Bond Income Helps India Central Bank Pay Record Windfall

Bond Income Helps India Central Bank Pay Record Windfall

(Bloomberg) --

The Reserve Bank of India’s record payout to the government was helped by profits earned from its intervention in the country’s bond and foreign exchange markets.

Almost 70% of the 1.76 trillion-rupee ($24.5 billion) disbursement -- which was approved by the RBI on Monday -- was derived from the income the central bank earned on its investments, gains from changes to accounting of its foreign exchange policy and the fees it earned from printing notes and minting coins. The rest, about 526 billion rupees, comes from its surplus capital.

The RBI’s annual report, released Thursday, shows interest income jumped about 43% to 1.1 trillion rupees in the year ended June 30. Other income surged to 862 billion rupees from 44.1 billion rupees a year earlier.

“The reason for this is the record open market bond purchases in the financial year to March 2019,” said Pranjul Bhandari, chief India economist at HSBC Holdings Plc. in Mumbai. “It led to a high interest income.”

The central bank earned an additional 210 billion rupees from changes to the way it treats its foreign exchange intervention operations, an official told reporters, asking not to be identified citing rules.

Central banks generally buy and sell government bonds as part of normal monetary operations, affecting liquidity in the market by boosting or withdrawing cash into the system. In India, where a shadow banking crisis has caused a cash crunch, the RBI has been purchasing bonds to inject more funds into money markets.

Bhandari estimates the government bought 3 trillion rupees of bonds in the market in the fiscal year through March, making up more than 70% of sovereign bond issuance.

The windfall from the central bank couldn’t have come at a better time for Prime Minister Narendra Modi, who is under pressure to halt a sharp slowdown in the economy. The money gives New Delhi more fiscal options, including possibly lowering its market borrowings or boosting spending to shore up growth

The central bank said the inflation outlook was benign and the recent catch-up in the progress of monsoon and winter crop sowing has eased concerns. Nevertheless, India’s external sector outlook was vulnerable to downside risks from global developments.

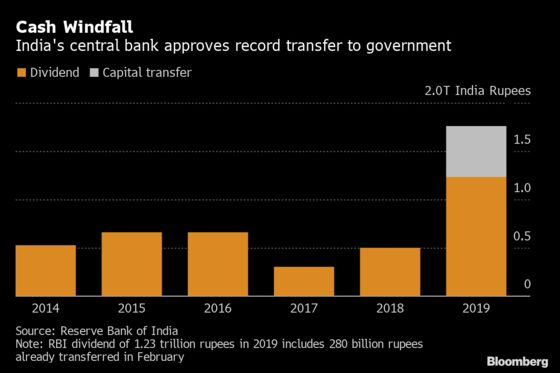

The RBI payout this year represents two parts: dividends and a capital transfer. The central bank pays dividends to the government every year, based on the profit from its investments and printing of notes and coins. It also holds substantial foreign securities in its investment portfolio, but interest income from that is seen lower than its domestic holdings because local rates are higher compared to those in the U.S., U.K or Japan.

The dividend of 1.23 trillion rupees is double the amount that had been transferred in recent years, and represents the entire net income of the RBI for the year ended June.

The capital transfer of 526.4 billion rupees is based on the recommendations of a panel set up to study how much excess capital the central bank holds.

The panel recommended, among other things, that the RBI’s economic capital -- made up of realized equity and revaluation balances -- should lie within the range of 20% to 24.5% of its balance sheet. It prescribed maintaining the realized equity -- or contingency buffer -- between 5.5% to 6.5%. That is lower than the 6.6% indicated by the think-tank Center for Advanced Financial Research and Learning, which is founded by the RBI.

The RBI board accepted both the recommendations, which took its payout to a record. But economists warned that future payments might not be as huge.

“The committee has lowered the prospect of a sizable transfer of RBI’s reserves over the next few years, as revaluation stores from the RBI’s balance sheet might be excluded from any excess capital calculation,” Radhika Rao, an economist at DBS Group Holdings Ltd. in Singapore, said in a note.

--With assistance from Unni Krishnan.

To contact the reporter on this story: Anirban Nag in Mumbai at anag8@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Karthikeyan Sundaram

©2019 Bloomberg L.P.