Here’s Why Oil's Outlook Could Be Even Bleaker Than Expected

As storm clouds gather over the world’s top oil-consuming region, OPEC and its allies would be advised to pay close attention.

(Bloomberg) -- As storm clouds gather over the world’s top oil-consuming region, OPEC and its allies would be advised to pay close attention as they prepare to make a key decision on output curbs early next month.

While the Saudi Arabian-led efforts to restrain supply amid surging North American shale production have hogged headlines, a sense of malaise is quietly creeping across Asia. With the U.S.-China trade war now almost a year old and showing no signs of ending, its impact is manifesting itself in everything from profit warnings by Japanese car makers to sagging Chinese diesel consumption.

From Ulsan in South Korea to Mailiao in Taiwan, the region’s big oil processors are cutting run rates as weak demand for fuel products erode their margins. To make matters worse, a wave of Asian mega-refineries is coming on stream this year, flooding the market with cheap fuel and setting off a price war.

It’s a bleak reality that could confound the Organization of Petroleum Exporting Countries and its partners as they try to figure out how best to balance the market. Geopolitical tension and supply-side disruptions are supporting oil prices for now, but a failure by the group to properly gauge demand for their crude in the biggest markets risks undermining their efforts.

“It feels like demand is very, very weak,” said Michal Meidan, head China analyst at Energy Aspects Ltd. “On the supply side, the consensus really was OPEC rolling over the supply cuts,” so it’s quite surprising that prices haven’t risen further, especially with all the geopolitical stress, she said.

Chinese fuel demand appears weak since the start of the year, the International Energy Agency said in its June report, and Japanese and South Korean oil consumption dropped more-than-expected in March and April, respectively. Indian oil demand growth fell to 25,000 barrels a day in April from a year earlier from 225,000 a day in the first quarter, the IEA said.

Double-digit drops in Chinese diesel demand in March and April have been partially due to a sharp slowdown in industrial output.

As refiners in South Korea and Taiwan struggle to break even, new plants that were commissioned in better times are starting up. Hengli Petrochemical Co.’s. 400,000 barrel a day refinery in Dalian is already at full capacity. Rongsheng Petrochemical Co.’s similar-sized plant in Zhoushan, has begun partial operations, while Hengyi Petrochemical Co. is set to start a smaller refinery in Brunei in the third quarter.

In an attempt to grab market share, Hengli offered gasoline in mid-June at about 5,300 yuan ($770) a ton after taxes, said Maggie Han, an oil analyst at consulting firm JLC in Beijing who is tracking offers from the plant. That’s more than 10% lower than other independent oil refiners in the region, she said.

“The start-up of Rongsheng’s refinery in Zhoushan, near major oil-consuming cities such as Shanghai and Hangzhou, will intensify a price war among coastal refineries hoping to market fuel into urban areas,” said Li Li, an analyst at commodities researcher ICIS-China. This will further squeeze the independent refineries and potentially lead to industry consolidation, she said.

The IEA cut its 2019 forecast for worldwide oil demand growth for a second straight month in June, to 1.2 million barrels a day, citing the slowdown in global trade. Wall Street is more pessimistic, with Morgan Stanley seeing an expansion of 1 million barrels a day and JPMorgan Chase & Co. projecting 800,000 barrels. While the IEA predicts growth will improve to 1.4 million barrels a day next year, it also sees supply jumping by 2.3 million barrels.

Not everyone is bearish though. Goldman Sachs Group Inc. said in a June 17 note that infrastructure spending and interest-rate cuts in response to the trade war were setting the stage for a rally in investment and manufacturing next quarter that would boost commodity prices. Citigroup Inc. is more bullish, and forecasts Brent crude may rise to $75 a barrel -- from around $64 now -- over the northern hemisphere summer.

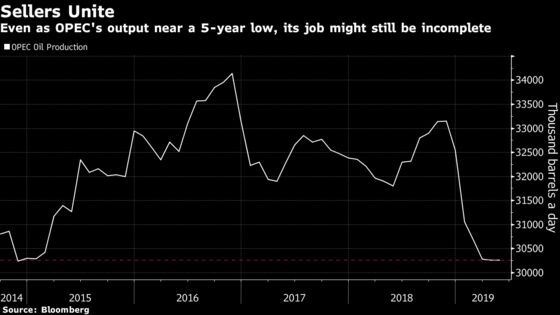

Against this backdrop, the OPEC+ coalition will meet in Vienna on July 1-2 to decide production levels for the rest of the year. The consensus is the current output curbs will be extended, but with OPEC’s total crude production already at the lowest level since 2014, the question is whether that will be enough.

The ratcheting up of tensions between the U.S. and Iran has added another dimension to the situation, complicating OPEC+’s rebalancing task. The risk is the group focuses too much on the Persian Gulf and not enough on the negative demand signals coming from Asia and elsewhere.

Russian Energy Minister Alexander Novak said Monday that the country was taking a wait-and-see approach on the OPEC+ output agreement, suggesting an extension might not be a fait accompli.

“The political risks are obviously mainly to the upside,” but the fundamental economics for oil are quite bearish, Erik Norland, a senior economist at CME Group, which owns derivatives and futures exchanges, said in a Bloomberg TV interview Monday. “You still have soaring supplies in the U.S., and you have demand that’s not really keeping pace.”

--With assistance from David Ingles, Yvonne Man and Tom Mackenzie.

To contact Bloomberg News staff for this story: Alfred Cang in Singapore at acang@bloomberg.net;Sarah Chen in Beijing at schen514@bloomberg.net

To contact the editors responsible for this story: Serene Cheong at scheong20@bloomberg.net, Andrew Janes

©2019 Bloomberg L.P.

With assistance from Bloomberg