RBI’s Policymakers Spar Over High Inflation, Steep Yield Curve

A debate is raging among India’s monetary panel members on the credibility of the central bank’s inflation forecasts.

(Bloomberg) -- A debate is raging among India’s monetary panel members on the credibility of the central bank’s inflation forecasts, raising questions over its price-growth targeting regime.

The argument between Michael Patra, the deputy governor for monetary policy, and J.R. Varma, a new member of the rate-setting panel, centers around whether the nation’s steep yield curve reveals a lack of market confidence in the Reserve Bank of India’s inflation estimates or is a reflection of excessive focus on old data.

For months now, inflation has exceeded the RBI’s tolerance band and held it back from cutting rates. Instead, it introduced liquidity measures and bought bonds in an attempt to bring down borrowing costs, with Governor Shaktikanta Das directly appealing to traders to help it control the steepening yield curve.

The latest data on Thursday show no respite for the central bank, with retail prices surging 7.61% in October, against the 7.31% estimated by economists. Inflation has remained above RBI’s 6% upper limit for seven successive months, though it has kept arguing that the pressure will ease.

Varma, a professor of finance at the Indian Institute of Management, isn’t convinced.

Sole Dissenter

He was the sole dissenter last month, when the RBI kept rates unchanged and said accommodative policies would extend into the next fiscal year. Varma contended that the stance on lower-for-longer rates should not be a decisive one.

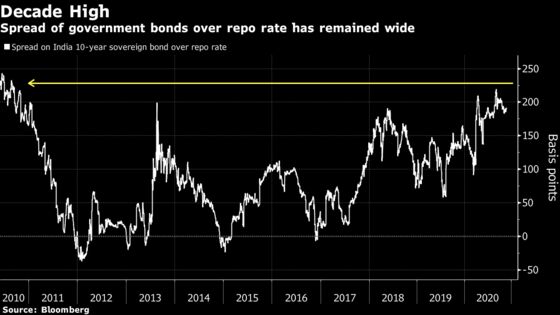

One of the hallmarks of a credible inflation-targeting regime is a substantial compression of the inflation risk premium, and the steep curve indicates doubts about RBI’s guidance, Varma was quoted as saying in the meeting minutes.

At the heart of the dispute is an interpretation of why the term premium -- the difference between short and long-term yields -- have stayed elevated. From July 2019 to August 2020, the gap between the policy rate and the 10-year bond yield increased 150 basis points to 215 basis points.

It’s now at 189 basis points, with the repurchase rate at 4% and the 10-year yield at 5.89%.

Liquidity, Not Inflation

For Patra, who co-wrote a paper with Harendra Behera and Joice John in the central bank’s November bulletin, the term premium is most closely associated with liquidity conditions.

Analysis shows that the bond market is backward-looking in its inflation view and adapts to prints that are one-month old, he said. Empirical analysis between January 2006 to September 2020 suggests that global uncertainty and liquidity are the main drivers of the term premium in India, he said.

“With interest rates at or the near-zero lower bound in several advanced economies, whether real or nominal, monetary policy that seeks to compress the term premium and influence the long-term interest rates more directly takes a step into the unknown,” Patra and his co-authors wrote.

A RBI spokesperson and Varma didn’t respond to emailed requests for comment.

©2020 Bloomberg L.P.