Property Stocks Tumble; China Backs Deals: Evergrande Update

Track the latest Evergrande updates here.

(Bloomberg) -- Chinese property stocks tumbled close to a new five-year low after a series of asset sales underscored concern that equity investors will bear the brunt of losses as developers offload projects to repay debt.

Shimao Group Holdings Ltd. agreed to sell stakes in a Hong Kong development at a loss while Sunac China Holdings Ltd. unloaded assets in Shanghai as developers seek to raise cash. China regulators meanwhile signaled they will support “quality” real estate firms looking to buy assets from struggling rivals, according to a report.

An index of Chinese developers fell for the sixth day in seven, led by Sunac, which posted a record one-day decline of 18%. Trading in Chinese dollar bonds remained light during the seasonal end-of-year lull, according to credit traders.

The rout in developer shares means the richest bosses behind China’s real estate firms have lost more than $46 billion combined this year, according to the Bloomberg Billionaires Index. Evergrande founder Hui Ka Yan’s wealth alone has plunged by $17.2 billion.

Key Developments:

- China Regulators Encourage Property Project Acquisitions: Report

- Evergrande Boss Leads $46 Billion Wealth Loss in Worst Year Yet

- China Regulators in Talks With Shimao, Trusts on Loan Extension

- Moody’s Downgrades Greenland Holding Group

- Sunac’s Further Asset Disposals May Boost Cash: Credit React

- Fitch Forecasts Chinese House Sales Dropping 10%-15% in 2022

- Shimao’s H.K. Disposal at a Loss May Imply Liquidity Woes: React

Evergrande Land Seized by Chengdu City on Lack of Development (6:37 p.m. HK)

The local government in western China’s Chengdu city took two parcels back without repaying the developers, saying that Evergrande failed to start construction on time, according to Dec. 17 statements from a Chengdu land regulator.

One site, sized 83,997 square meters, was sold to a firm fully owned by by Evergrande’s onshore subsidiary Hengda Real Estate in 2010, according to a statement and corporate registry search platform Qichacha.

Another site, sized 258,667 square meters, was sold to a developer in 2002 and transferred to another Hengda unit in 2011, according to a separate statement and Qichacha.

China Chengxin Cuts Evergrande Onshore Unit Rating to B From BB (6:10 p.m. HK)

China Chengxin International noticed deteriorating cash flow of Evergrande as its funds to repay bonds will be “very limited,” according to a statement.

China’s RiseSun Said to Weigh $1.6 Billion Battery Unit Sale (5:48 p.m. HK)

Chinese real estate developer RiseSun Holdings Co. is considering a potential sale of a unit that makes electric-vehicle batteries, according to people familiar with the situation.

The company is working with an adviser to identify prospective buyers and is seeking as much as 10 billion yuan ($1.6 billion) for RiseSun Mengguli Power Technology Co., the people said, asking not to be identified as the information is private.

RiseSun is also weighing other options, including selling a stake in RiseSun MGL to raise fresh funds, the people said. Negotiations are ongoing and there’s no certainty the talks will result in a transaction, they added.

A representative for RiseSun declined to comment.

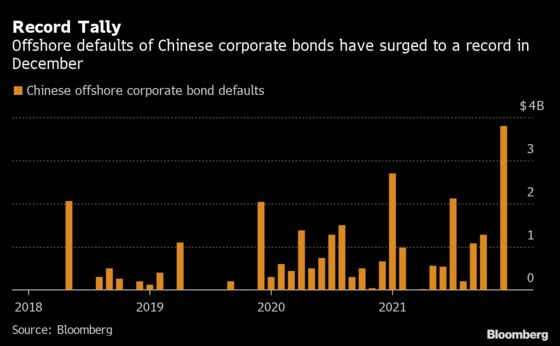

China Offshore Bond Defaults Hit Record in December (4:10 p.m. HK)

December is poised to be a record month for Chinese offshore corporate defaults after missed payments by indebted companies including China Evergrande and Kaisa Group Holdings Ltd.

Chinese firms have defaulted on a record $3.8 billion in offshore bonds so far this month, data compiled by Bloomberg show. The previous monthly high was in January when Chinese borrowers failed to repay $2.7 billion of such notes.

