Xi Sends Warning to Investors With Delayed Huarong Lifeline

Xi Sends a Warning to Investors With Delayed Huarong Lifeline

(Bloomberg) -- China Huarong Asset Management Co. ultimately proved too big to fail, but its protracted bailout process shows Beijing’s determination to punish creditors who ignore risks in heavily indebted companies.

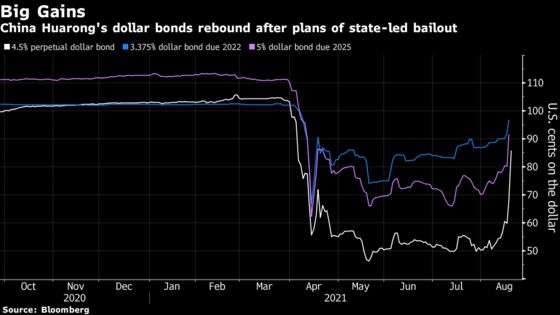

The almost five-month saga triggered some of the most extreme swings ever for an investment-grade Chinese bond issuer, changing the way even seasoned money managers evaluate the nation’s $12 trillion credit market. While some Huarong bonds rallied to 97 cents on the dollar after the company unveiled a recapitalization by state-backed investors late Wednesday, the rescue came too late for many bondholders who sold at heavy losses earlier this year.

For President Xi Jinping’s government, there’s a lot to like about a Huarong resolution that introduces more market discipline without the need for a messy default that could stoke broad financial contagion. The risk is that this muddle-through strategy -- and Beijing’s opaque approach to dealing with troubled borrowers -- drives away investors who want more clarity on the rules of the game in Chinese credit.

“There’s clear desire from the government to impose more discipline in the system,” said David Loevinger, sovereign analyst at TCW Group Inc. and former senior coordinator for China affairs at the U.S. Treasury. “That said, Huarong is so big and so interconnected with the financial system. Investors are still struggling to figure out where is the line, and who is on the safe side of the line.”

Huarong’s capital will be replenished by state-owned investors including Citic Group, China Insurance Investment Co. and China Life Asset Management Co., the nation’s biggest bad-loan manager said in an exchange filing Wednesday. The unspecified amount of funds will help the Huarong continue to operate and meet a minimum regulatory capital requirement. Huarong assured investors it has no plan to restructure its debt, while announcing a record $15.9 billion loss for 2020.

The statement confirmed a Bloomberg report that Huarong was poised to receive fresh capital as part of an overhaul plan, according to people familiar with the matter, who put the amount being discussed at about 50 billion yuan ($7.7 billion). Control of the company would shift to Citic, the people had said, though details were still being finalized and could change.

For the more speculative funds with a high tolerance for risk, Huarong bonds may have been the trade of a lifetime. But the volatility made the notes toxic to many of Huarong’s core investors, who had counted on a quick resolution for the quasi-sovereign issuer.

“Just because the government has ultimately decided to bailout Huarong, it doesn’t mean the damage hasn’t been done,” said Jim Veneau, head of fixed income Asia at AXA Investment Managers. “There are economic losses and someone is bearing them. If that support were to be forthcoming, it should have been much earlier.”

The Communist Party has long put a premium on financial stability, but it also increasingly wants to investors off the assumption that overextended companies will always be saved. President Xi said this week China must prevent causing follow-on risks in the process of defusing financial concerns.

Huarong’s bailout falls somewhere in the middle. It addresses moral hazard by penalizing some long-term investors who failed to assess the risks involved in lending to Huarong. But at the same time, the rescue shows that implicit guarantees still exist, depending on the company. China Evergrande Group -- a privately-owned developer -- may face a more severe punishment, Citigroup Inc. analysts have said.

“China’s willingness to prop-up heavily indebted borrowers is increasingly selective,” said Suvir Mukhi, co-chief investment officer at Income Partners Asset Management. “Thus we continue to focus very closely on stand-alone credit profiles of issuers, rather than relying on the expectation of state support.”

Mukhi said his firm bought Huarong bonds prior to the recent rally.

With about $21 billion in outstanding offshore bonds, Huarong is one of the bigger issuers in China’s investment-grade market. Fear of contagion was particularly evident in April, with a Bloomberg Barclays index of high-rated dollar notes showing spreads blowing out to a 13-month high. Bonds of other debt managers, which rallied on Thursday, were also caught by the Huarong selloff earlier in the year.

Existing Huarong shareholders will likely see the value of their stakes plunge as the company recognizes losses on non-performing assets, two people familiar with the plan said. Warburg Pincus and Goldman Sachs Group Inc. are among a group of investors that bought a $2.4 billion stake in Huarong before it went public in 2015. Huarong shares remain suspended in Hong Kong.

Huarong has so far repaid all its bonds on time and said last month it would redeem a $500 million perpetual note in September, helping to boost market confidence. The company has also reached agreements with state-owned banks to ensure it can meet obligations through at least the end of August, Bloomberg reported in May.

If the potential strategic investment is implemented, it will replenish Huarong’s capital, consolidate its foundation for sustainable operations, and ensure it meets regulatory requirements, the firm said on Wednesday.

“This marks the end of the Huarong crisis,” said Yong Zhu, who manages about $6 billion at DuPont Capital Management in Wilmington, Delaware and owns Huarong bonds. “Huarong is one of the key strategic SOE companies -- it’s like the government’s own son. But investors need to be careful. Not every SOE will be bailed out.”

©2021 Bloomberg L.P.