India’s Own Version of Yield Control Already Seen in Play

Some investors say the Reserve Bank of India may have already adopted its own version of yield-management policy.

(Bloomberg) -- Even as central banks warm up to the idea of adding yield curve control to their armory, some investors say the Reserve Bank of India may have already adopted its own version of yield-management policy.

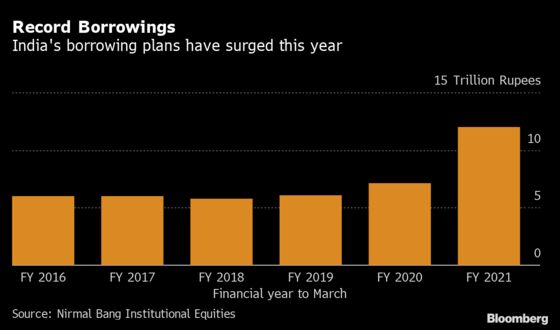

Governor Shaktikanta Das has been coy about outlining how the RBI plans to manage the government’s record borrowings. The central bank has kept traders guessing by making discreet purchases, largely of treasury bills, instead of announcing a calendar of open-market operations. In the process, RBI has boosted market’s belief of the authority being the buyer of last resort, which has kept yields in check despite massive debt supply.

“The best approach is to keep yields relatively stable through indirect intervention” while ensuring sufficient liquidity and giving a clear guidance on policy rates, said Suyash Choudhary, head of fixed income at IDFC Asset Management in Mumbai. “This is exactly what the RBI is so far doing.”

The RBI has bought 1.2 trillion rupees ($15.8 billion) of debt since the fiscal year began April 1, and conducted 100 billion rupees of ‘Operation Twist’ in April. The backstop has kept yields on the most-traded 2029 debt at 6.02%, relatively little changed from levels just before the 54% jump in federal borrowing was announced May 8.

While Das has shown a penchant for using unconventional tools by adopting a Federal Reserve-style Operation Twist and European Central Bank-like cheap funding to banks, an explicit yield control strategy won’t work in India, investors say.

A hard yield control policy may be “construed as distorting market signals,” Choudhary said. With the budget deficit set to widen, the RBI might not be comfortable in “leaning heavily” toward this policy, according to ICICI Securities Primary Dealership Ltd.

Fed, BOE

Yield curve control is a fallout of central banks in developed markets running out of tools with rates at near zero or even negative. While Bank of Japan adopted it in 2016, the Reserve Bank of Australia rolled out its own version this year. And there’s talk that the U.S. Federal Reserve and Bank of England may also consider it as a policy option.

Bank of Japan has a 0% target for the 10-year yield, while Australia has set a 0.25% target for the three-year yield after dropping rates to historic lows.

Authorities in emerging markets typically use market purchases to cope with excess debt supply. But Das in May said he will use all instruments and “even fashion new ones” as the RBI seeks to support an economy staring at its first recession in four decades. The RBI has cut rates by 115 basis points this year.

“There’s room for them to provide more explicit support to the long-end to bring down financing costs for the government,” according to a Deutsche Bank note. “The RBI also has the legal ability to enter primary auctions but they have yet to do so. This could change in coming months.”

For now, the authority has more room for conventional policy action, economists say.

“The immediate question to me is: can India lower interest rates more? I would say yes,” said Sergi Lanau, deputy chief economist at Washington-based Institute of Economic Finance. “India and most major emerging markets have policy rates way above zero. If they embark on programs that involve creating reserve money to buy government bonds, effective rates will fall below the policy rate.”

India’s federal and state governments may have to borrow net 17.5 trillion rupees this fiscal to finance their massive support packages, with the RBI having to buy 3-6 trillion rupees of bonds, according to ICICI Securities.

“Strong sporadic interventions around specific thresholds, which may not be keeping in specific with any script, could well be the way to implement” a soft yield control policy, economists A. Prasanna and Abhishek Upadhyay wrote in a report to clients.

©2020 Bloomberg L.P.