Global Private Equity Snaps Up Chinese Commercial Property

Global Private Equity Snaps Up Chinese Commercial Property

(Bloomberg) -- A flurry of private equity funds buying commercial property in China is reviving syndicated loan volumes in the region.

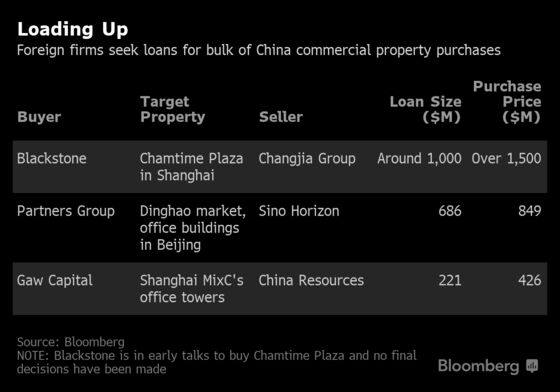

Firms including Blackstone Group LP and GAW Capital Advisors are in talks with banks in Asia for loan deals of more than $2 billion so far this year to buy office towers mainly in Beijing and Shanghai. The pipeline of such deals is expected to grow, which will help broaden financing opportunities for lenders, according to Standard Chartered Plc. Overseas firms purchased a record $9 billion of commercial property in China last year.

"We expect loan demand from recent foreign private equity firms’ acquisition activity in the real estate sector in East Asia to continue, given that numerous sponsors have or are raising sizable real estate and infrastructure funds," said Lyndon Hsu, global head of leveraged & structured solutions at Standard Chartered in Singapore.

Commercial property investment in China by foreign firms surged 62 percent to 78 billion yuan ($11.6 billion) in 2018, the largest amount in data dating back to 2005, according to CBRE Group Inc. In contrast, China’s acquisition-related syndicated loan volumes slumped about 34 percent to $16.6 billion last year amid lackluster economic growth and tight capital control in the country.

HSBC Holdings Plc is seeing increased interest from foreign investment firms for property in China, according to Steve Willingham, Hong Kong-based co-head of infrastructure and real estate finance for Asia Pacific. “Investors consider China a growth market opportunity compared to markets like the U.S. and Europe.”

Loans for property purchases by top-tier financial sponsors, often partly backed by prime commercial buildings, are viewed as less risky for banks because they are less sensitive to a property downturn, unlike home prices. In November, Singaporean developer CapitaLand Ltd. and sovereign wealth fund GIC Ltd. splashed out 12.8 billion yuan to buy Shanghai’s tallest twin towers in the biggest commercial property purchase of 2018.

One caveat for such lending is some of these borrowers often push for higher amount of loans relative to the value of the underlying property. This means less buffer for banks to absorb price volatility. "The leverage ratio on those loans has generally become quite aggressive," said Yuanyuan Fan, managing director of mergers and acquisitions finance at China Merchants Bank Co. in Shenzhen. "Lenders will have to negotiate for tighter loan clauses to lower risks."

Here are further comments from bankers:

Lyndon Hsu at Standard Chartered

- Sees real estate acquisition activity and financing opportunities broadening from prime commercial property to logistics warehousing as China continues to improve and expand distribution efficiency to cater to large online goods providers

- Data center development is also another real estate sub-sector which is growing fast given the need for computers capable of storing enormous volumes of data

Steve Willingham at HSBC

- In real estate investments there’s often a limit on the amount of debt that can be raised onshore based on existing mortgages and capital expenditure

- Investors often push for higher leverage to increase returns in late stages of a property cycle. But that’s a global challenge, not just a China phenomenon

Yuanyuan Fan at China Merchants Bank in Shenzhen

- It’s natural that these loans have more Chinese banks on board as the underlying assets are in China and local lenders now have closer relationships with foreign private equity firms after years of overseas expansion

To contact the reporters on this story: Carol Zhong in Hong Kong at yzhong71@bloomberg.net;Annie Lee in Hong Kong at olee42@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu

©2019 Bloomberg L.P.