Inside the $5 Billion ‘Apollo’ Deal to Salvage Cathay Pacific

Inside the $5 Billion ‘Apollo’ Deal to Salvage Cathay Pacific

(Bloomberg) -- The code name was “Apollo.” Its mission was to keep Cathay Pacific Airways Ltd. alive.

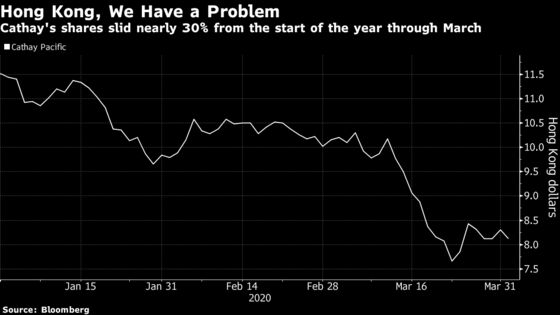

Hong Kong’s dominant airline had been in financial strife for months, its strong start to 2019 a distant memory. Social unrest in the city triggered a slump in passengers through the second half of last year. Then came the coronavirus pandemic, which forced Cathay to ground most of its fleet, cut salaries and put staff on unpaid leave as it hemorrhaged more than $10 million a day.

The carrier’s shares had lost a quarter of their value in the first few months of 2020 and passengers were down 99% from a year earlier. One of Hong Kong’s most-recognized brands was veering toward collapse.

In March, Chairman Patrick Healy and Chief Executive Officer Augustus Tang kicked off negotiations that culminated with this week’s announcement of a plan to raise HK$39 billion ($5 billion) from the Hong Kong government and its top shareholders, namely Swire Pacific Ltd., state-run Air China Ltd. and Qatar Airways, according to people familiar with what happened.

The following account is based on conversations with those involved in bringing the rescue plan to fruition. The people asked not to be identified so they could speak freely about how the bailout came together. Cathay and its top shareholders either wouldn’t elaborate beyond their public statements or didn’t comment. The Hong Kong government and Cathay Group have long maintained close communication “on different issues,” the city financial secretary’s office said in a statement.

The task at hand was so big -- almost like a moonshot -- that the deal was code-named “Apollo.” The Greek god was famously used by NASA as the moniker for its program to put men on the moon.

Cathay hired Morgan Stanley to help orchestrate complex negotiations involving Swire Pacific and Air China. As Cathay’s troubles mounted, speculation grew that Swire -- one of the last remaining British trading companies based in Hong Kong -- might sell its stake to Air China, which already owns almost 30% of the airline. Both shareholders were active in the talks to ensure their holdings weren’t diluted.

It soon became clear that billions in fresh capital was needed to ensure Cathay’s continued viability. Singapore Airlines Ltd. had already unveiled a plan to raise S$8.8 billion ($6.3 billion) in a rights issue backed by its biggest shareholder, state investor Temasek Holdings Pte. That deal, and other airline rescue plans, would serve as a template for Cathay.

Bet on Recovery

But arranging a rescue for Cathay would be far more complex and take more time since it would involve lengthy back-and-forth negotiations with shareholders, including an airline controlled by the Chinese government -- which has been strengthening its clout in the former British colony. The Hong Kong government also would be involved, hiring as its adviser Goldman Sachs Group Inc., which declined to comment for this story.

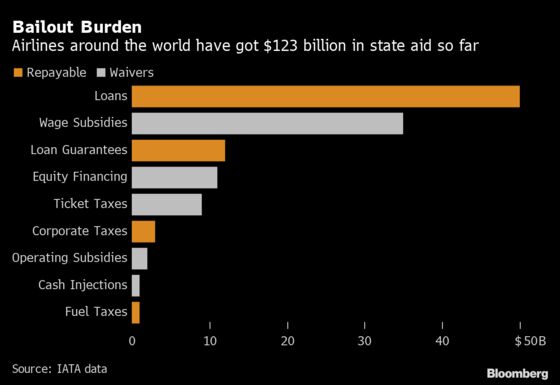

Local authorities were receptive to the airline’s request for help since they considered it a key asset to the city’s future as a financial, commercial and trading hub. It also presented an opportunity to make a significant investment betting on the recovery of the industry, rather than just being a straight-up bailout. And it would hardly be controversial: the aviation industry has received more than $120 billion in state aid to weather the coronavirus pandemic, according to the International Air Transport Association.

With the spread of Covid-19, video calls were becoming widely used in deal-making. Cathay and its advisers used Zoom and other teleconferencing programs during negotiations, along with the more traditional approach of conference calls and face-to-face meetings at various corporate offices around Hong Kong.

The deal had to be announced on a Tuesday to coincide with the city’s weekly executive council meetings. That meant advisers didn’t sleep much in the lead up, especially the night before, as they hammered out the details.

‘Observer’ Board Seats

The proposal involved the carrier selling to the Hong Kong government HK$19.5 billion of preferred stock and HK$1.95 billion of warrants convertible into a 6.08% stake. The government would get a couple of “observer” seats on Cathay’s board too. The plan also consisted of a HK$11.7 billion rights issue underwritten by Morgan Stanley, Bank of China International Ltd., HSBC Holdings Plc and BNP Paribas SA.

Swire, Air China and Qatar Airways supported all the resolutions for the recapitalization. An extraordinary general meeting to approve the plan is slated to take place on or around July 13.

“As a long-term shareholder, we have strong commitment to Cathay Pacific, and have full confidence in its long-term future,” Swire said.

Helping spearhead the bailout was Tang, appointed Cathay CEO in August after a long career with Swire Group. The British family-run business empire has roots in the region dating back to the 19th century, when it had interests in steam shipping on the Yangtze River and the sugar trade.

Swire invested in Cathay in 1948, shortly after the airline was founded, and was expelled from the mainland following the founding of the People’s Republic of China in 1949. It started consolidating businesses in Hong Kong, and today is the largest shareholder in Cathay with a 45% stake.

While the plan was designed to help Cathay survive the crisis, there’s so much uncertainty over the future of the airline industry and the timing of a recovery in demand that questions remain as to whether the package will be enough.

| Read more on the crisis in the aviation industry: |

|---|

| Airline Industry Forecast to Suffer Record $84 Billion Loss |

| Government Aid to Airlines Differs Vastly Between Regions: Chart |

| U.K. Travel Firms Attack Quarantine as IATA Says No One Will Fly |

Cathay itself said it may access equity and debt capital markets again to strengthen its balance sheet if conditions are right.

“Tough decisions will need to be made in the fourth quarter of this year to get Cathay Pacific to the right size and shape in which to compete successfully,” Healy said Tuesday. “Nothing is off the table.”

Longer term, the airline aims to leverage its geographical position to feed off growth and demand in the Greater Bay Area of Hong Kong, Macau and southern China’s Guangdong province. Cathay executives regularly refer to the area as a driver of growth over the next few decades.

“Our short-term challenges are significant, but our long-term future remains bright,” Healy said in his statement.

For now, executives at Cathay and its bankers will have to plug away to get shareholder approval and to sell the deal to investors. Until they ensure that this “Apollo” mission to save Cathay is successful, the traditional cocktails-and-dinner celebration for the conclusion of a deal will have to wait.

©2020 Bloomberg L.P.