Doubling of RBI Bond Buying Suggests No Move to Direct Financing

RBI’s soft yield-control policy suggests it plans to keep the government’s borrowing programme afloat without direct financing.

(Bloomberg) -- The Reserve Bank of India’s decision to double secondary market bond purchases and its preference for a soft yield-control policy suggest Governor Shaktikanta Das plans to keep the government’s borrowing program afloat without breaking the monetary taboo of direct financing.

The restraint contrasts with some emerging-market central banks, including in Indonesia, that have agreed to buy billions of dollars of bonds directly from their governments to fill funding gaps amid the pandemic-fueled downturn. That approach carries risks, especially for inflation, the currency and the independence of the central bank.

Having so far managed to keep a lid on financing costs for the government, the RBI is unlikely to change its strategy, said Sergi Lanau, deputy chief economist at the Washington-based Institute of International Finance.

“The RBI seems very aware of the fiscal financing challenge but is reluctant to engage in direct financing of the deficit,” Lanau said. “This is understandable since history tells us central bank assists to fiscal policy are often abused.”

The RBI has so far cut interest rates by 115 basis points this year and adopted a Federal Reserve-style Operation Twist -- simultaneous purchase and sales of bonds of different maturities -- to control borrowing costs. This month, Das announced a package of measures, including 200 billion rupees of open market bond purchases, meant to reassure traders worried about a debt deluge.

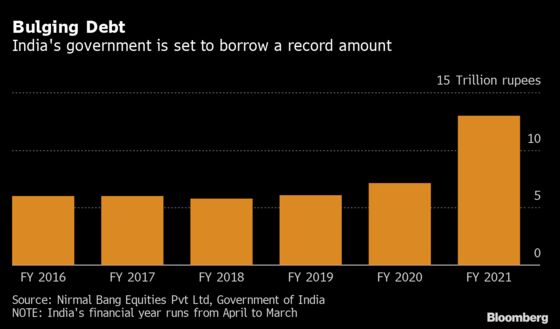

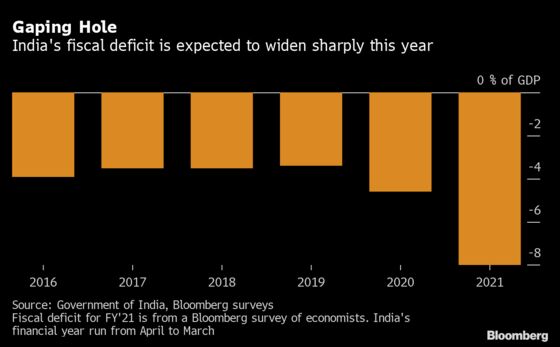

The yield on benchmark 10-year bonds has remained below 6% -- a level traders see the RBI trying to defend -- despite the government ramping up borrowings this fiscal year to an unprecedented 13 trillion rupees ($177 billion). That increase in debt could see India’s combined fiscal deficit surge to more than 10% of GDP.

Among reasons for the RBI’s reluctance on debt monetization may be the economy’s experience in the 1980s when deficit financing led to double-digit inflation. A repeat will go against the RBI’s primary mandate of bringing headline inflation to the 4% midpoint of its 2%-6% target range, and keep it from using conventional policy tools to support an economy headed for its worst annual contraction.

India’s Fiscal Responsibility and Budget Management Act bars the RBI from buying bonds directly from the government in the primary market. Besides, the government’s cautious strategy on fiscal stimulus compared to its peers like Indonesia could pay off.

Analysts at Nomura Holdings Inc. said in a recent note that while a wider fiscal deficit could still give rise to deficit monetization, they believe it poses less of a risk to Indian bonds than Indonesian debt, given New Delhi’s lower foreign bond ownership -- 2.3% of outstanding versus 28% in Indonesia.

Investors may also view the RBI’s credibility as less at risk than Bank Indonesia’s, according to Nomura analysts.

©2020 Bloomberg L.P.