Plug Power and Lordstown Show Trust Is a Precarious Thing

(Bloomberg Opinion) -- Overhauling the world’s industry, power systems and transport to halt the climate crisis will require hundreds of billions of dollars of new investment. Happily, the equity markets have been in a mood to write large checks.

High valuations are helping clean-tech companies attract vast amounts of capital to fund their ambitions. Special purpose acquisition companies, which raise money from investors and then find a company to merge with and take public, have further greased the money machine.

Trust is a fragile thing, though.

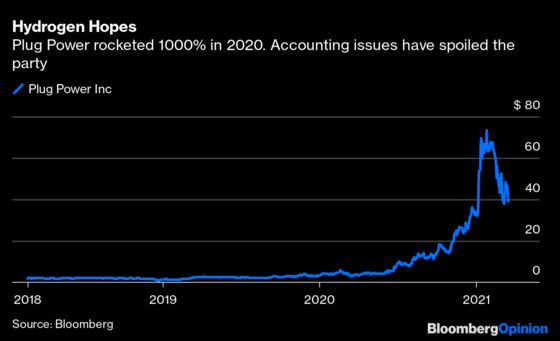

Several clean-tech companies are facing accounting and regulatory bother. They’re also in the crosshairs of short sellers. Hydrogen fuel cell maker Plug Power Inc. told investors this week that its financial statements spanning the last three years should no longer be relied upon, because of accounting errors.

The restatements won’t affect Plug Power’s cash position or revenue goals, but they became necessary after audit firm KPMG LLP changed its view on the proper accounting treatment for various items including leases and loss accruals. The company emphasized there had been no misconduct. It’s not the first time, however, that it has drawn the wrong sort of attention. In January a short seller, Kerrisdale Capital, highlighted Plug Power’s poorly conceived customer agreements.

Plug Power isn’t an isolated example of trouble. Lordstown Motors Corp., an electric-vehicle manufacturer, said this week that the U.S. Securities and Exchange Commission was looking into claims by short seller Hindenburg Research that it paid consultants to generate pre-orders for its forthcoming pickup truck.

And last month Nikola Corp., a maker of electric- and hydrogen-powered trucks said several statements made by former Chairman Trevor Milton about its technological capabilities were “inaccurate in whole, or in part.” The SEC’s investigation of Nikola on matters also raised by Hindenburg continues. Milton has left the company and General Motors Co. has scaled back a proposed partnership.

I expect we’ll see more of this kind of thing. Hoping to discover the next Tesla Inc. while it’s still a minnow, investors prefer throwing money at small companies promising the moon rather than experienced heavyweights. The upside’s greater, but so are the dangers.

Twelve months ago Plug Power’s accounting issues wouldn’t have warranted much attention. It hadn’t made a profit in its more than two-decade history, generated a few hundred million dollars of annual sales and had a market cap of barely $1 billion. However, in January the market value had swelled to $34 billion amid excitement that governments are finally committing to net-zero emissions targets and that hydrogen will be crucial in decarbonizing heavy industry and transport.

Clean-tech stocks have deflated somewhat subsequently as bond yields have risen but Plug Power remains the largest company by value in the Russell 2000 index of U.S. small caps and it’s a favorite among retail investors. About $4.5 billion of its shares changed hands on Wednesday. The high valuation reflects the profits investors believe it will earn in future, not the losses it made in the past. But it’s still important that shareholders can rely on a company’s financial statements.

The business has taken financial advantage of its recent popularity, raising about $4.5 billion since November by selling stock — including a $1.6 billion investment by South Korea’s SK Group. Investors in February’s $2 billion capital increase are sitting on 40% paper losses now. They won’t be pleased.

Though unrelated to the accounting restatements, Plug Power is also contending with problematic contracts. In 2017 Walmart Inc. and Amazon.com Inc. were promised tens of millions of share warrants in return for ordering hydrogen fuel cells for their warehouse forklifts from the company. Plug Power’s surging share price means those agreements have become a burden. Non-cash charges connected to the warrants caused it to post a negative $100 million of revenue last year. You don’t see that very often in business.

These customers “are literally getting paid to take the product,” an incredulous analyst said on the company’s February investor call.

The need to generate customer orders is at the root of Lordstown’s difficulties. During an investor call on Wednesday, its management said a special committee had been formed to review Hindenburg’s accusations that many of the 100,000 vehicle preorders boasted about by the company aren’t serious. Lordstown said it would cooperate with the SEC’s request for information.

Last week Chief Executive Officer Steve Burns said the firm had “always been really clear” that preorders are nonbinding. Lordstown became a public company last year after merging with DiamondPeak Holdings Corp., a SPAC. The transaction generated $675 million in gross proceeds with the aim of starting production in September.

It’s great that small companies are able to raise large gobs of equity capital to fund the infrastructure and equipment we need to decarbonize the economy. But it’s vital, too, that investors can trust the information with which they’re presented. Missteps could harm investor confidence, raise the cost of capital and hold back the clean-tech revolution at a crucial moment.

On a fully diluted basis the implied value was even higher

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2021 Bloomberg L.P.