Brutal Week in Global Credit Markets May Just Mark the Beginning

Panic Selling Sparks Worst Week For Asian Bonds Since 2014

(Bloomberg) -- Fears about the coronavirus hammered credit markets across the globe this week and shut out almost all borrowers looking for fresh cash in the U.S. and Europe.

There’s plenty of hope but few signs that next week will be any better.

Wall Street debt bankers sat idle for a fifth straight day as corporate borrowers waited out the global market volatility. Bausch Health Cos. delayed an $8 billion debt refinancing, and other junk-rated companies in the U.S. and Europe pulled offerings that had been announced before the sell-off.

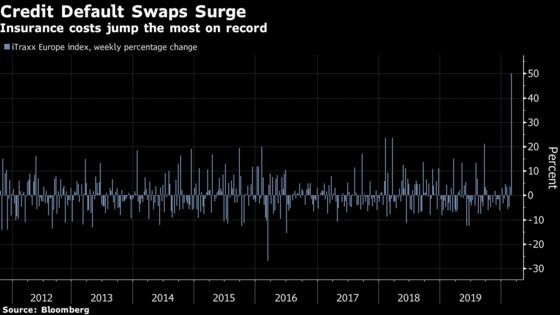

With the World Health Organization raising the global risk of the coronavirus to “very high”, fear of global economic fallout sent risk premiums surging. For U.S. investment-grade bonds, yields relative to Treasuries jumped 17 basis points, putting them on pace for the biggest weekly increase since 2011. Euro high-grade spreads widened the most since March 2015, while Asian dollar bonds were on track for the worst week since 2014.

Piling Up

The credit-market stall has left investor cash piling up and corporate borrowers ready to tap into yields that -- even after the selloff -- remain well below historical averages. The outlook has become so uncertain that a Bloomberg survey of Wall Street bond dealers suggested they expected either another week of zero issuance or a deluge of as much as $50 billion in sales.

“At some point you have got to buy this,” said Andrew Feltus, a money manager at Amundi Pioneer Asset Management in Boston. “It is either the end of the world or everything has been put on sale pretty aggressively.”

Many investors are bracing for rocky months ahead as they price in the potential for a significant blow to the global economy from a virus that continued to spread. It also comes at a time when companies, particularly in Europe, are usually readying for a March bond-sale deluge.

New Deals?

“Fear is spreading faster than the virus,” said Gordon Shannon, a London-based portfolio manager at TwentyFour Asset Management, which oversees 17.4 billion pounds ($22 billion). “Spread levels can go a lot wider.”

European bankers are estimating just 10 billion euros ($11 billion) of new corporate and sovereign debt may come next week, according to a Bloomberg survey. That’s far cry from an average of 46 billion euros a week to start the year.

The turmoil put an increasing number of planned junk-bond sales on ice. Fugro NV, a geological data provider pulled a planned 500 million euro bond sale Friday, citing market conditions. Minimax Viking and NorthRiver Midstream both yanked U.S. loan offerings earlier in the week.

Bausch Bails

Bausch, the drugmaker once known as Valeant Pharmaceuticals, put the brakes on a $5.14 billion loan it had been marketing and a $3.25 billion bond offering that was originally expected to be announced this week, according to people familiar with the matter who asked not to be identified because they’re not authorized to speak publicly.

“Primary will be quiet for a while -- I doubt issuers will come to the market until risk sentiment stabilizes,” said Tim Winstone, a portfolio manager at Janus Henderson Group Plc.

The U.S. investment-grade company bond market faces its first week without a sale since July 2018, a rarity outside of summer lulls and holiday shutdowns. Europe has only seen two company deals this week totaling less than 1 billion euros. That compares with 20 billion euros of issuance from financial and non-financial companies in the equivalent week last year, according to data compiled by Bloomberg.

Still, if issuers do bring forward deals, they may find willing buyers. This week’s limited number of syndicated bond sales in Europe all found reasonable demand. Global bond funds had a 60th week of net inflows, with investment-grade funds pulling in $11.8 billion, according to a Bank of America note, citing EPFR Global data.

Investors in the U.S. felt more jittery. They pulled $283.5 million from the biggest leveraged loan exchange-traded fund, the most on record. Funds that buy up U.S. high-yield bonds saw their worst weekly outflow since 2018, according to data compiled by Refinitiv Lipper.

“Certain issuers and tenors can still work in this type of market with a bit of new-issue premium,” said Tom Moulds, a senior portfolio manager at BlueBay Asset Management. “I think next week you will certainly see some issuers trying to come to the market.”

Investors have been avoiding riskier debt. Funds that buy U.S. high-yield bonds saw their worst weekly outflow since 2018, according to data compiled by Refinitiv Lipper. And funds that buy leveraged loans had withdrawals of $952 million in the week ended Feb. 26.

Week of Turmoil

In Asia, where companies have continued to issue debt, spreads on Asian dollar bonds widened 5 to 10 basis points Friday, according to traders, as a sell-off that started last week intensified. JPMorgan Private bank advised clients to take profit on borrowers with weaker structures and longer duration, according to Anne Zhang, the firm’s head of Asia fixed income.

“The markets are in a state of panic,” said Ek Pon Tay, portfolio manager for emerging-market fixed income at BNP Paribas Asset Management.

--With assistance from Finbarr Flynn, Brian Smith, Denise Wee, Jeannine Amodeo, Rebecca Choong Wilkins, Hannah Benjamin and Davide Scigliuzzo.

To contact the reporters on this story: Claire Boston in New York at cboston6@bloomberg.net;Tasos Vossos in London at tvossos@bloomberg.net;Priscila Azevedo Rocha in London at pazevedoroch@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, ;Shannon D. Harrington at sharrington6@bloomberg.net, Adam Cataldo

©2020 Bloomberg L.P.