Key Auction Looms for RBI as Traders Balk at India Yields

An auction of Rs 32,000 crore of bonds on Friday will show if the RBI can begin bending traders to its will.

(Bloomberg) -- Barely weeks into India’s new borrowing program, the nation’s sovereign bond traders and the central bank are shaping up for a third bruising battle.

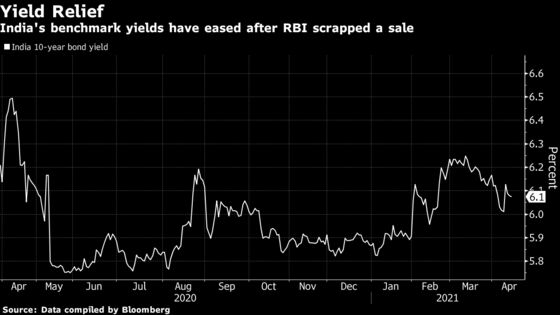

The Reserve Bank of India’s explicit assurance to buy 1 trillion rupees ($13 billion) of bonds this quarter has failed to encourage more purchases by traders. Underwriters were forced to rescue a five-year bond sale on April 9 and the RBI canceled an offering altogether on April 16 when traders demanded higher yields for benchmark 10-year debt.

An auction of 320 billion rupees of bonds Friday will show if the central bank can begin bending traders to its will, or whether the market could lose confidence entirely in its recent move toward quantitative easing. At stake is a near-record 12.1 trillion rupee government borrowing plan for this fiscal year that is key to helping the country combat a new wave of Covid-19 infections.

The South Asian nation is now the world’s second-worst hit country after the U.S., adding more than 200,000 cases daily for the last week. Soaring infections have compelled India’s financial and political capitals to impose movement curbs that can cripple economic activity. That has added to concerns about the need for greater fiscal stimulus, which in turn could push borrowing even higher.

The market will be watching to see if underwriters are leaned on again and the RBI accepts more than the scheduled amount, according to B. Prasanna, head of global markets, sales, trading and research at ICICI Bank Ltd. “This could be quite bad for risk appetite going forward and lead to investors keeping away from bond auctions, fearing secondary market selling from primary dealers at distress levels,” he said.

While the RBI isn’t alone in its tussle with bond traders, it is trying to contain inflation while many of its peers are striving to spur prices higher. Governor Shaktikanta Das has also added moral suasion to his policy tool kit, repeatedly urging traders to treat the bond yield curve as a “public good” because of its impact on borrowing costs in the broader economy.

Das has provided the market with a clearer roadmap for the next few months but traders want more clarity on how purchases of at least 3 trillion rupees will play out over the full fiscal year.

The yield on the benchmark 10-year bond fell two basis points to 6.05% on Thursday.

Traders continue to demand higher yields, citing domestic inflation pressures and the global reflation trade, and some have adopted strategies that present new challenges for policy makers.

One such approach to optimizing gains is by selling bonds first to the RBI under the new Government Securities Acquisition Programme, and then buying the same bonds later at auctions for a lower price, according to Dhawal Dalal, co-chief investment officer for debt at Edelweiss Asset Management Ltd.

In order to avoid this situation, the RBI should keep a sufficient gap between G-SAP purchases and scheduled auctions, he said.

ICICI’s Prasanna suggested policy makers adjust how they make bond purchases under the new regime.

“RBI should definitely look at tweaking the tenors of the bonds it buys under G-SAP and buy more of the 5-, 10- and 14-year bonds, rather than buying the shorter end,” he said. “The biggest concern for the market is supply of duration due to the heavy borrowing program schedule.”

©2021 Bloomberg L.P.