Is KKR Building What Europe’s Phone Giants Never Could?

(Bloomberg Opinion) -- As our appetite for data booms, private equity firms are betting on the cell towers and cable infrastructure to support it. The prize looks to be in creating the pan-European giant that has so far eluded the region's telecoms industry.

For years, Europe's carriers have struggled to consolidate across the continent in the same way as their U.S. counterparts. But KKR & Co. is making strides in the tower business, where companies lease space to mobile carriers to install the antennae that power their networks.

Last month, the U.S. leveraged-buyout firm snapped up just less than 50 percent of Altice NV's French towers arm, SFR TowerCo. KKR already owns a 40 percent stake in Telxius Telecom SA, an operator in Germany and Spain that was spun out of Telefonica SA last year.

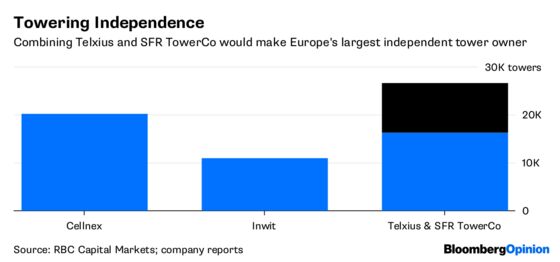

Would it make sense for KKR to engineer a merger of the two companies? It's instructive to compare the valuations of peers Inwit SpA and Cellnex Telecom SA, according to RBC Capital Markets analyst Jonathan Dann.

Inwit (still 60 percent owned by Telecom Italia SpA) and Cellnex both have an enterprise value of about 20 times trailing 12-month Ebitda, despite the fact the latter gets 30 percent of its revenue from the much less profitable business of operating television masts.

The key difference is that Cellnex owns towers in Spain, Italy, France, the Netherlands, U.K. and Switzerland, while Inwit only operates in its domestic Italian market. Investors appear to be much more willing to reward geographic spread with a more generous valuation.

KKR could follow that template -- and reap a profit. Its deal to acquire the stake in the Altice unit gave the operation an enterprise value of 18 times 2017 Ebitda. In the Telxius purchase, the comparable figure was 11.4 times, lower because of the operator's less profitable submarine cable business.

Putting the Telxius and Altice towers together would create a business with scale across Europe that would be more attractive to investors together than separately.

Even if that doesn't happen, the industrial logic of KKR's investment looks sound. Towers owned by carriers typically find it harder to generate business from rival operators. In Europe, independently owned towers serve an average of 1.7 carriers, compared with 1.1 for captives, according to advisory firm Delta Partners Group. That means there's a lot of expansion potential for KKR.

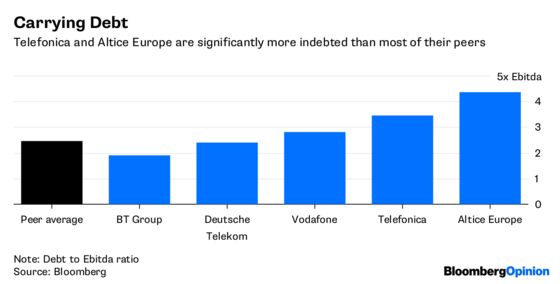

Given their remaining majority shareholders, the carriers will still need to be convinced. But Telefonica and Altice have significantly higher leverage than most of their peers. That makes it harder to invest in acquiring the new tower sites that 5G phone networks will require, a task more easily achieved by a separate firm. The prospect of a stake in a more valuable multinational business might also be more appealing for them.

With tower businesses in other countries likely to come up for grabs, don’t be surprised to see private equity firms bidding for more pieces of a prospective pan-European towers behemoth.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.