Key Part of China Shadow Banking Faces Doubling of Defaults

Key Part of China’s Shadow Banking Faces Doubling of Defaults

(Bloomberg) -- China’s $3 trillion trust industry, a key alternative source of funds for weaker companies, risks sending shock waves through the nation’s financial system with defaults among its investment products predicted to double this year under the strains of the coronavirus outbreak.

The once fast-growing pocket of shadow banking in China has 5.4 trillion yuan ($766 billion) in trust offerings coming due this year, high-yield products backed by loans that are sold to banks, institutional investors and wealthy individuals. About 300 of these products will go into default compared with last year’s record of 118, estimated Xu Zijun, a Beijing-based senior analyst at Reality Finance Research.

A hint of the wider danger came last month when Anxin Trust Co., a particularly aggressive shadow lender, said the government had been involved in its rescue plan to avoid triggering “systemic financial risks.”

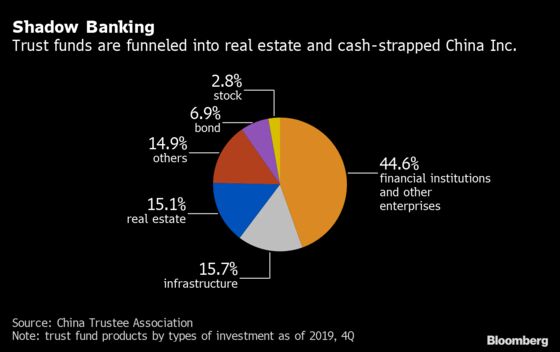

While Anxin has struggled for some time, its latest difficulties emerged as Chinese companies are rocked by the fallout of the virus outbreak that had shuttered large swathes of the economy. China’s 68 trust companies are on the forefront of the calamity given they count property developers, manufacturers and local government financing vehicles among their biggest borrowers.

“Borrowers behind the trust products are those with a higher risk,” said Yang Hao, an analyst at Nanjing Securities. “It represents the most vulnerable part of corporate financing and when a crisis comes, this is the first link to go awry.”

The sector’s asset quality will probably continue to deteriorate this year as slowing growth pressures highly leveraged borrowers or those heavily dependent on shadow banks, Moody’s Investor Service said last month. Those stresses could ripple out to other parts of the system, said Michael Taylor, chief credit officer for APAC at Moodys. There could be direct exposure for banks owning trust companies and an indirect impact to lenders via common borrowers and more generalized risk aversion, he said.

More than 1,500 trust products with a value of 577 billion yuan were designated as risky at the end of last year, according to the China Trust Association, up from about 870 a year earlier. In fact, there were just two firms in the industry that had avoided defaults as of end 2019, Reality Finance’s Xu said.

On the other side of these increasingly precarious products are wealthy investors, asset managers and banks such as China Zheshang Bank Co. and Heihe Rural Commercial Bank Co., which are among financial firms suing Anxin to recoup 1.7 billion yuan.

China’s regional banks don’t need another jolt. Authorities have already been forced to bail out or seize three lenders and quell bank runs by nervous depositors in the past year. Banks could face as much as $800 billion in loans going sour following the outbreak, rating firm S&P Global has said.

Reined In

Still, the risks from the trust sector could have been worse. Concerned over a rapid debt-build up, authorities have been reining in the trust companies, bringing their assets under management down 18% from a peak in 2017. A sweeping set of stringent asset management rules has also dented the appeal of their products.

Taylor at Moody’s said the government has the tools at hand to handle the build up of stress in the trust sector. China’s banking regulator on Tuesday proposed to ease the restriction on foreign investments in trust firms by removing the minimum $1 billion assets requirement on the buyer.

Regulators stepped in to save Anxin after the Shanghai-based firm fell behind on payments on 27.6 billion yuan in trust products after last year being hammered by blowups in unit-trust products, sold to single institutional clients.

The firm’s struggle is on wide display because it’s one of the few listed trust companies, obliging it to provide detailed financial disclosures. It has also been one of the more aggressive, growing its assets almost 20-fold since 2013 as the industry’s assets as a whole doubled.

Anxin’s shares are now suspended in Shanghai, after plunging 80% from a peak in 2017. It was fined 14 million yuan by regulators this month for misconduct, including insufficient disclosure of risks and over-promising returns on its trust products.

Other trust companies have also warned of strains. China Everbright Trust and Jic Trust both had products miss payments, local media reported. Both firms declined to comment. Zhongtai Trust Co. said in an emailed statement that a borrower in Guizhou failed to repay loans because the virus outbreak had hurt the company’s sales of financial products and delayed its ability to secure a bank loan.

Two leading trust companies have missed payments to their investors on at least six products valued at more than 2.5 billion yuan, according to managers at the firms, who asked not to be identified discussing private matters. The products were tied to loans to local government financing vehicles and property developers, repayments of which have been delayed, they said.

Rolling over these products is also becoming increasingly difficult as the government isn’t easing restrictions on who can invest with trusts, the people said.

There is likely to be more pain to come. One of the trust sector’s prime clients have been housing developers. As China locked down its economy at the start of the year, more than 100 real estate firms filed for bankruptcy as housing sales came to a halt, adding to almost 500 collapses in 2019.

“Some highly leveraged developers with piles of short-term debt have been surviving on their high turnover rate,” said Gu Xiaoming, an analyst at Zhengzhou-based Bridge Trust Co. “They will be under great pressure to make the payments on time.”

©2020 Bloomberg L.P.

With assistance from Bloomberg