The Bond Market Goes Through the $14.5 Trillion Looking Glass

(Bloomberg Opinion) -- With negative yields becoming commonplace across even the longer maturities in many of the world’s government bond markets, fixed-income managers are letting their imaginations run a little wilder about what might come next. So brace yourself for renewed talk of helicopter money, the implementation of Modern Monetary Theory, and the prospect of the benchmark U.S. Treasury offering less than zero.

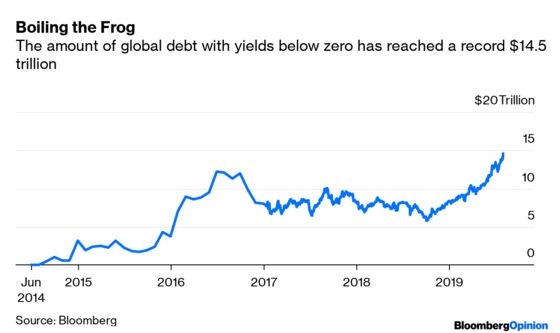

Bond investors have spent the past few years becoming accustomed to previously inconceivable developments in the markets. So they can be excused for developing an immunity to just how extreme recent shifts in the debt market have been, at the forefront of which is the explosion in the amount of negative-yielding debt.

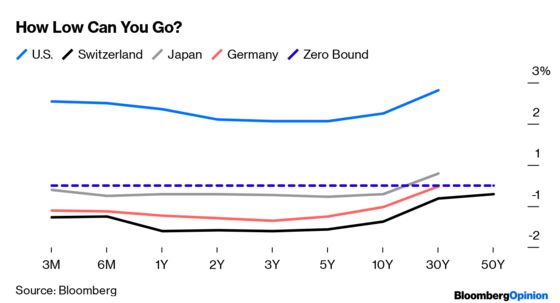

As the chart above shows, the total value of “less than zero” bonds has trebled since October as interest rates on fixed-income securities get lower and lower. The entire suite of German government bonds from three months to 30 years now offers negative yields for the first time, as does the even longer-dated Swiss yield curve. Monday saw Ireland’s 10-year borrowing costs dip below zero for the first time.

With central banks poised to continue or resume the bond-buying programs they introduced after the global financial crisis, other government debt markets look set to follow suit in breaching the zero bound. Spain’s benchmark bond yields a smidgen above 0.2%, Portugal’s is a tad below 0.3%. U.K. 10-year yields are at a record low of about 0.5%, half their level of less than three months ago.

And while U.S. yields remain at about 1.8%, Joachim Fels, Pimco’s global economic adviser, says it’s “no longer absurd” to speculate that the world’s benchmark rate for 10-year borrowing costs could drop below zero. “We may get there faster than you think,” he says.

The problem with pushing down borrowing costs that are already at or near record lows is that you get diminishing returns on how much of an impact it has on the real economy – hence the failure of central banks to lift inflation and meet their targets in recent years.

So Eric Lonergan, a fund manager at M&G Prudential, reckons the concept of helicopter money, with central banks creating cash and delivering it to individual citizens to spend, might come back into vogue. “The logic is compelling,” Lonergan wrote in an article for the Financial Times last week. “One problem with this common sense idea is its simplicity, which rarely appeals to economists charged with taking important decisions.”

As central bankers run out of ammunition from their conventional armories, a more radical shift may become inevitable, with governments acknowledging that they must play more of a role in combating a global slowdown – and a new-fangled economic experiment called Modern Monetary Theory becoming the next experiment in how to boost growth.

MMT, which argues that an expansionary fiscal policy can be financed through cheap debt without risking default, has been criticized for not being modern, not being monetary and not being a theory. That didn’t stop the first textbook on the subject from selling out its initial print run earlier this year, nor the adoption of MMT as a cause celebre by Alexandria Ocasio-Cortez and other left-wingers in the U.S. Democratic party.

There’s likely to be a “pro-growth convergence of fiscal and monetary policies,” Pascal Blanque, the chief investment officer of Amundi SA, told me recently. Blanque previously expected only a recession to usher in MMT. Now he sees “an alignment of the planets between the man in the street, politicians, academics, politicians” that may well see it becoming mainstream thinking.

In “Through the Looking-Glass,” Lewis Carroll’s Alice says there’s no use trying to believe in impossible things. “I daresay you haven’t had much practice,” the Queen replies. “Why, sometimes I’ve believed as many as six impossible things before breakfast.” Bond investors are starting to understand her thinking.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.