‘Stealth’ RBI Support May Turn to Large Scale India Bond Buy

India’s central bank may abandon years of austerity to vacuum up government debt directly.

(Bloomberg) -- India’s central bank may abandon years of austerity to vacuum up government debt directly after Prime Minister Narendra Modi’s administration raised its borrowing target to $159 billion, according to market participants.

Options being touted include increasing the use of tools already deployed, such as open-market purchases of bonds and Federal Reserve-style ‘Operation Twist,’ according to DBS Bank Ltd.’s Radhika Rao. If required, even primary market purchases or private placements could be considered, she said.

The Reserve Bank of India hasn’t directly bought sovereign debt since a law barring the practice came into effect in April 2006. But given the need for massive state spending to lift Asia’s third-largest economy from the pandemic-induced crisis, even officials who crafted the tougher rules have joined the growing number of advocates urging the RBI to buy the nation’s debt as it mulls more policy responses.

“The RBI will be concerned about market stability to ensure yields don’t spike and hamper monetary transmission,” said Shailendra Jhingan, chief executive officer at ICICI Securities Primary Dealership Ltd. “We expect OMO purchases to be the preferred route.”

Central banks across Asia have already been challenging taboos and creeping closer to monetization of debt. Indonesia has broken new ground in directly bidding at auctions while the Reserve Bank of New Zealand has said it is open-minded about such purchases.

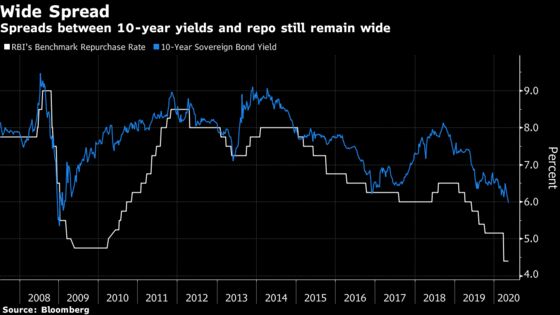

In the absence of any RBI action over the weekend, yields jumped by the most in three years on Monday. The yield on the 10-year debt climbed 20 basis points to 6.17% after rising as much as 27 basis points, the most since Feb. 2017. Benchmark yields may rise further to as much as 6.5% in the near term, according to Nirmal Bang Equities Pvt.

Bloomberg calculates the RBI’s share of the government debt next year may exceed its current 15% holding, bigger than Bank Indonesia’s estimated 11% and closer to Australia and New Zealand’s 24% and 39%, respectively.

RBI spokesman Yogesh Dayal did not respond to an email seeking comments.

‘Stealth Support’

Late on Friday, the government said it will borrow 12 trillion rupees ($159 billion) in the year that began April 1, 54% more than budgeted. Half of this will be raised by the end of September. The increase -- which signals a major slippage in fiscal deficit amid rising pressure on revenue -- will boost the size of weekly auctions to 300 billion rupees.

With states also facing a fiscal crunch, the gross combined borrowing may be as much as 20 trillion rupees this year, according to IDFC Bank Ltd.

Traders had factored in a spike in borrowing; they just didn’t think it would come so soon. Hours before the statement from New Delhi, bond yields in Mumbai had fallen to the lowest in over a decade, as the market cheered the launch of a new 10-year paper. The optimism also reflected bets that the RBI would continue what DBS calls “stealth support.”

Data show the RBI bought a net 910 billion rupees of debt in the secondary market in April.

ICICI PD’s Jhingan said the entire extra borrowing will now have to be picked up by the central bank to ensure the market stays stable. That’s because all of the RBI’s measures since the beginning of March -- slashing its policy rate, 400 billion rupees of announced OMOs and a 100-billion rupee Operation Twist -- have failed to meaningfully reduce borrowing costs for companies.

The RBI has been providing its support, with its balancesheet expanding from 25.7% of GDP as of May from 21.7% in Dec. 2019, IDFC Bank said. The increase represents support provided by its long-term repo operations, targeted lending operations, open-market purchases and higher ways and means advances, it said.

Governor Shaktikanta Das may start getting uncomfortable if the ratio of rupee-asset holdings approaches 30% of the RBI’s AAA-rated foreign-currency reserves, Saugata Bhattacharya, chief economist at Axis Bank Ltd., wrote in a note.

The RBI didn’t say whether the government’s additional borrowing will only make up for lost revenue or whether it would finance new spending. Barclays Plc pegs the budget deficit at 5.75% of gross domestic product this financial year versus the 3.5% target.

The gap is likely to be around 5.5% of GDP for the year to March 2021, a finance ministry official with knowledge of the matter said Monday. There’s no plan by the RBI to buy sovereign debt directly and the government may end up borrowing less than the revised target of 12 trillion rupees, the official said, asking not to be identified citing rules on speaking to the media.

“We believe RBI stands ready to monetize a big portion of this slippage,” said Ananth Narayan, a professor of finance and former head of trading for South Asia at Standard Chartered Plc. “So far, it has already effectively monetized the deficit to the extent of 2% of GDP.”

©2020 Bloomberg L.P.