A $1.6 Trillion Fund Warns of a Ticking Liquidity Bomb

(Bloomberg Opinion) -- Bank of England Governor Mark Carney says investment funds that promise to allow customers to withdraw their money on a daily basis are “built on a lie.” The chief investment officer of Europe’s biggest independent asset manager agrees with him.

“There is no point denying we are faced with a looming liquidity mismatch problem,” says Pascal Blanque, who oversees more than 1.4 trillion euros ($1.6 trillion) as the CIO of Amundi SA.

As I wrote earlier this month, market liquidity can melt away faster than a dropped ice-cream in a heatwave. That prospect is one of “various things keeping me awake at night,” Blanque told me earlier this week.

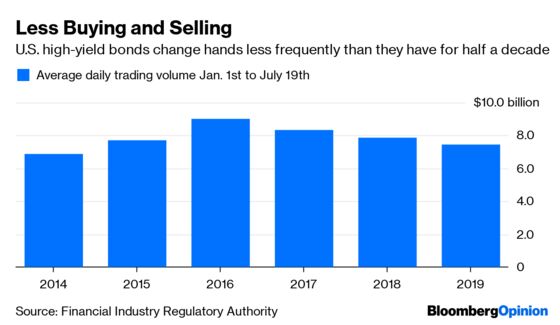

In the wake of the global financial crisis, regulators have obliged investment banks to bolster their balance sheets. That has reduced the amount of capital those institutions are willing to commit to the securities markets. So in many areas, liquidity is already drying up. For example, daily turnover in U.S. high-yield debt is at its lowest since 2014, as noted by my Bloomberg Television colleague Lisa Abramowicz:

Market making, where firms generate prices at which they are willing to either buy or sell financial products, is effectively “a public good,” Blanque says. As that activity declines, the drop in turnover reduces the banking industry’s exposure to a collapse in prices or a surge in volatility. But the dangers are simply transferred, rather than diminished.

“Market making is falling off a cliff at the level of individual banks, but creating a systemic problem,” Blanque says. “The banks are less risky – but the risks have been shifted to the buy side.”

That poses a problem for regulators, something the Bank of England acknowledged in a working paper published earlier this month. As the funds industry has supplanted banks as a source of credit in the past decade, households and companies have benefited from a useful alternative source of financing. But, the report warned, we don’t know how this market-based system will respond under stress.

Modelling such a scenario “can generate an adverse feedback loop in which lower asset prices cause solvency/liquidity constraints to bind, pushing asset prices lower still,” the BOE found. In other words, the new market structure may be worse than the old.

The difficulty for asset managers in such an eventuality is finding sufficient cash to repay exiting investors while preserving the structure of the portfolio without distorting market prices, according to Blanque. “We don’t know the channels of transmission, we don’t know how the actors will act,” he says. “It is uncharted territory.”

Part of Amundi’s response to the issue is to include liquidity buffers in its portfolios, which may mean holding securities such as German bunds and U.S. Treasuries, which should always trade freely. But the industry needs to come up with a common definition so that liquidity is included along with risk and return when assessing a portfolio’s robustness, Blanque says.

For now, asset managers have to cope with what Blanque called “the sacred cow” of allowing clients to withdraw funds on a daily basis. “It is a bomb, given the risks of liquidity mismatch,” he warns. “We don't know if what is sellable today will be sellable in six months’ time.”

Regulators are slowly coming to realize that the fund management industry has increased exponentially in both size and systemic importance in the past decade. I’ve argued before that asset managers should be stress tested in the same way as banks are forced to assess their ability to withstand market shocks. The recent distress experienced by customers of Tim Haywood, Neil Woodford and Bruno Crastes suggests that need is becoming more urgent.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.