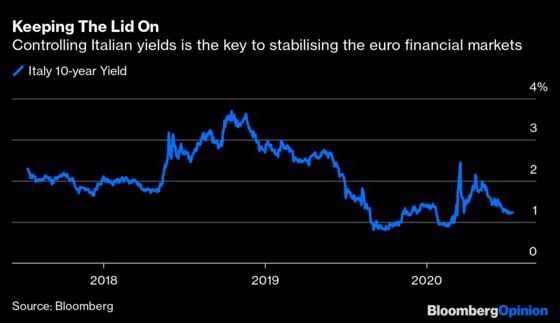

(Bloomberg Opinion) -- Do central bankers learn from their mistakes? After sounding inflexible in March, Christine Lagarde fortunately changed tack and unambiguously demonstrated her resolve to defend the euro area from the impact of the pandemic.

The challenge now facing the president of the European Central Bank is to show the institution is still fighting the crisis when the need for big initiatives has been satisfied. Fine-tuning the existing support measures could nevertheless go a long way when the ECB governing council meets today.

The temptation must be to sit tight and shift the conversation to the politicians, calling on them to provide a matching fiscal response at this weekend's summit of EU leaders. That would risk the impression of complacency in this last ECB monetary policy meeting until September, ahead of a summer of likely continuing market volatility.

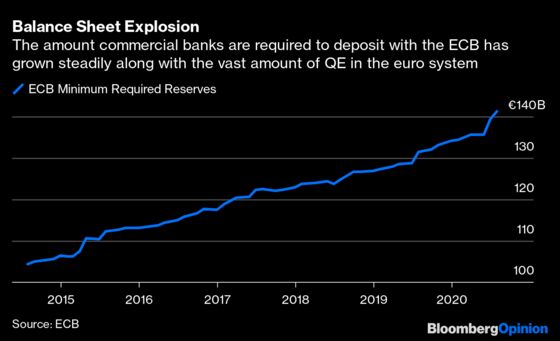

Now is the time to sweat the small stuff and address some of the side effects of the existing package. One logical next step, which the ECB has hinted at, would be to mitigate further the impact of negative rates on the European banking sector by cutting the cost of parking funds with the central bank. A more profitable banking sector will have more confidence to increase lending. The ECB’s July euro-area lending survey cautioned that banks expected to tighten lending criteria as state guarantees expire in some countries.

The fix would involve tweaking the so-called deposit-tiering system. In short, this would permit banks to hold more of their excess reserve funds at the zero main financing rate, instead of the negative 50 basis points official deposit rate. The ECB currently allows six times each bank’s minimum reserve requirement but raising this multiplier to eight times could collectively save euro-zone banks 1.4 billion euros ($1.6 billion) annually.

The boost from changing the multiplier may be modest compared to overall banking sector earnings, as analysts at ABN Amro Bank NV point out. But a little bit now would help sustain the momentum of central bank policy.

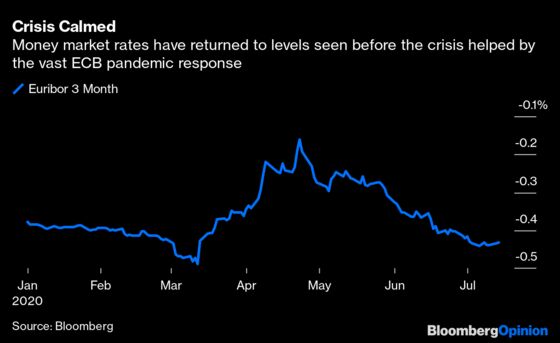

The snag is that this may inflate borrowing costs between the banks themselves. In fact, any impact on the overall liquidity of the system is likely to be minimal given the ECB’s existing stimulus measures, as ABN’s analysts note. The seizure of the money markets at the start of the Covid-19 crisis is past, as evidenced by the three-month Euribor rate’s gradual decline.

Steadily improving the overall stimulus package would also have a strong signaling effect — demonstrating that the ECB still has ammunition and is constantly prepared to support the economic recovery. There have been signs that the second-quarter contraction was not as deep as the central bank initially feared, and the third-quarter rebound may be even stronger. But with the risks of a second virus wave, now is not the time to sit back and hope enough has been done.

The key is to ram home a “don’t fight the ECB” message to the markets. Lagarde is not going to repeat her early mistakes.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.