Markets Await Outcome for Opaque Bond Tied to Evergrande

Nervy Markets Await Outcome for Opaque Bond Tied to Evergrande

(Bloomberg) -- China Evergrande Group has already fallen behind on payments to banks, suppliers and holders of onshore investment products, and hasn’t given any indication that it paid two recent dollar bond coupons.

Now the world’s most indebted developer may be facing its next big debt test, underscoring the broader risks of opaque obligations in credit markets already on edge. Shares in China Evergrande Group and its property management unit were suspended from trading in Hong Kong Monday with no reason given.

People familiar have said that a dollar note with an official due date of Oct. 3 issued at an initial amount of $260 million by an entity called Jumbo Fortune Enterprises is guaranteed by Evergrande. As the maturity was a Sunday, the effective due date is Monday. The issuer is a joint venture whose owners include Hengda Real Estate, Evergrande’s main onshore unit.

Nonpayment of the bond principal would constitute a default as the note has no grace period, although five business days would be allowed if failure to pay is down to administrative and technical error, according to the people. Details of the guarantees weren’t broadly known as the note prospectus isn’t publicly available and the deal wasn’t listed on exchanges.

Any failure to pay Jumbo Fortune’s note may also pose a risk of cross-default for Evergrande’s other bonds, according to Bloomberg Intelligence analyst Daniel Fan. Creditors of the Jumbo note could potentially ask the trustee to declare a formal default if they achieve a minimum threshold of investors, and that could trigger holders of other dollar bonds to do the same, he said.

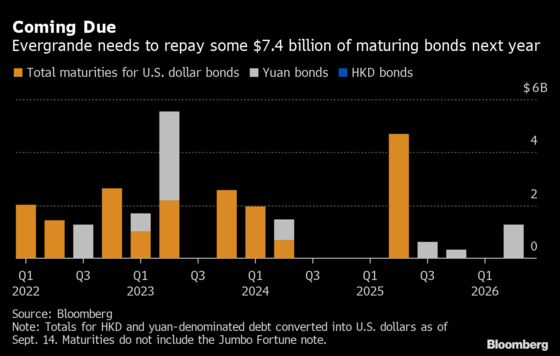

Uncertainly over the full extent of Evergrande’s debt load, beyond its more than $300 billion reported in liabilities, has plagued investors since a liquidity crisis at the firm stoked fears of a collapse that could trigger financial and economic contagion. Authorities ranging from Federal Reserve officials to Hong Kong’s central bank are looking into just how exposed financial institutions are to the crisis.

Standard Chartered’s head of China macro strategy Becky Liu expects Evergrande has more structured products such as guaranteed bonds, similar to the Jumbo Fortune note, with offshore dollar bonds making up just 6% of the firm’s total reported liabilities.

The law firm White & Case is advising various investors with regards to Jumbo Fortune, a spokesperson for the firm said.

There was no response from Evergrande to a request for comment about its interest payments or debt guarantees.

Debt crises historically have a way of worsening when obligations that had flown under the radar suddenly start showing up on screen. In the 2007-2008 global financial crisis, opaque mortgage-backed securities whose risks were hard to quantify played a major role. More recently in China, credit markets have at times been shaken by uncertainty about debt guarantees and intertwined obligations that were excluded from balance sheets.

Cross-guarantees have been a problem for China over the past decade with the rise of shadow banking, said Andrew Collier, managing director of Orient Capital Research in Hong Kong. “There is little ability to find out the size of the problem until there is a debt blowup and creditors worry about not getting paid.”

| Read more on the latest at Evergrande: |

|---|

|

Some Evergrande dollar securities have repayment acceleration provisions which stipulate that any indebtedness reaching $20 million could constitute an event of default, according to the offering memorandum of notes seen by Bloomberg. Creditors aren’t able to take legal action until bonds are formally declared to be in default.

While creditors have the option of filing lawsuits in an offshore court to enforce Evergrande’s payment obligations, “practically, bondholders may enter into some informal standstill and negotiate with the issuer,” said Fan at Bloomberg Intelligence.

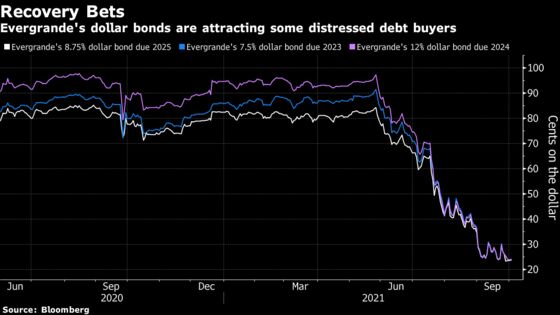

Still, some investors are betting that the bond prices don’t reflect the boost that could come from any recovery in a restructuring scenario. Firms such as Marathon Asset Management and Saba Capital Management have been building their positions in the debt, Bloomberg reported in September. Evergrande’s 8.25% dollar bond due March 2022 rose about 3 cents on the dollar to 28 cents following the report of Hopson Development’s stake sale, according to credit traders in Hong Kong.

The embattled developer isn’t the only firm adding to its debt piles with bonds that aren’t listed on exchanges and may lack much publicly available information. Private placements are popular among China’s real estate firms as these securities can be simpler to arrange than public deals -- they’re typically sold to a small group of investors with no expectations about the size and more room to negotiate on pricing.

Evergrande is likely to have more securities of a similar kind and “if holders don’t tell, no one will know of such debts’ existence,” said Ting Meng, senior Asia credit strategist at ANZ Banking Group Ltd.

©2021 Bloomberg L.P.

With assistance from Bloomberg