RBI Owns More of Its Benchmark Bond Than Yield-Managing BOJ

Reserve Bank of India now holds more than half of the country’s closely watched 10-year bond, keeping the yield remarkably steady.

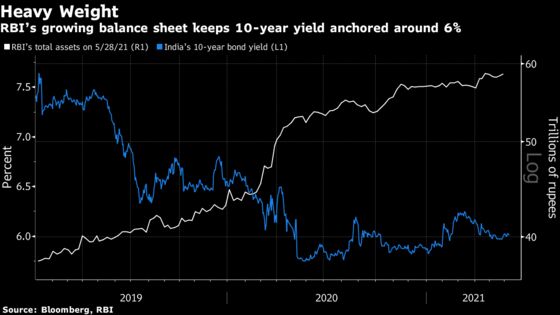

(Bloomberg) -- The benchmark yield in India’s one-trillion-dollar sovereign bond market is holding remarkably steady despite a ballooning government borrowing program. A possible reason for the lull is that the central bank now holds more than half of the closely watched 10-year bond.

The Reserve Bank of India has lifted its holding of the 5.85% 2030 bond to 545 billion rupees ($7.5 billion) or at least 52% of the total outstanding via Operation Twists, two tranches of government securities acquisition program and indirectly via a special auction in February, Bloomberg calculations show. The number is likely even higher if the RBI’s discreet secondary-market purchases are incorporated.

That dwarfs the Bank of Japan’s 21% holding of its March 2031 bond. The comparison is stark because the Japanese central bank has a specific commitment to control the yield of its benchmark.

The RBI has repeatedly denied it wants to keep the 10-year yield anchored around 6%, even though the market sees that as a line in the sand for the central bank. A central bank spokesman wasn’t immediately available for comment.

To be sure, the BOJ hasn’t needed to scoop up as much of the latest issue to maintain its yield target under current market conditions. The BOJ still holds 48.4% of Japan’s government bonds while the RBI owns 15.7% of Indian sovereign debt as of December.

The RBI purchases have helped India’s 10-year yield to stay boxed in a range of 6.04%-5.96% since last month even after the government said in late May that it plans to borrow an additional 1.58 trillion rupees on top of its plans to raise 12 trillion rupees in the current fiscal year. However, the RBI’s overwhelming influence in the most liquid part of the sovereign yield curve is raising concern that investors may be crowded out.

“The RBI’s purchase of the 10-year bond helps to keep the segment of the yield curve in check, but not the entire curve,” said Arvind Chari, chief investment officer at Quantum Advisors Pvt. “It impacts the floating stock available and makes shorting the bond difficult.”

Some also see it complicating the central bank’s efforts to bring in more foreign investment into the nation’s debt. Indian bonds are the only ones so far in Asia to face foreign outflows on a year-to-date basis even as its 10-year yields are the second-highest yield in the region after Indonesia among investment-grade sovereigns. India’s 10-year yield rose one basis point to 6.02% on Wednesday.

While the RBI’s holding of the current 10-year bond hasn’t had a big impact on liquidity so far, offshore investors wanting to invest would need a clear signal that it would be liquid in the future, according to Rajeev Pawar, head of treasury at Ujjivan Small Finance Bank. Otherwise they will slowly lose interest, he said.

©2021 Bloomberg L.P.