RBI Seen Using Hybrid Playbook to Keep Bond Traders Guessing

India’s central bank may adopt its own version of yield-curve control as it digs deeper into its toolbox to cushion the economy

(Bloomberg) -- India’s central bank may adopt its own version of yield-curve control as it digs deeper into its toolbox to cushion the economy during the coronavirus pandemic, according to a unit of the country’s second-largest private lender.

The Reserve Bank of India may buy debt at irregular intervals to tame spikes in yields as it seeks to accelerate transmission of cuts in policy rates, breaking from the hard yield-control policies followed by the Bank of Japan and Reserve Bank of Australia, A Prasanna and Abhishek Upadhyay, Mumbai-based analysts at ICICI Securities Primary Dealership Ltd., wrote in a report to clients.

The authority may implement “soft yield-curve control” involving “strong, sporadic interventions around specific thresholds, which may not be in keeping with any specific script,” he said. “The RBI would cap any sell-off in bonds but at the same time abstain from specifying any defined range or level.”

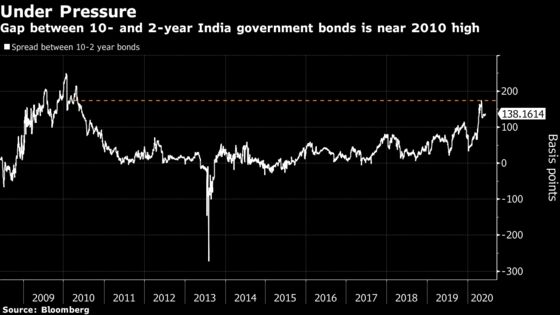

Whether with the use of a Federal Reserve-style ‘Operation Twist’, the European Central Bank-like cash boost to banks and open-market debt purchases, the RBI has shown to be decisive in its quest to keep rates low. Still, the gap between the most-traded 2029 notes and two-year debt is near the widest in a decade, hindering the pass through of rate cuts.

The RBI may buy 3 trillion rupees to 6 trillion rupees ($79 billion) of bonds this fiscal year to implement its plan, Prasanna wrote. The authority has bought about 1.2 trillion rupees of debt since April 1, which has helped pull down yields on the 6.45% 2029 notes by more than 50 basis points since end-January.

The yield on 2029 bond was little changed at 5.98%, while that on the new benchmark 10-year note was also steady at 5.80% at 10:09 a.m. in Mumbai.

“The RBI should keep an intervention threshold very close to current market levels,” said Prasanna. “Actions reinforcing this premise would incentivize market participants to veer around to RBI’s thinking.”

Yield-curve control, a policy that involves purchasing, or selling, government bonds in order to target the yield on a specific maturity, has been used by Japan for years to boost economic activity and was recently adopted in Australia. Some economists expect the U.S. to adopt the tool in coming months as policy makers seek to provide more support for businesses and households.

©2020 Bloomberg L.P.