One China Bank Is Making Capital More Expensive for Many Lenders

One China Bank Is Making Capital More Expensive for Many Lenders

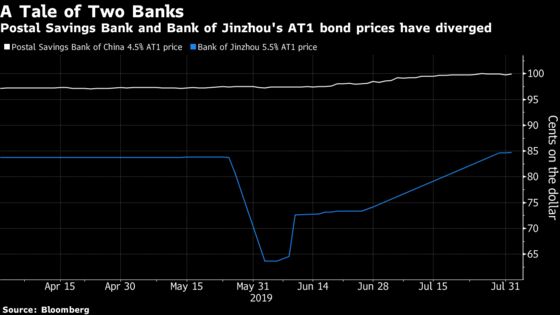

(Bloomberg) -- Just two years ago, a little-known Chinese lender could raise capital from global investors at a yield of 5.5%, only 1 percentage point more than the debt of the nation’s leading retail bank, Postal Savings Bank of China Co.

But that all changed in June, when investors grew concerned about the outlook of the firm, Bank of Jinzhou Co. Yields on its so-called Additional Tier 1 notes blew out to over 21% after its auditors resigned citing inconsistencies in its loans, before coming back down to 11.4% this week, according to Bloomberg-compiled prices. Loss-absorbing securities from similar issuers, used to fulfill capital requirements, have also come under pressure.

The roller coaster ride for bond buyers is a stark reminder of the risks of investing in China’s credit markets. Growing market concern about smaller lenders has pushed up bond spreads to levels where it may not make economic sense for banks to buy back callable capital notes at the first opportunity they can, contrary to the expectations of investors when they first got into the debt. That’s putting further downward pressure on the bank bonds, at a time when investors are no longer counting on an implicit government guarantee for every Chinese financial institution.

“There is definitely still some concern of smaller Chinese banks not calling their Additional Tier 1 securities,” said Nicholas Yap, desk analyst at Nomura International (HK) Ltd. There’s a “fundamental divergence” between big Chinese lenders and smaller banks, and that “will likely persist going forward,” he said.

Amid the turmoil, smaller Chinese lenders are finding it harder to raise funds. Investors are going to demand “a lot” of premium for small banks to issue bonds offshore, meaning that funding channel for capital debt is “pretty much closed” for them, according to Arthur Lau, head of Asia ex-Japan fixed income at PineBridge Investments. That’s a potential negative factor for China’s slowing economy because those lenders are a key source of credit to small and medium-sized companies.

Bank of Jinzhou didn’t immediately respond to an email requesting comment.

While most AT1 dollar bonds sold by weaker Chinese banks don’t face call dates until 2021 or later, their current high yields suggest it may not make sense for the issuers to redeem the bonds at the first opportunity possible.

The yield on Bank of Jinzhou’s 5.5% perpetual bonds, for example, is higher at the moment than the rate of 348.6 basis points over Treasury yields that would be applied if the notes aren’t called.

In fact, most smaller Chinese lenders don’t have an economic incentive to call their AT1s in 2021 and beyond, according to David Marshall, co-head of Asian bank research at CreditSights Inc.

Bank of Jinzhou’s liquidity crunch came soon after the Chinese government took over Baoshang Bank, the nation’s first seizure in more than two decades. Support from Chinese state-owned financial heavyweights, including Industrial & Commercial Bank of China Ltd., helped boost Bank of Jinzhou’s AT1 bonds. Still, the stumbles among financial institutions have been a wake-up call for investors.

Government Support

The potential for a bank to not call its Additional Tier 1 bonds “is usually not assumed in Asia,” according to Matthew Phan, credit analyst at Bloomberg Intelligence. “It is expected that the Chinese government or another big shareholder would inject capital.”

Chinese authorities have been pushing to reduce leverage in the banking system, posing challenges for smaller lenders burdened with heavy bad debt loads. While regulators have been trying to ease market jitters about the sector, further consolidation may be in the works.

“As more banks are slowly ‘let go’ to market forces or forced into marriages with better capitalized institutions,” there could be more events in coming months, according to Manu George, director of fixed income at Schroder Investment Management.

To contact the reporters on this story: Denise Wee in Hong Kong at dwee10@bloomberg.net;Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum, Neha D'silva

©2019 Bloomberg L.P.