Wall Street Circles as China Brokerages Struggle for Returns

Wall Street Circles as China’s Brokerages Struggle for Returns

(Bloomberg) -- China’s more than 130 brokerages, who have a $21 trillion market to trade and make deals in, aren’t very good at making money.

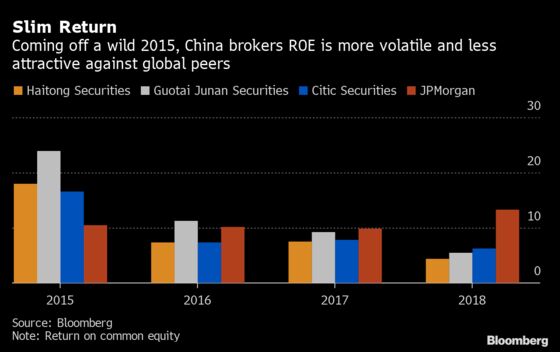

Their return on equity last year was just about half of Wall Street’s powerhouses, who are now preparing to rush in as the world’s second-largest economy opens its financial market fully to foreign banks. Of the some 80 sectors in Shanghai’s benchmark index, the industry ranks near the bottom, far, far below the more than 30% in returns China’s distillers make, for example.

The scant returns are a result of fierce competition among the firms, a conservative approach to riskier ventures and a distaste for leverage. The financial opening this year will likely provide a jolt to the industry, forcing consolidation and winnowing out of those that can’t compete.

“Those who have a core competitiveness and are better positioned to seek higher returns from managing risk will get a bigger slice of the pie,” said Liu Yiqian, general manager of the innovation and development division in Shanghai Securities. “We might see 7 to 10 top brokers dominate the market.”

At the top of the pyramid sits Citic Securities Co., which last year reported a return on equity of 7.8%. It’s expected to take a big role in any consolidation and has already been making moves by buying rival Guangzhou Securities Co. and a number of others over the past years.

Authorities in Beijing want more concentration in the industry, calling for the creation of “aircraft-carrier sized” brokerages that can compete with the likes of Goldman Sachs Group Inc. as the markets open. Together, China’s brokers have assets that are equal to what Goldman sits on by itself.

Speculation over a consolidation, and ample liquidity from China, has kept sector’s shares buoyant even though it has recently been dragged down by the market rout. A Bloomberg index of Chinese brokers trading in Hong Kong has slid 24% so far this year, about the same as the benchmark Hang Seng Index. The sector is trading at an average price to earning ratio of 9.34 times, compared with 8.88 for the Hang Seng.

“We want to yield higher return on equity to give the best returns to our shareholders, but also to do it within our risk management capability,” said Yang Minghui, Citic’s president, at a press briefing on Friday. “It will be challenging, but we are very inspired to improve our ability in designing products, investment and trading services, as well as risk management. “

Yang said the firm doesn’t have any acquisition plans “at the moment.”

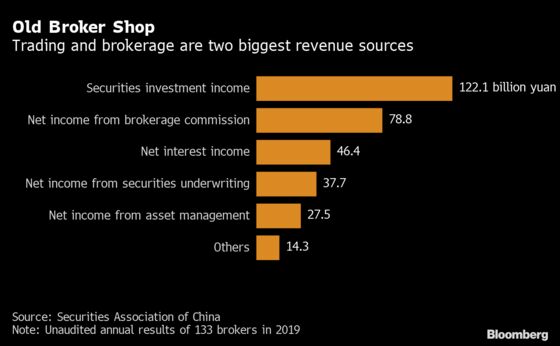

The bulk of the firms have largely been involved in less capital demanding business such as trading and underwriting after three decades of development. Their mom-and-pop approach has struggled amid an exodus of retail investors. Now they face the challenge of building out a broader menu of investment banking services, such as market making and prime brokering.

“The trillion-yuan trading volume every day should have brought securities firms a bonanza, but after rounds of price wars the margins are actually very low,” said Dong Chen, deputy president of Changchun-based Northeast Securities Co.

Underwriting fees and commissions are tight. Share sales in China also face a lengthy reviewing process and are subject to an unofficial valuation cap of 23 times of earnings, leaving brokers little room to differentiate their services other than cutting prices to win mandates.

The weighted average gross spread, a key measure on the profitability of IPOs, is about a fourth in China of what banks make in the U.S. The commission rate in China slid to just below 3 basis points, or 0.03 percentage point, in the middle of last year, from 8 basis points in 2013. Online brokers, such as Eastmoney, charge fees below 2 basis points.

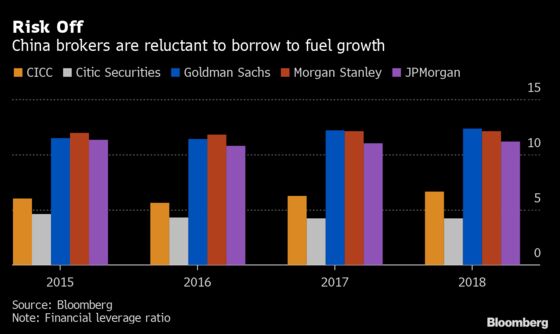

While competition is largely to blame for the margin pressure that’s hurting returns, their conservative approach to borrowing is also holding brokerages back.

“Compared to Wall Street banks Chinese brokers borrow far less, and they don’t leverage that much money to more capital-intensive businesses that generate higher returns,” said Wang Jian, chief analyst at Guosen Securities Co. As competition heats up, some brokers might ratchet up leverage and expand into new areas such as derivatives and market making, he said.

©2020 Bloomberg L.P.

With assistance from Bloomberg