China Plans $7 Billion Huarong Recapitalization Led by Citic

Huarong Poised to Get $7 Billion in Citic-Led Recapitalization

(Bloomberg) -- China Huarong Asset Management Co. is poised to receive about 50 billion yuan ($7.7 billion) of fresh capital as part of an overhaul plan that would shift control of the embattled company to state-owned conglomerate Citic Group, people familiar with the matter said.

The plan, some details of which are still being finalized and could change, calls for Citic to assume the Chinese government’s controlling stake in Huarong from the Ministry of Finance, the people said, asking not to be identified discussing a private matter. The capital injection would come from a Citic-led consortium, two of the people said.

Broad outlines of the plan have been approved by China’s State Council and could be announced as soon as this week, the people said. REDD reported some details of the proposed overhaul earlier this week.

Huarong’s dollar bonds rose to multi-month highs after Bloomberg’s report on Wednesday, with the 4.5% perpetual note climbing 4.4 cents on the dollar to 90.5 cents. That’s up from a low of 50 cents in May.

If Beijing follows through, it would mark the government’s first major attempt to resolve a crisis at Huarong that has roiled the world’s second-largest credit market since April. The financial giant’s plight has become the biggest test in decades of Chinese authorities’ willingness to support troubled state-owned borrowers amid a record wave of defaults.

Existing Huarong shareholders will likely see the value of their stakes plunge as the company recognizes losses on non-performing assets, two people familiar with the plan said. Warburg Pincus and Goldman Sachs Group Inc. are among a group of investors that bought a $2.4 billion stake in Huarong before it went public in 2015.

For bondholders, the implications are less straightforward. While the capital injection would help shore up Huarong’s balance sheet, the stake transfer to Citic would leave the company one step removed from government control -- a change that may unnerve some creditors. Huarong plans to continue honoring local and offshore debt obligations, but its ability to do so over the longer term will depend on how much cash it can raise from asset disposals, the people said. Huarong aims to raise about 50 billion yuan from asset sales, one of the people said.

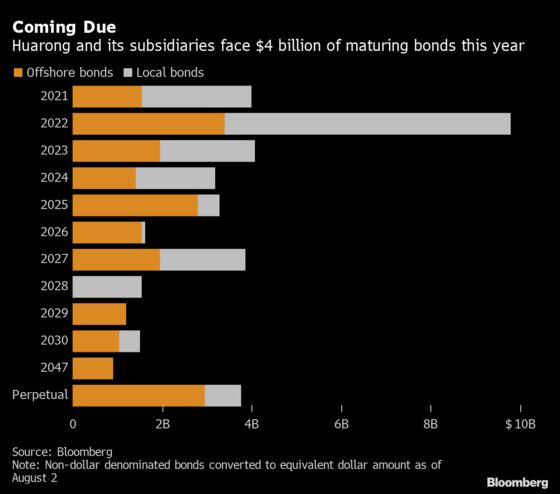

The government’s ultimate decision on Huarong will be scrutinized by investors for its broader implications. Any effort to help the company make good on its $242 billion of liabilities -- including about $21 billion of offshore bonds -- would neutralize a potential systemic risk to China’s financial system and make it easier for other state-owned borrowers to tap the country’s $12 trillion credit market.

At the same time, authorities may be wary of providing unconditional support. That would likely undermine President Xi Jinping’s campaign to curb reckless borrowing, much of which has been enabled by implicit government guarantees. When asked about Huarong last month, a spokesperson for China’s banking regulator said the government addresses problems at risky companies with “market-oriented” solutions.

Some analysts have warned that rescuing troubled companies will only delay China’s reckoning with its record corporate debt pile, making it more painful when a crisis inevitably strikes.

What Bloomberg Intelligence Says...

“In order to avoid contagion for other Chinese SOEs, the government and Citic could choose to avoid haircuts for Huarong bondholders and ask shareholders to bear losses, as has been done in previous bailouts in China.”

--Dan Wang, credit analyst

In response to a request for comment, Huarong said its public filings should be the primary source of information about its situation. The company said in a Hong Kong exchange filing on Tuesday that shareholders had approved several resolutions at an extraordinary general meeting, including the appointment of a new executive director. The filing didn’t mention anything about a capital injection.

Citic, one of China’s biggest state-owned companies, didn’t respond to requests for comment. Nor did the Ministry of Finance and the China Banking and Insurance Regulatory Commission, which regulates bad-debt managers.

Huarong’s fate has been a subject of intense speculation since it missed a deadline to report results at the end of March. That stoked concern the company might be headed for a landmark default, sending its bonds to record lows.

While missed payments at state-owned Chinese companies have become more common in recent years, none of the defaulters have been as systemically important as Huarong. In addition to its close link to China’s central government and complex web of connections to other financial institutions, Huarong is also one of the country’s biggest issuers of offshore bonds that sit in portfolios from Hong Kong to London and New York.

Huarong has so far repaid all its bonds on time and said last month it would redeem a $500 million perpetual note in September, helping to boost market confidence. The company has also reached agreements with state-owned banks to ensure it can meet obligations through at least the end of August, Bloomberg reported in May.

Investors have remained jittery because both Huarong and regulators have stayed quiet about the state of the company’s finances and restructuring plans. Huarong’s dollar bonds due January 2025 trade at about 84 cents on the dollar, implying an unusually high risk of default for an investment-grade issuer.

Whether or not the capital injection plan comes to fruition, Huarong’s balance sheet is poised to shrink over time, people familiar with the matter said. The company is planning to sell nearly all its local units outside of the core distressed-debt business, Bloomberg reported in June.

Huarong, together with China Cinda Asset Management Co., China Great Wall Asset Management Co. and China Orient Asset Management Co., was created to buy bad loans from banks in the aftermath of the late 1990s Asian financial crisis, when decades of government-directed lending to state companies had left China’s biggest lenders on the brink of insolvency.

The bad-debt firms later expanded beyond their original mandate, creating a labyrinth of subsidiaries to engage in other financial businesses and borrow billions from the bond market. Huarong was the most aggressive of the four under former Chairman Lai Xiaomin, who was executed in January for crimes including bribery.

Established in 1979 to help pilot Deng Xiaoping’s economic reforms, Citic Group is a ministerial level financial conglomerate directly overseen by China’s State Council. That means it sits above Huarong in the nation’s complex hierarchy of government ministries and state-owned enterprises. Citic Group last year appointed former People’s Bank of China Deputy Governor Zhu Hexin as its chairman.

Citic Ltd., the group’s main listed arm, has about HK$9.7 trillion ($1.25 trillion) of assets and holds stakes in firms including China Citic Bank Corp. and Citic Securities Co.

©2021 Bloomberg L.P.

With assistance from Bloomberg