PBOC Seen Front-Loading Policy Action Amid Economic Threats

PBOC Seen Front-Loading Policy Action as Economic Threats Loom

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

China’s central bank has fueled expectation it will ease monetary policy early this year with its vow to take proactive action to stabilize growth in 2022.

A growing number of economists are predicting the People’s Bank of China will cut banks’ required reserves as well as policy interest rates in the first quarter, as fresh pandemic outbreaks and lockdowns add to headwinds for an economy already buffeted by weak private consumption and a housing market crisis.

The first quarter could be a “key window” for China to further ease monetary policy before the U.S. hikes interest rates, according to a report Friday in the China Securities Journal, which is run by the official Xinhua News Agency. That report cited brokerages including Huatai Securities.

BNP Paribas SA economists expect a 10-basis point cut in the medium-term lending facility rate in January or February and a 50-basis point reduction in the reserve requirement ratio in the first quarter, they said in a briefing Thursday. Goldman Sachs Group Inc. economists also forecast a RRR cut in the first quarter, according to a note last week.

“In case that the pandemic leads to further lockdown, we see the possibility for the PBOC to quicken its pace,” said David Qu, China economist at Bloomberg Economics, who forecasts a 10-basis point cut in the MLF rate in the first quarter and a RRR cut potentially late in the first quarter or early second quarter.

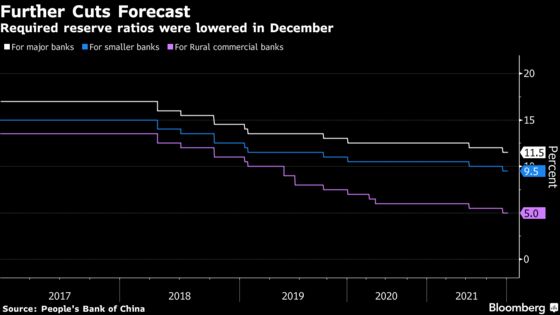

The PBOC is likely to transition to an easing cycle this year after providing only targeted support in 2021 while guiding credit growth to slow down for most of last year. It allowed banks to lower the one-year benchmark lending rate by 5 basis points in December, its first reduction in 20 months, and cut the RRR by 50 basis points in the same month.

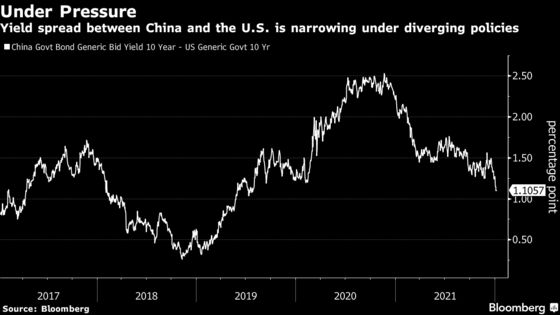

The divergent policies between the PBOC and a Federal Reserve that’s set to hike rates is narrowing the yield spread between 10-year U.S. Treasuries and Chinese government bonds, which is around 110 basis points now compared with about 200 basis points a year ago. This could put downward pressure on the yuan, which is hovering around its highest level since May.

In addition to any further monetary stimulus, the government is looking to increase fiscal spending early in the year, with the National Development and Reform Commission telling local governments to spend more in the first three months of this year.

Read more: China Sees Investment Boost in Early 2022 on More Bond Sales

More stimulus could benefit China’s battered stocks that are sensitive to liquidity conditions in the financial markets. The CSI 300 has fallen more than 2% this week, the worst start to a year since 2016. The Nasdaq-style ChiNext Index fared even worse, down nearly 7% as investors dumped expensive stocks.

Uncertainties Ahead

There are still many uncertainties to the outlook, and the release of the final economic data for 2021 over the next few weeks will give a more complete picture of the health of the economy and could change expectations on what the PBOC needs to do.

Fourth-quarter economic data will be released Jan. 17 and December credit and lending data will likely be announced next week. The 500 billion yuan ($78 billion) of medium-term loans maturing on Jan. 17 will provide the PBOC an opportunity to cut rates, add extra liquidity to the economy ahead of the Lunar New Year, or even do both.

Zhou Hao, a senior emerging market economist at Commerzbank AG, said the PBOC could choose to hold off its actions in the first quarter because it tended to avoid conforming to strong market expectations in the past. Inflation could also rise faster than expected over the Lunar New Year due to a low base last year, which would restrict the space for easing, he said.

©2022 Bloomberg L.P.

With assistance from Bloomberg