China Regulators Encourage Property Acquisitions (2:15 p.m. HK)

China is ramping up support of the embattled real estate sector as growing stress in the industry threatens to deepen an economic slowdown.

Authorities are encouraging banks to fund acquisitions of projects of distressed developers and pushing financially healthy property firms to make such purchases, the central bank-backed Financial News reported Monday.

China is also providing credit support to an economy showing strain from the property slump, with domestic banks on Monday lowering borrowing costs for the first time in 20 months. The move follows action by the People’s Bank of China earlier this month to cut the amount of cash banks must hold in reserve, freeing up 1.2 trillion yuan ($188 billion) of cheap long-term funds for lenders.

The support measures come as some developers such as Kaisa and Evergrande struggle to sell assets to raise cash and service mounting debts amid a crackdown on leverage in the industry. Regulators have eased up on the clampdown in recent weeks, such as by encouraging stronger real estate firms to tap the onshore interbank bond market for financing.

Jones Lang Sees Opportunities in China Despite Woes (11:05 a.m. HK)

China still has strong economic fundamentals that will provide opportunities for both onshore and offshore investors, Jones Lang LaSalle’s Asia-Pacific Chief Executive Officer Anthony Couse said in an interview on Bloomberg TV.

The Chinese government has been focused on ensuring developers deleverage in the past five years, and highly leveraged firms will look to dispose of assets, presenting opportunities for onshore capital, investment and fund managers.

Kaisa Appoints Advisers; Shares Resume Trading (8:10 a.m. HK)

Kaisa has appointed Houlihan Lokey (China) Ltd as its financial adviser and Sidley Austin as legal adviser after missing multiple offshore debt payments.

The financial adviser will evaluate Kaisa’s liquidity and explore all feasible solutions, the company said in a stock exchange filing on Monday. Kaisa said it hasn’t received any notice regarding acceleration of repayment by holders, and has been in talks with holder representatives about a comprehensive debt restructuring plan. The shares dropped 12% in Hong Kong trading.

Evergrande Backer’s Privatization Collapses (8:05 a.m. HK)

Chinese Estates Holdings Ltd. minority shareholders failed to give sufficient support to the company’s proposed privatization, derailing a plan by the long-time ally of Evergrande to delist next month. The stock plunged 30%.

Among the 74 stockholders participating, 64 voted no and made up 10.8% of the shares among the investors, according to a stock exchange filing Friday. The Hong Kong real estate firm, owned by the family of billionaire Joseph Lau, announced plans in October to buy out investors at HK$4 a share. The stock last traded at HK$3.78 before being halted Friday afternoon ahead of the results. Chinese Estates requested a trading resumption and said its listing will be maintained.

Evergrande Declared in Default by S&P for Failed Payments (8 a.m. HK)

Evergrande was labeled a defaulter by S&P Global Ratings, the second credit-risk assessor to do so.

S&P cut Evergrande to “selective default” Friday over its failure to make coupon payments by the end of a grace period earlier this month, a move that may trigger cross defaults on the developer’s $19.2 billion of dollar debt. S&P also withdrew its ratings on the group at Evergrande’s request.

Fitch Ratings was the first to declare the property developer in default on Dec. 9. Long considered by many investors as too big to fail, Evergrande has become the largest casualty of President Xi Jinping’s campaign to tame the country’s overindebted conglomerates and overheated property market. Concern has since spread to higher-rated firms like Shimao Group as liquidity stress intensifies.

Shimao Sells Stake in Hong Kong Development (7:30 a.m. HK)

Shimao agreed to sell its 22.5% stake in three entities created for the Grand Victoria property development in Hong Kong for HK$2.1 billion ($270 million), according to an exchange filing.

The buyers include entities owned by fellow developers SEA Holdings, Wheelock & Co. and Sino Land. Shimao expects to recognize a loss of about HK$770 million from the sale.

Separately, Sunac China Holdings Ltd. sold three projects in Shanghai and Hangzhou for 2.68 billion yuan ($420 million), the 21st Century Business Herald reported, citing unidentified people.

©2021 Bloomberg L.P.