the firepower — not to mention the willingness — to roll over what Turkish borrowers already owe.

The troubles for his banks don’t have to end there. President Donald Trump seems like he’s just getting warmed up. He has the power to restrict dollar funding through sanctions, and were that to happen, Turkey would be utterly impoverished overnight.

He isn’t there yet. Turkey’s strategic position for NATO should, hopefully, allow sanity to prevail in Washington and in Ankara.

But Trump has all the cards, and Erdogan should quit this pointless battle while he’s behind.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.