Trading Losses Seen No Cause for Panic on Top Oil Refiner

Oil Trading Losses May Be No Cause for Panic on China's Sinopec

(Bloomberg) -- Sinopec Corp.’s trading losses shouldn’t deflect investors from the potential opportunity presented by its shares holding near a two-year low.

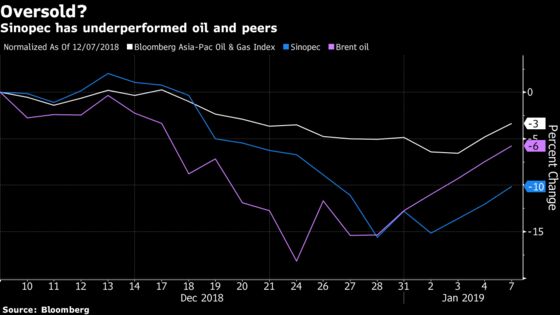

The refining giant, officially called China Petroleum & Chemical Corp., has slumped 10 percent in the past month amid a global oil rout and after it reported losses on derivatives linked to crude prices at its main trading unit Unipec. That’s made it the second-worst performer on the Bloomberg Asia Pacific Oil & Gas Index over the period.

Investors have been too bearish over the trading losses, according to Morgan Stanley, which maintained its overweight rating on the stock. The company is better positioned than peers to deliver stable and strong free cash flow, China International Capital Corp. said, adding that the stock remains its top pick among oil and gas companies over the long run.

“We believe the market expectation for the trading loss is too bearish, and we think this has introduced a good buying opportunity,” Morgan Stanley analysts including Andy Meng said in a note dated Sunday. The company is unlikely to book a big loss in the fourth quarter, they said.

The company, which hasn’t disclosed the size of Unipec’s losses, said Friday they were related to the unit’s hedging transactions, unearthed during regular supervision and that independent auditors are looking into the issue.

Price Targets

The stock has rebounded 6.3 percent to HK$5.75 as of Tuesday, since bottoming at a two-year low on Dec. 28 after the losses were announced. While at least seven analysts tracked by Bloomberg have cut their price targets on Sinopec over the past month -- which coincided with a collapse in global oil prices -- the stock is still far below the consensus estimate of HK$8.

Sinopec has a price-to-earnings ratio of 8.1 times, compared with an average of 11 times for 20 global peers including Exxon Mobil Corp. and Royal Dutch Shell Plc, according to data compiled by Bloomberg. That makes it one of the lowest valued oil stocks in the world. Almost all the analysts covering Sinopec have the equivalent of a buy rating on the stock, the data show.

The exception is Citigroup Inc. The bank downgraded Sinopec to a sell, saying the company will barely break even in the fourth quarter because of an estimated 20 billion yuan ($2.9 billion) inventory loss -- or drop in value of crude and products it has in storage because of the crash in oil prices -- as well as a potential 7.6 billion yuan hit from Unipec. The trading issue raises concern about corporate governance, Citi analysts including Toby Shek said in a Jan. 4 note, adding that investors might be too optimistic on dividends.

Earnings Outlook

As of Tuesday, Sinopec is expected to see fourth-quarter net income of about 15.5 billion yuan compared with 11.8 billion in the same period last year, according to the average of 12 profit estimates compiled by Bloomberg. The company will probably publish results at the end of March.

Sinopec raised its dividend payout in August after reporting record half-year earnings, fueled partly by improving refining profits.

“The potential negative impact of the incident has been priced in,” CICC analysts Nelson Wang and Chen Lu wrote in a note Monday, referring to the losses at Unipec. “Its higher-than-peer dividend yield is still a bright spot that merits attention.”

To contact the reporter on this story: Aibing Guo in Hong Kong at aguo10@bloomberg.net

To contact the editors responsible for this story: Ramsey Al-Rikabi at ralrikabi@bloomberg.net, ;Charlie Zhu at qzhu46@bloomberg.net, Jasmine Ng, Jason Rogers

©2019 Bloomberg L.P.