A Great Vehicle Lurks in Hyundai’s Corporate Chop Shop

Elliott Management Co may cancel a central part of a restructuring plan for the merger between Hyundai Glovis and Hyundai Mobis.

(Bloomberg Opinion) -- Is the tide turning in the favor of activist shareholder Elliott Management Corp. in its drive to clean up the web of more than two dozen auto-related companies at the core of the Hyundai chaebol?

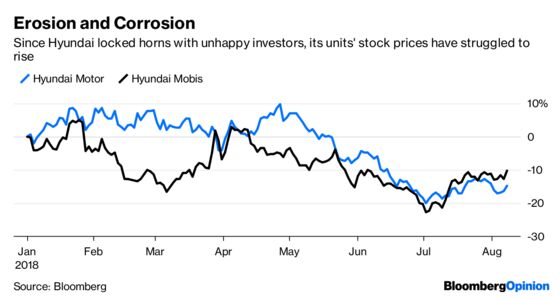

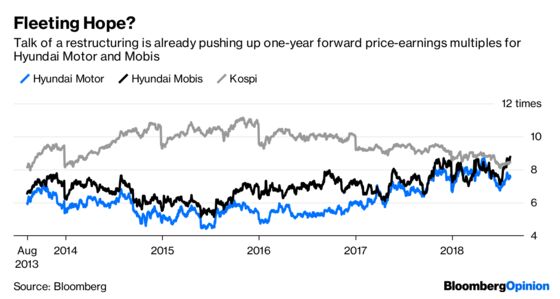

On Wednesday, South Korean media reported that the group may cancel a central part of a restructuring plan that’s been opposed by Elliott, in the form of the planned merger between its logistics business Hyundai Glovis Co. and the after-sales division of parts supplier Hyundai Mobis Co. The company batted down the reports but shares in Mobis and the core company Hyundai Motor Co. rose, as investors became hopeful that one of the key bones of contention for Elliott could be laid to rest.

The argument by Elliott and proxy advisers such as Glass Lewis & Co and Institutional Shareholder Services Inc. is that the morass of listed companies and circular shareholdings that make up Hyundai’s empire has weighed on valuations across the group. Shareholders are put off by the structure, which gives the founding Chung family a level of control out of proportion to their economic interest, and allows some Hyundai entities to benefit from related-party transactions.

The Mobis-Glovis merger that Hyundai had proposed as a step toward resolving these issues would do nothing of the sort, in Elliott’s view. Instead, the group should create a more efficient holding company structure, cancel shares and boost shareholder returns. As we wrote here, Hyundai’s plan was fraught with illogical numbers – but if the group abandons this central plank, what options does it have to keep shareholders happy while attempting to tidy up?

Given the tangle that is Hyundai’s ownership structure, no solution will be easy or painless. But there are ways to keep the restructuring simple rather than drag investors along and erode more value.

A good starting point is the best-known business, Hyundai Motor, which sits at the center of four loops of circular shareholdings. As analysts at Goldman Sachs Group Inc. noted at the time of Hyundai’s initial restructuring announcement, the car unit “has the least efficient capital structure and greater potential for value-unlocking compared to Hyundai Mobis or Hyundai Glovis.”

A restructuring could begin by the Chung family selling down their stakes in affiliates and transferring their shares into Hyundai Motor, where the family’s relatively low ownership levels means it isn’t currently incentivized to dole out dividends or clean up the capital structure. Putting ownership control in the same place as the bulk of the assets should boost payouts, as should the fact that Hyundai Motor carries the most cash among group companies.

Then there’s Hyundai Mobis, the valuable parts business that generates cash and strategically fits with Hyundai Motor. Spinning off the Mobis after-sales business and merging it with Hyundai Motor instead of Glovis would make a great deal of sense. Mobis could be the ultimate “value creator,” according to Smartkarma analyst Sanghyun Park.

A major problem with any plan would be tax. The basis of Hyundai’s previous proposals has been an attempt to minimize tax payments, which would inevitably flow from restructuring transfers. Still, while there’d be an initial hit from capital gains, in the longer term a holding company would get tax relief on dividend income from its affiliates. (Hyundai also argues a holding company would forbid it from owning financial subsidiaries, but Elliott has a simple solution to that: Sell the financial subsidiaries.)

The trouble for Elliott is that it doesn’t want to have to wait around so long. But for longer-term investors, aligning the interests of various stakeholders so that incentives ultimate drive a higher valuation should be a more important goal than just maximizing returns straight off the bat.

As the likes of Toyota Motor Corp. have shown, slimming down and reducing inefficiencies is the one way to keep shareholders happy in the struggling global car market. Shares of Hyundai Motor and Mobis are down between 12 percent and 23 percent since their April peaks, eroding already depressed valuations. If the family that control Hyundai do in fact want to please all their shareholders, they should be ready to bite that bullet.

To contact the editor responsible for this story: David Fickling at dfickling@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.